Bharat Electronics Ltd (BEL) Q4 FY26 Analysis: Stellar Full-Year Revenue Beat vs. Near-Term Margin Contraction

The Indian defense manufacturing landscape is undergoing a structural realignment, catalyzed by the government's aggressive "Atmanirbhar Bharat" (self-reliance) indigenization mandates. As the premier Navratna Defense PSU specializing in strategic electronics, Bharat Electronics Limited (BEL) is at the absolute epicenter of this capital expenditure cycle.

In this comprehensive earnings deep dive, we dissect BEL’s Q4 FY26 (January–March 2026) consolidated financial performance, analyze key management transcripts, benchmark the company against its closest peers, and evaluate whether the stock's premium valuation leaves a sufficient margin of safety for long-term investors.

1. The Snapshot

2. The "Wow" Factor: High-Impact Insights

Massive Topline Beat: BEL achieved record-high consolidated revenue of ₹27,610.11 Crore for the full year FY26, representing a growth of +16.15% YoY and dramatically outperforming the market’s early-year consensus forecast of ₹23,700 Crore by nearly ₹3,910 Crore due to aggressive execution in Q4.

Order Book at Historical Peak: The company's order book stood at ₹73,882 Crore as of April 1, 2026. This translates to an incredibly strong book-to-bill ratio of $2.68\times$, ensuring highly predictable revenue streams for the next three fiscal years.

The Margin Squeeze: Despite an 11.75% YoY growth in consolidated Q4 revenue, EBITDA margins contracted by 161 basis points YoY to 29.17% (down from 30.78%). This margin contraction was primarily driven by a sharp +37% YoY surge in other operational expenses and provision-led charges.

Aggressive Institutional Accumulation: DII holding crossed 20% for the first time in BEL's history during Q4 FY26, with combined institutional ownership (FPI + DII) reaching 39.5%. Foreign Portfolio Investors (FPIs) added 99 basis points to stand at 19.50%, reinforcing the structural accumulation thesis.

3. Operational KPI Table

To understand BEL's operational health, we track key sector-specific metrics:

4. Financial Deep Dive

The fourth quarter is seasonally the strongest for defense contractors due to year-end execution cycles. BEL’s Q4 FY26 consolidated financial results reflect steady delivery, though operating leverage was partially offset by escalating costs.

Consolidated Financial Comparison Table

All figures in ₹ Crore (except margins and EPS):

$$\text{EBITDA Margin} = \left( \frac{\text{EBITDA}}{\text{Revenue from Operations}} \right) \times 100$$

Cost vs. Efficiency Analysis

Our "Margin of Safety" framework demands critical focus on operational costs:

Material Costs & Raw Materials: Raw material costs rose by 8.2% YoY, driven by supply chain realities in high-end semiconductor procurement. Semiconductors account for roughly 17--19% of BEL's total material inputs, leaving it sensitive to import price fluctuations from Taiwan, Europe, and the US.

Employee Benefit Expenses: Employee costs grew by 8.5% YoY as BEL continues to scale its design capabilities. This is a necessary "investment" rather than structural leak; advanced radar development and software integration require high-value, niche engineering talent.

Other Expenses Surge: The primary pain point in Q4 was a sharp +37% YoY increase in other expenses due to provision adjustments and warranty clauses. This restricted absolute EBITDA growth to +5.9%, causing the overall EBITDA margin to contract by 161 bps to 29.17%.

5. Peer Benchmarking: BEL vs. HAL

How does BEL perform against its closest defense sector peer, Hindustan Aeronautics Limited (HAL)?

6. The Forward Curve: FY27 Outlook

Based on the latest earnings call transcripts, management has issued highly concrete forward guidance for FY27:

Revenue Growth Target: Projected at 15%+ YoY, which models an estimated FY27 consolidated revenue of approx ₹31,750 Crore.

EBITDA Margin Guidance: Guaranteed to remain above 28%, backed by rising indigenization which offsets raw material inflation.

Order Inflows: Expected to exceed ₹55,000 Crore in FY27.

The QRSAM Mega-Catalyst: The single largest near-term catalyst is the upcoming ₹30,000 Crore Quick Reaction Surface-to-Air Missile (QRSAM) order. Expected to be formally awarded in early Q2 FY27, BEL will act as the lead system integrator with a dominant 70% share. This contract alone will expand BEL's active order book to over ₹1,00,000 Crore.

Capex & R&D Commitments: Management guided for ₹1,200 Crore in capital expenditure and ₹2,200 Crore in R&D to scale new technologies like artificial intelligence, cyber warfare, and directed energy weapons (DEWs).

7. Valuation Guardrails

Current P/E = CMP/TTM EPS = 410.95/8.29 = 49.57x

Book Value Per Share (BVPS) approx ₹32.50 Price-to-Book (P/B)approx 12.6x

Five-Year Historical Context

5-Year Median P/E: $41.3\times$

Current P/E: $49.57\times$

Valuation Category: Trading at a Premium

The Premium Justification

While a 49.5times forward P/E is historically rich, the stock is insulated by several defensive characteristics:

Zero-Debt Balance Sheet: BEL maintains a net-cash position with substantial working capital reserves.

Impending Backlog Expansion: The QRSAM and long-gestation electronic fuzes contracts provide near-unrivaled cash flow predictability.

Monopolistic Integration Moat: BEL addresses 50--60% of electronics scope in Indian naval and airborne platform manufacturing, rendering it a structural beneficiary of India's capital expenditure growth.

8. Shareholding Pattern Shift (Q4 FY26)

There have been notable movements in the equity ownership distribution of BEL:

[Promoter: 51.14%] ====> Unchanged (Govt of India)

[FIIs/FPIs: 19.50%] ====> Up +99 bps (from 18.51% in Dec 2025)

[Mutual Funds: 14.28%] => Down -54 bps (from 14.82% in Dec 2025)

[Retail & Public: 9.37%] => Down -50 bps (from 9.87% in Dec 2025)

[Promoter Pledge: 0.00%] => Perfect Credit Comfort

Key Takeaway: The institutional migration from retail hands to high-conviction foreign institutions in Q4 FY26 indicates that professional capital is aggressively buying the post-March correction as a long-term compounder.

9. The Advisory Note: Strategic vs. Tactical

The Strategic Thesis (Long-Term): For institutional investors looking at a 3–5 year horizon, BEL remains a "Core Compounder." The company’s deep indigenization moat, structural relevance to national defense, and entry into civil domains (like Metro signaling and AI healthcare infrastructure) protect its business model. Any major market correction should be treated as a strong buying opportunity.

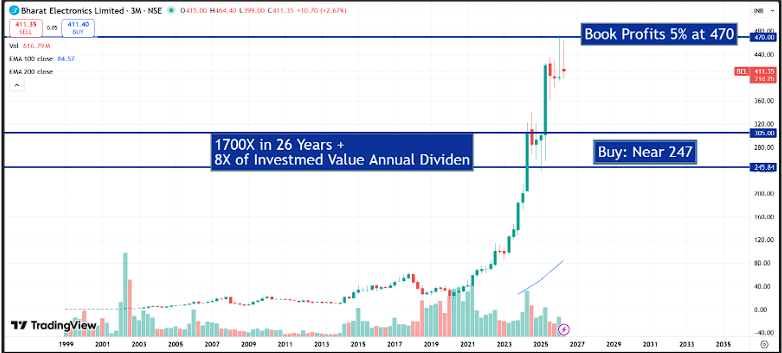

The Tactical Play (Near-Term): Tactically, the stock is currently digesting its massive multi-year run-up. The recent $10\%$ correction from its March 52-week high of ₹473.45 is a healthy consolidation. Strong technical support is established at ₹305(representing its 50MEMA).

Actionable Advice: We recommend an accumulate-on-dips strategy. Instead of deploying lump-sum capital at current levels, investors should scale in systematically, targeting the ₹305–₹250 range.

Fair value: https://docs.google.com/spreadsheets/d/e/2PACX-1vQnnzD1FwulYQ7XKiShXw_FurJLgvqo-o0d7FK46x-05mXijZD-lSkCmpXKcoJU6Q/pubhtml?gid=1488823234&single=true

Mandatory Professional Disclosure

This report is prepared by our Senior Investment Advisory desk solely for educational and informational purposes. It does not constitute formal, personalized investment advice or an endorsement to buy or sell securities.