Listen to this Blog

📊 Havells FY25 Results Analysis: Robust Growth with Strategic Resilience

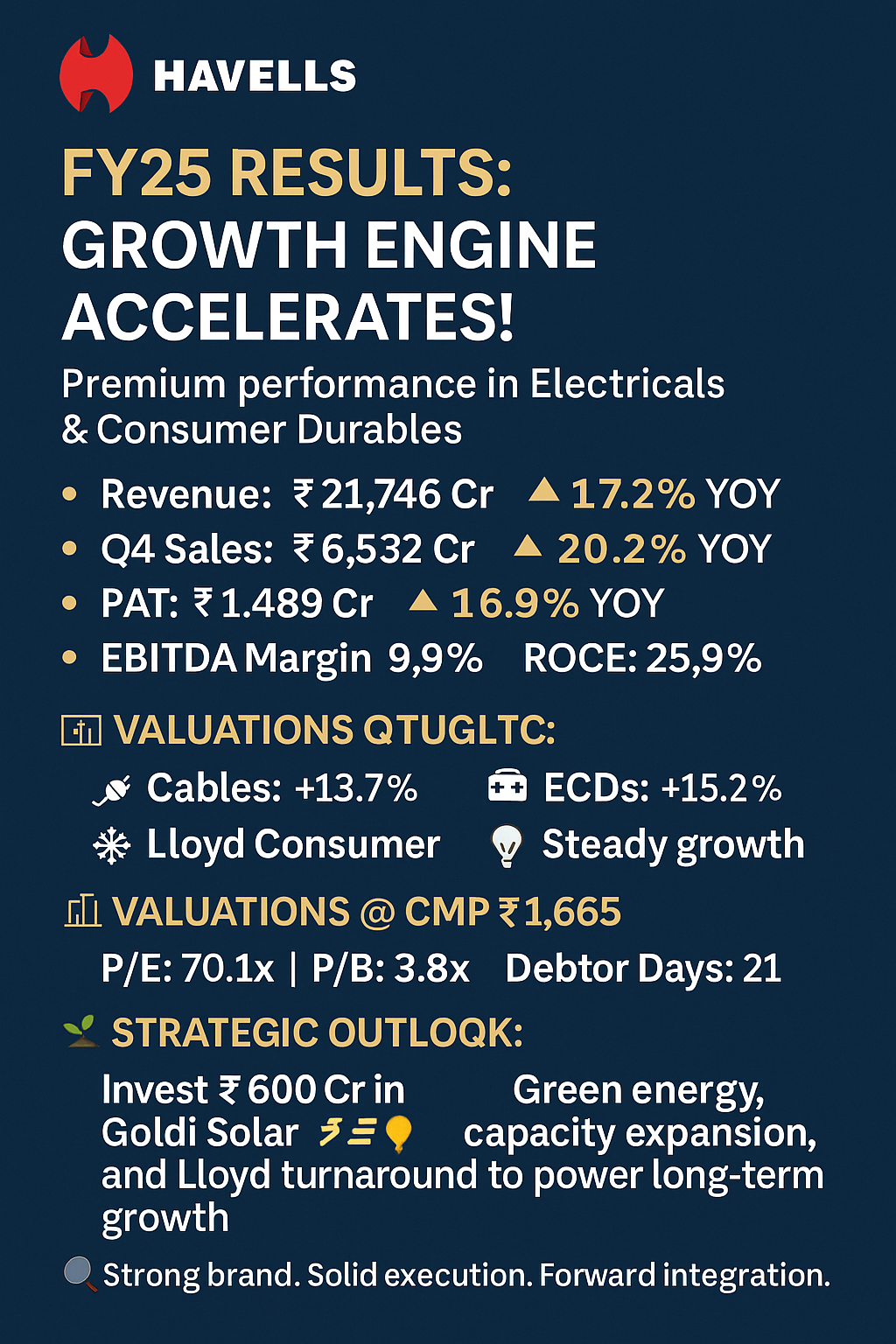

🔹 Revenue & Sales Growth – FY25 & Q4FY25

FY25 Net Revenue: ₹21,746 Cr — up +17.2% YoY from ₹18,550 Cr.

Q4FY25 Revenue: ₹6,532 Cr — up +20.2% YoY, led by Lloyd Consumer (+39.5%) and Cables (+21.2%).

Core segments like Switchgears (+6.7%), Lighting (+1.6%), and ECDs (+15.2%) maintained positive momentum.

🧩 Segmental Performance – FY25 & Q4FY25

📌 Insight: Lloyd segment turned around with full-year profitability; ECDs and Cables continue to scale with better product mix and capacity expansion.

💰 Profitability Analysis

⚙️ Commentary: Despite inflationary pressures, Havells maintained margin discipline aided by cost optimization and product premiumization.

🧮 Key Financial Ratios (FY25)

ROE: 18.8%

ROCE: 25.9%

Current Ratio: 1.8

Inventory Days: 67

Debtor Days: 21

Net Working Capital: 37 days (stable YoY)

💡 Liquidity remains strong, ensuring operational flexibility.

💼 Valuations at CMP ₹1,665

📈 While valuations appear rich, the premium is attributed to the brand’s strong moats, execution history, and return ratios.

🌐 Industry & Strategic Outlook

The electricals and consumer durables sector is witnessing a structural demand shift due to urbanization, premium housing, and lifestyle upgradation.

Lloyd’s turnaround and investment in Goldi Solar (₹600 Cr for 9.2% stake) signals Havells’ strategic pivot towards the green energy value chain.

🔮 Near-Term & Long-Term Outlook

🔸 Near-Term:

Seasonal headwinds may moderate ECD sales in Q1 FY26.

Margin outlook stable due to softening raw material costs.

🔸 Long-Term:

Industry tailwinds from real estate, infra push, and solar integration.

Sustained outperformance possible through brand, distribution, and energy solutions.

📢 Disclosure

This analysis is for informational purposes only and does not constitute investment advice.

.jpg)