Listen to this Blog

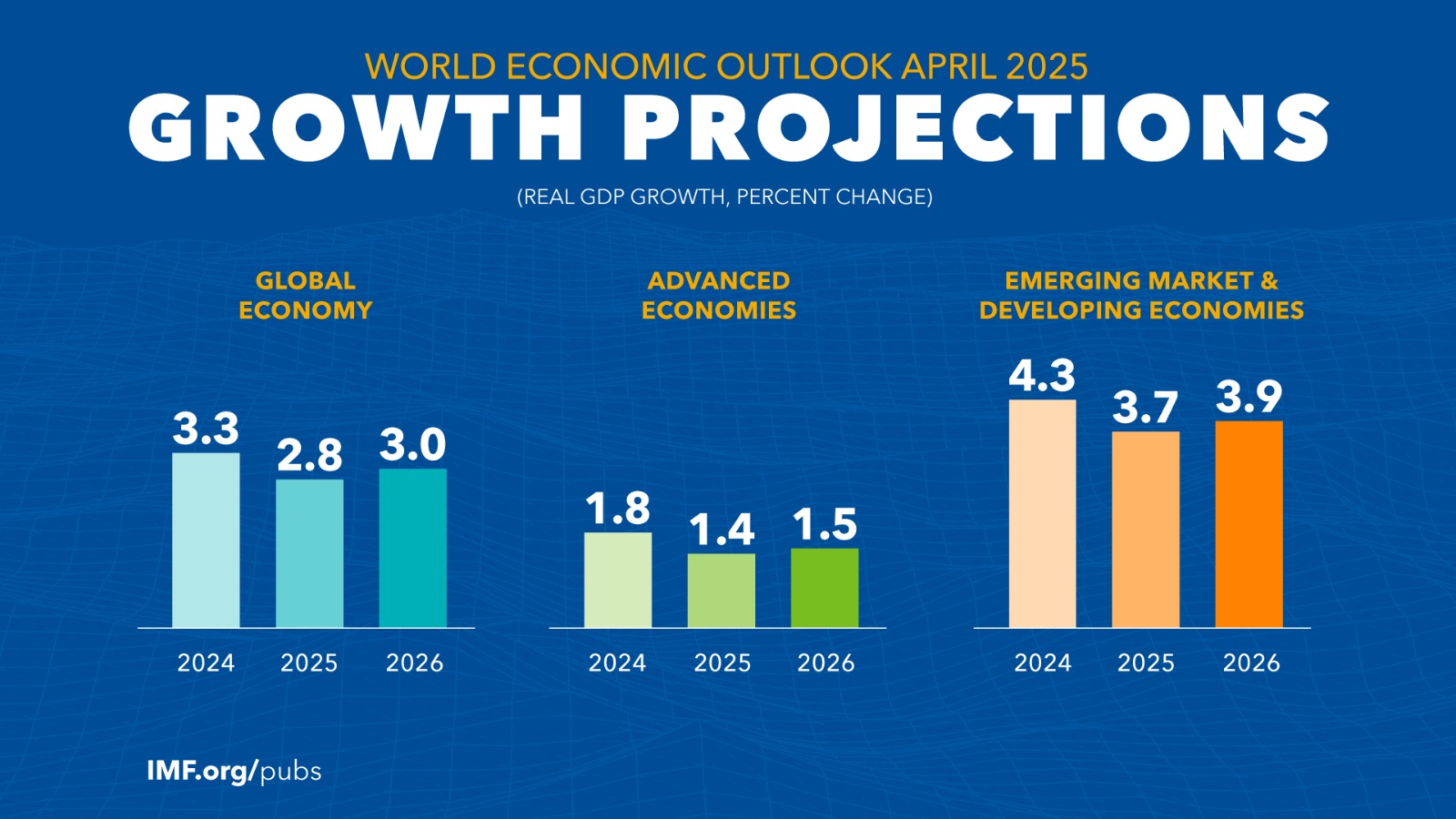

🌍 IMF World Economic Outlook 2025

📈 Long-Term Investment Insights, Sector Impacts & Companies

By Piyush Patel | Investment Strategist | Profit From IT

📅 Released: April 23, 2025

🧭 Executive Summary

The IMF April 2025 Report projects a deceleration in advanced economies while spotlighting growth in India, Southeast Asia, and select emerging markets. For investors, this is a strategic asset allocation moment — to realign portfolios towards resilient economies and forward-looking sectors.

🌐 Top Growth Projections – 2025 (GDP %)

| 🌏 Country | 📊 Projected Growth |

|---|---|

| 🇮🇳 India | 6.2% |

| 🇨🇳 China | 4.0% |

| 🇮🇩 Indonesia | 4.7% |

| 🇸🇦 Saudi Arabia | 3.0% |

| 🇪🇬 Egypt | 3.8% |

| 🇺🇸 USA | 1.8% |

| 🇧🇷 Brazil | 2.0% |

| 🇷🇺 Russia | 1.5% |

| 🇬🇧 UK | 1.1% |

| 🇩🇪 Germany | 0.0% |

🔗 Source – IMF World Economic Outlook April 2025

🏭 Sector-Wise Impact Analysis

| 🏷 Sector | 📉 Developed Markets | 📈 India / EMs | 📌 Notes |

|---|---|---|---|

| 🏗 Infrastructure | 🔻 Limited Capex in EU | 🚀 Govt & Private-led Infra boom | L&T, KNR Construction, IRB Infra |

| 🏦 Financial Services | ⚖️ Cautious lending | 💹 Growing retail credit & UPI penetration | HDFC Bank, ICICI, Bajaj Finance |

| 🔌 Energy / Renewables | 🌿 Green shift, but slow | ⚡ Focus on solar, hydrogen, RE | Adani Green, JSW Energy, Borosil Renewables |

| 🛒 Consumption | 😐 Slow recovery in EU/US | 🍛 Rising middle class in India | DMart, HUL, ITC, Titan |

| 🧠 Tech & AI | 🎯 Focused US expansion | 💡 India’s SaaS & automation growth | Infosys, TCS, Zoho, Tata Elxsi |

| 🚗 EV & Mobility | 🚧 Flat in EU/US | ⚙️ EV ecosystem expansion in Asia | Tata Motors, Exide, M&M, Greaves |

| 🏥 Healthcare | ⚠️ Neutral to slow | 🏥 Insurance & diagnostics boom | Apollo, Dr. Lal, Star Health |

| 📦 Manufacturing | 📉 EU Deindustrializing | 🏭 PLI-led Capex in India | Dixon, Syrma SGS, Amber, Tata Electronics |

📌 Key Observations for Investors

🇮🇳 India: A Beacon of Growth (6.2%)

-

📈 Double-engine growth: Government infra & private capex.

-

📱 Tech, manufacturing, consumption, and BFSI lead the charge.

✅ Beneficiary Stocks:

-

L&T, HDFC Bank, TCS, DMart, Titan, ICICI Bank, Dixon Tech, Adani Green

🇨🇳 China: Restructuring Phase (4.0%)

-

🏭 Shift from real estate to tech, clean energy, and export focus.

-

🎯 Caution due to regulatory and geopolitical risks.

✅ Beneficiaries: BYD, NIO (Global EVs), Alibaba Cloud

⚠️ Risk: Real Estate exposure, Property ETFs

🇺🇸 USA: Resilient but Cooling (1.8%)

-

💉 Healthcare, AI, and defense tech remain strong.

-

🏦 Rate-sensitive sectors underperform.

✅ Companies: Microsoft, Nvidia, Lockheed Martin, UnitedHealth

⚠️ Risk: Banking & REITs in rate-sensitive zones

🇩🇪 🇫🇷 🇮🇹 Eurozone: Stagnation Alert

-

🧊 Germany’s 0.0% reflects industrial slowdown.

-

🔻 Manufacturing, auto, energy vulnerable.

⚠️ Avoid: EU-focused industrial ETFs, auto-heavy funds

🌍 Emerging Markets & Middle East

-

🌐 Diversification into Egypt, Indonesia, Saudi Arabia offers tailwinds.

-

⛽ Energy, tourism, and infrastructure play a big role.

✅ Companies: Saudi Aramco, Telkom Indonesia, Egypt’s CIB

Funds: iShares EM ETF, India + ASEAN-focused mutual funds

📈 Portfolio Action Plan – 2025 & Beyond

🧩 Reallocation Strategy:

-

✅ Increase exposure to: India, ASEAN, MENA

-

⚠️ Reduce allocation to: EU, Japan, over-leveraged global REITs

-

🔄 Rebalance into sector ETFs: infra, green energy, consumption, AI

💼 Tactical Allocation by Investment Instruments

| 🎯 Asset Class | 🛠 Suggested Focus |

|---|---|

| 📊 Equities | India/EM stocks, US Tech |

| 📦 Mutual Funds | Global Innovation, India Capex, EM Blend |

| 💰 Debt | Short-duration, India Corporate Bonds |

| 🏠 Real Assets | REITs (India), InvITs |

| 💎 Alternates | Gold (10–15%), Thematic SIPs (EV/Green) |

🔐 Final Word from the Strategist

🌟 The IMF’s 2025 roadmap clearly signals a pivot towards growth markets, with India at the forefront. Investors should align their capital towards macro-backed long-term compounding stories—not short-term noise.

📢 Invest in the direction of the wind, not against it.

🔐 Disclosure

This blog is intended for informational and educational purposes only and does not constitute financial advice or a recommendation to buy or sell any securities, mutual funds, or other investment products.

-

All growth projections and macroeconomic data cited are based on the IMF World Economic Outlook – April 2025, which are subject to revisions based on evolving global events and economic indicators.

-

Sectoral trends and company mentions are based on public data and industry performance as of the date of publication. Past performance is not indicative of future results.

-

Investing in equities, global markets, and mutual funds involves market risks.

.jpg)