Listen to this Blog

📊 CDSL Q4 & FY25 Result Analysis

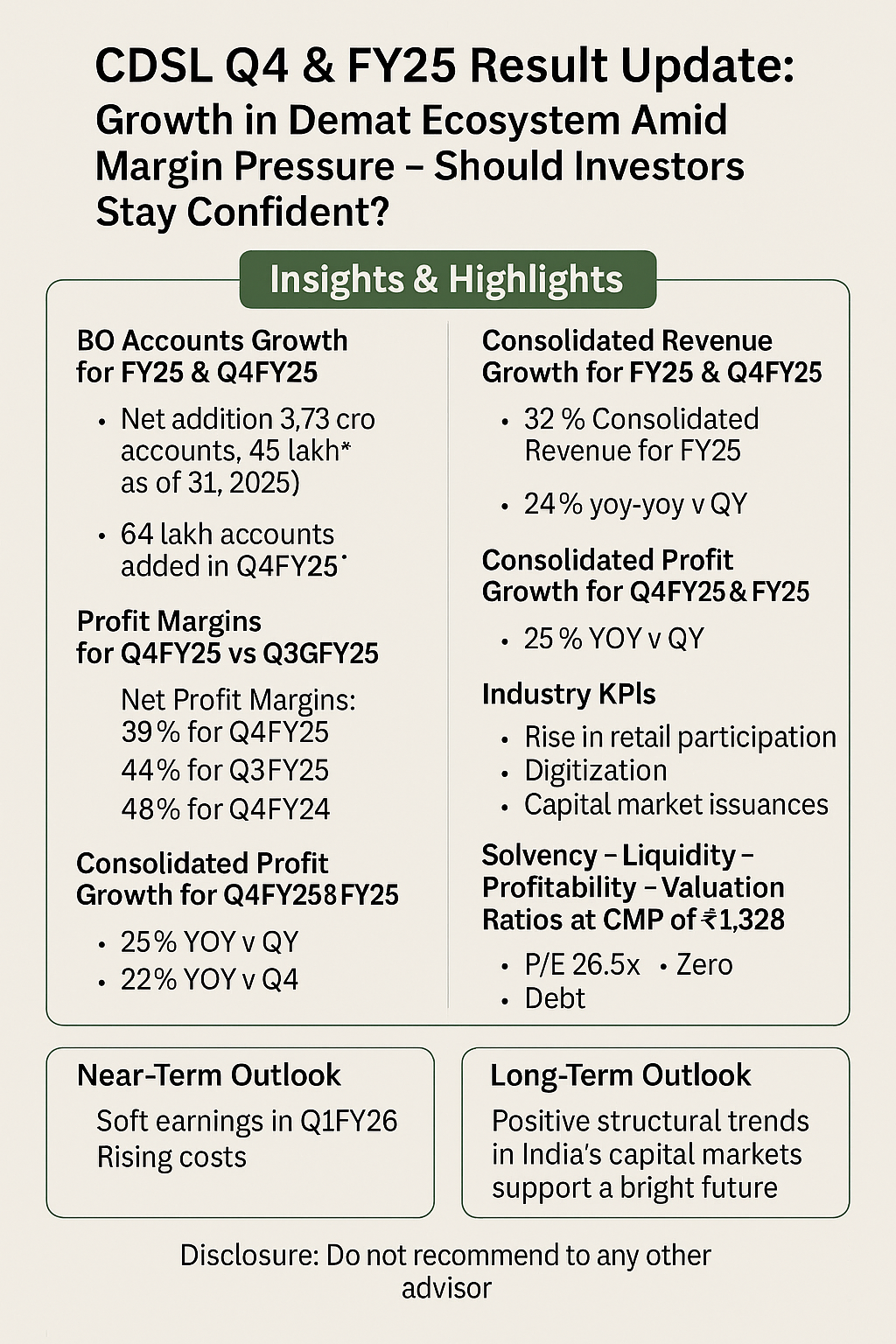

CDSL Q4 & FY25 Results: Growth in Demat Ecosystem Amid Margin Pressure – Should Investors Stay Confident?

Explore CDSL’s Q4 & FY25 results: BO account growth, revenue trends, profitability analysis, industry KPIs, and investor outlook. Fair valuation insights at CMP ₹1328.

🔍 Key Business Highlights

BO Account Growth:

FY25 Net Additions: 3.73 crore new demat accounts (15.29+ Cr total BO accounts as of March 31, 2025)

Quarterly Trend (Q4FY25): Net addition of 64 lakh accounts, slight drop QoQ.

Demat Custody Value:

Rose to ₹35.92 lakh crore in Q4FY25, up from ₹31.56 lakh crore in Q3FY25 and ₹23.06 lakh crore in Q4FY24 – a 56% YoY growth.

Number of Issuers & ISINs:

Issuers: 98,436 (+36% YoY)

ISINs: Continuous upward trend, reflecting deepening of the capital markets.

📈 Financial Performance Summary

✅ Consolidated Figures (₹ in Cr)

✅ Full-Year FY25 vs FY24

✅ Standalone Revenue Mix (Q4FY25)

Annual Issuer Income: ₹87 Cr

Transaction Charges: ₹49 Cr

IPO/CA Income: ₹25 Cr

Online Data Charges: ₹37 Cr

Other Income: ₹58 Cr

Dividend from Subsidiary (CVL): ₹48 Cr (in Q2FY25)

📉 Profitability & Margins

Despite a strong topline for FY25, Q4 margins declined YoY and QoQ due to rising employee & tech infra costs.

💡 Industry KPIs & Business Drivers

Structural Tailwinds:

Rise in retail participation

Digitization of financial services

Growth in capital market issuances

Subsidiary Strength:

CVL: 8.93 Cr+ KYC records (largest KRA), offers RTA, GSP, e-KYC, and e-Sign

CIRL: 17.5L e-insurance accounts

CCRL: Digital commodity receipts for FPOs and traders

🧮 Solvency, Liquidity, Profitability, Valuation

→ Verdict: Debt-Free, Cash-Rich, Profitable – but premium valuations.

🔎 Near-Term Outlook

Challenges:

Q4fy25 Revenue is down, suggesting cool off, -ve for fy26.

Margins under pressure due to rising operational costs

Market-linked income components (like IPO activity) remain cyclical

Opportunities:

Continued BO account growth

Cross-leveraging from subsidiaries (e-KYC, Insurance Repository, etc.)

Growing capital market inclusion through digital innovations

🌐 Long-Term Outlook

Bullish Structural Drivers:

Financial inclusion

Regulatory focus on transparency

India’s shift to digital investing platforms

Sustainable Moat:

Duopoly status

High switching costs for BO accounts

Platform stickiness

→ CDSL remains a long-term structural play on India’s capital market deepening.

📢 Disclosure

This blog is created for educational purposes only and does not constitute investment advice. Readers are advised to do their own research before making any investment decisions.

.jpg)