Listen to this Blog

🏢 Company Overview

Jubilant FoodWorks Ltd. (JFL) is India’s largest QSR operator managing Domino’s Pizza, Popeyes, Dunkin’, and COFFY. With deep tech integration and operational strength, JFL concluded FY25 with a total of 3,316 stores across India and five international markets.

📈 Q4 FY25 Financial Highlights

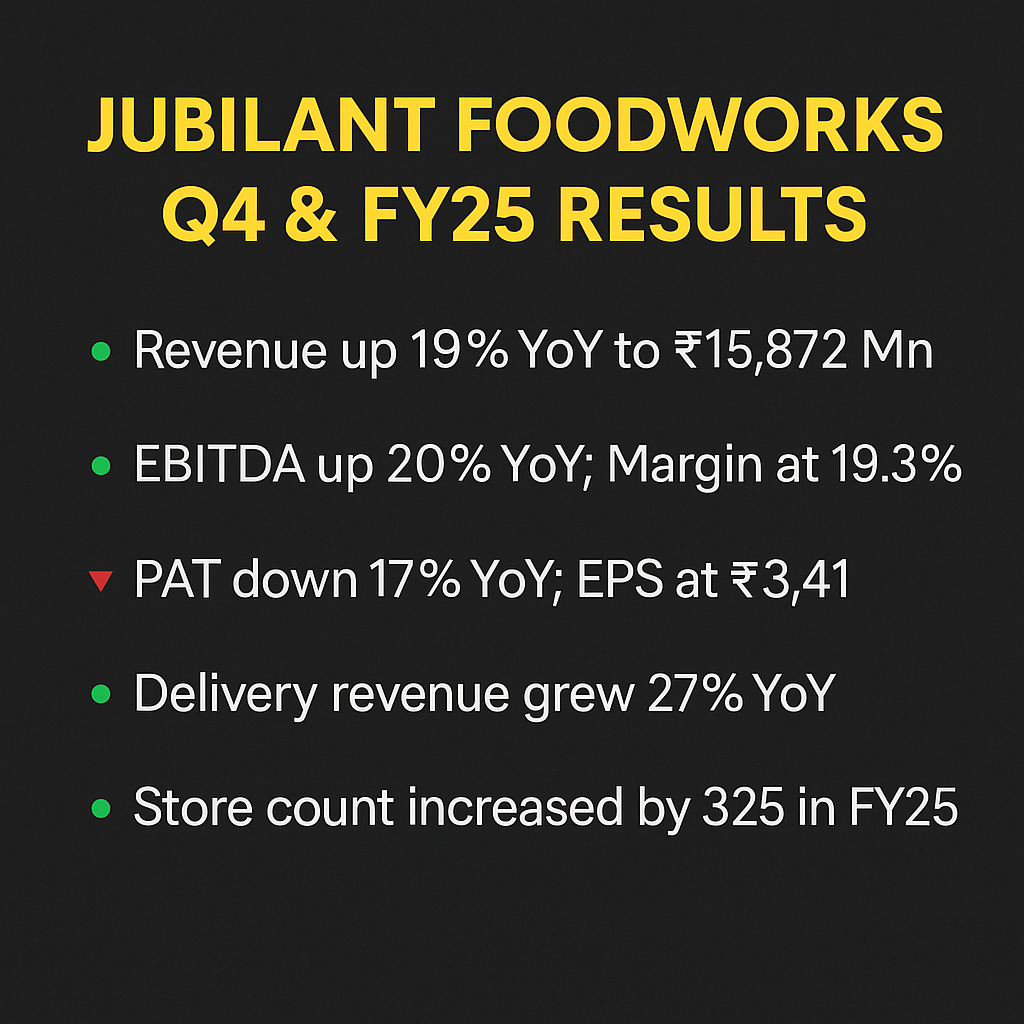

Revenue ₹15,872 Mn 🟢 +19.1% YoY

EBITDA ₹3,056 Mn 🟢 +19.7% YoY | EBITDA Margin 19.3%

PAT ₹495 Mn 🟢 +31.5% YoY | PAT Margin 3.1%

EPS ₹0.74 🟢 vs ₹0.57 YoY

Delivery Revenue 🟢 +27.1%

Like-for-Like Growth (Domino’s) 🟢 12.1%

Mature Store ADS ₹84,011

📅 FY25 Full-Year Performance

Metric FY25 YoY Growth Consolidated Revenue ₹81,417 Mn 🟢 +44.0% Standalone Revenue ₹61,047 Mn 🟢 +14.3% EBITDA ₹11,807 Mn 🟢 +7.8% PAT ₹1,941 Mn 🔴 -17.0% EPS ₹3.41 🔴 vs ₹3.52

🛒 Network & Segmental Insights

India Stores 2,304 (Domino’s 2,179)

International Stores 763

Net Additions in FY25 🟢 +325 Stores

City Presence Expanded to 475 🟢 +54 new cities

📊 Income Snapshot (₹ Mn)

Metric Q4 FY25 FY25 YoY Trend Revenue ₹15,872 ₹61,047 🟢 +14.3% EBITDA ₹3,056 ₹11,807 🟢 +7.8% PAT ₹495 ₹1,941 🔴 -17.0% PAT Margin 3.1% 3.2% 🔴 Decline EPS (₹) ₹0.74 ₹3.41 🔴 Lower YoY

⚙️ Key Financial Ratios (Standalone)

Debt-to-Equity 0.60 🔴 Higher than FY24

Current Ratio 1.12 🟢 Stable

PBV (Price to Book) 4.27x 🟢 Valuation Correction

Trade Receivables ₹3,301 Mn 🔴 +25% YoY

💸 Cash Flow Summary (₹ in Mn)

CFO (Operating) ₹16,680 🟢 Strong Growth

CFI (Investing) ₹-8,500 🟢 Reduced Outflow

CFF (Financing) ₹-8,495 🔴 Shift to repayments

Net Cash Flow ₹-315 🔴 Negative balance

🛠 Operational & Digital Innovation

Big Big Pizza launched with 6-flavor slices

ELATE Android-based PoS deployed

App MAUs 13.1 Mn 🟢 +17% YoY

Loyalty Members 33.7 Mn 🟢 Expanding base

🔮 FY26 Outlook & Strategic Direction

India Expansion planned 250 stores

Turkey Expansion planned 30–50 stores

Focus areas include dual product innovation, operating efficiency, digital ordering, and scaling Popeyes and COFFY brands

📘 Valuation Update

CMP ₹680

EPS FY25 ₹3.41

P/E Ratio 199.1x 🔴 Very High

Book Value per Share ₹159.26

P/BV Ratio 4.27x 🟢 Below 5-year average

🔍 Long-Term Watchlist for Investors

PAT margin expansion above 5 percent

Consistent SSSG above 10 percent YoY

Positive free cash flow trend

Scaling contribution from Popeyes and COFFY

ROE improvement and steady dividend payout

🧠 Key Investor Takeaways

🟢 Strong leadership in Indian QSR delivery segment

🟢 Growing digital and loyalty-driven customer base

🟢 Efficient cash generation despite expansion🔴 Valuation premium not yet backed by earnings growth

🔴 Negative free cash flow and high P/E

🔴 Margin pressures in international operations

📢 Disclaimer

This report is for educational purposes only. It is not investment advice. Please consult a SEBI-registered financial advisor before making investment decisions.

.jpg)