📊 Private Sector Banks H1 FY26 – Quality Growth & Investment Insights

🔎 Industry Overview

India’s private sector banks in H1 FY26 delivered mixed results:

Industry sales growth: +5.0%

Industry profit growth: -4.5%

Deposits: ₹87,09,861 Cr

Advances: ₹80,51,880 Cr

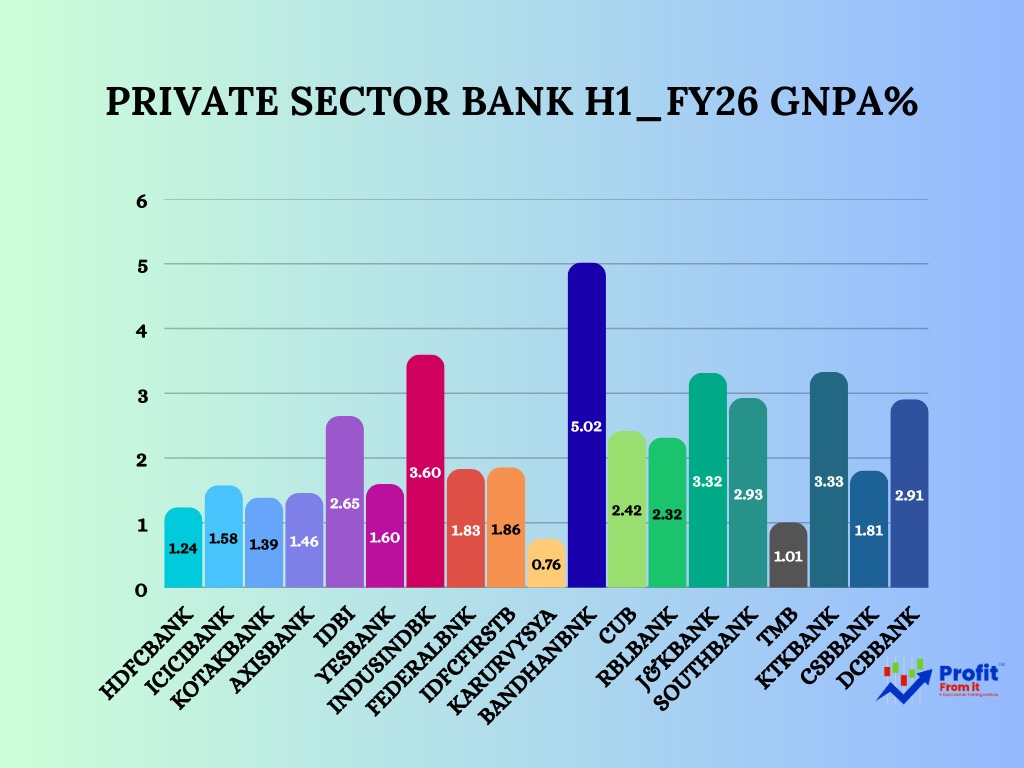

Industry GNPA (avg): ~1.86%

Market cap concentration: HDFC Bank and ICICI Bank together command ~65% of industry capitalization.

Market cap leadership is concentrated in HDFC Bank and ICICI Bank, together commanding ~65% of industry capitalization.

🏦 Core Quality Anchors

HDFC Bank ✅

H1 FY26: Sales +5.5%, Profit +4.6%

Q2 FY26: Sales -2.4%, Profit +10.0%

Deposits: ₹27,98,169 Cr | Advances: ₹27,65,109 Cr

GNPA: 1.24%

Market Cap: ₹15.4 lakh Cr (~40% industry)

Quality Take: Profit resilience at mega scale; defensive compounder.

Investor View: Anchor holding for stability and downside protection.

ICICI Bank ✅

H1 FY26: Sales +7.5%, Profit +9.2%

Q2 FY26: Sales +4.4%, Profit +3.2%

Deposits: ₹16,45,864 Cr | Advances: ₹14,92,161 Cr

GNPA: 1.58%

Market Cap: ₹9.9 lakh Cr (~26% industry)

Quality Take: Consistent dual growth, disciplined underwriting, no profit shocks.

Investor View: Best complement to HDFC Bank; reliable compounding at scale.

💡 Together, ICICI + HDFC form the strongest core portfolio duo, balancing growth and defense.

🌟 Emerging Quality Satellites

City Union Bank (CUB) 🌱

H1 FY26: Sales +16.0%, Profit +15.5%

Q2 FY26: Sales +15.2%, Profit +15.1%

Deposits: ₹56,680 Cr | Advances: ₹54,065 Cr

GNPA: 2.42%

Quality Take: Rare small-cap with clean, repeatable dual momentum.

DCB Bank 🌱

H1 FY26: Sales +19.2%, Profit +18.8%

Q2 FY26: Sales +13.3%, Profit +18.7%

Deposits: ₹52,974 Cr | Advances: ₹53,218 Cr

GNPA: 2.91%

Quality Take: Balanced growth and profit conversion; compounding-friendly.

CSB Bank 🌱

H1 FY26: Sales +32.7%, Profit +10.8%

Q2 FY26: Sales +37.0%, Profit +15.9%

Deposits: ₹34,261 Cr | Advances: ₹64,776 Cr

GNPA: 1.81%

Quality Take: Strong top-line prints; profit sustainability to be validated.

Karur Vysya Bank 🌱

H1 FY26: Sales +14.6%, Profit +17.5%

Q2 FY26: Sales +16.3%, Profit -88.1%

Deposits: ₹92,184 Cr | Advances: ₹54,153 Cr

GNPA: 0.76% (lowest among peers)

Quality Take: Excellent asset quality; profit volatility in Q2 needs monitoring.

⚠️ Watchlist & Underweights

Axis Bank, Kotak Bank, Federal Bank, RBL Bank ❌ – Profit contraction undermines quality; await normalization.

IndusInd Bank, Bandhan Bank ❌ – Volatile profit swings; avoid until stability proven.

IDFC First Bank, IDBI Bank ❓ – Growth-forward but profit discipline/base-effect heavy; monitor closely.

🌍 Global Peer Benchmarks

Large-cap compounders: JPMorgan Chase (US), DBS & OCBC (Singapore), HSBC (UK).

Digital-growth analogues: Nubank (Brazil), Tinkoff (Russia).

Regional specialists: Siam Commercial Bank (Thailand), Bank Rakyat (Indonesia).

📈 Long-term Growth Trajectory

System credit CAGR: 11–13% over next 20 years.

Private banks credit CAGR: 13–15%, with share rising to ~55–60%.

Profitability: ROA 1.6–2.2%, ROE 16–20%.

Quality drivers: Formalization, digital rails, deposit franchise strength, diversified fee income, and disciplined risk management.

📝 Investor Takeaway

Core Overweight: HDFC Bank → stability + compounding.

Underweight: Axis, Kotak, Federal, RBL, IndusInd, Bandhan → profit volatility.

📌 Final Word: For investors, HDFC Bank (quality growth anchor) offers the best balance of scale, consistency, and compounding. Selective small-cap satellites can add alpha, but discipline in sizing and monitoring is key.

Declaration: The information presented in this report is based on publicly available data and internal analysis as of H1 FY26. While every effort has been made to ensure accuracy, the insights are intended for informational purposes only and do not constitute investment advice.