📈 H1 FY26 Internet & Catalogue Retail Industry – Investor Insights

🌐 Industry Overview

The Internet & Catalogue Retail industry delivered healthy sales growth (+11.6% H1, +7.4% Q2) in FY26. However, profitability diverged sharply across companies, with Naukri’s margin expansion driving industry-level profit growth (+35.9% H1, +46.9% Q2) while peers faced compression.

💰 Market Capitalization Landscape

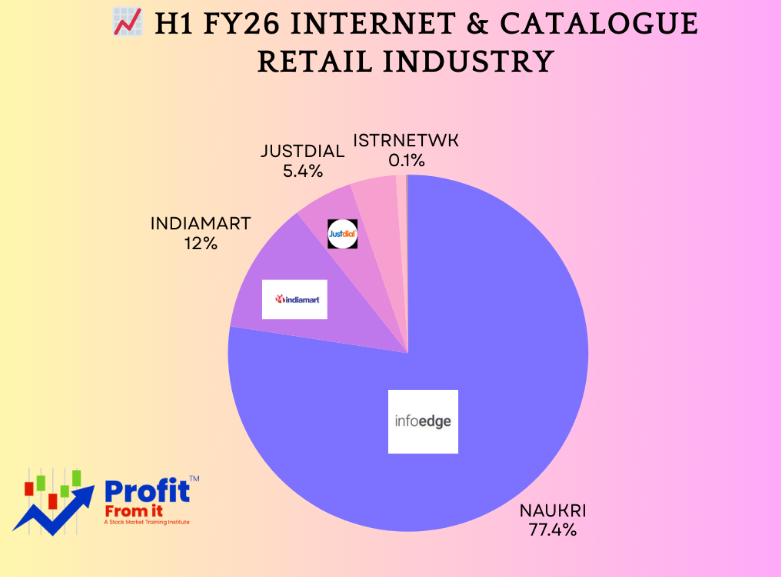

Naukri dominates with ₹86,451 Cr market cap, commanding 76.6% of industry share.

Indiamart follows at ₹13,907 Cr (12.3%), while JustDial holds ₹6,293 Cr (5.6%).

Smaller players (Crizac, Matrimony, Istrnetwk, Jupiterin, OlympTX, JSHL) collectively contribute less than 6% of industry capitalization.

📊 Implication: Industry performance is heavily concentrated in Naukri, making it the anchor for fund positioning.

📊 Comparative Growth Analysis

🔹 H1 FY26

Naukri: Sales +13.1%, Profit +101.2% 🚀

Indiamart: Sales +12.4%, Profit -5.2% ⚠️

JustDial: Sales +6.2%, Profit -5.4% ⚠️

Industry Aggregate: Sales +11.6%, Profit +35.9%

🔹 Q2 FY26

Naukri: Sales +5.7%, Profit +313% 🚀

Indiamart: Sales +12.7%, Profit -39.3% ⚠️

JustDial: Sales +6.7%, Profit -22.7% ⚠️

Industry Aggregate: Sales +7.4%, Profit +46.9%

📌 Observation: Naukri’s profit surge offsets declines in Indiamart and JustDial, sustaining industry-level earnings growth.

📉 Margin Dynamics

Naukri: Margin expanded from 19.7% → 35.0% (H1) and 9.2% → 35.9% (Q2) ✨

Indiamart: Margin compressed from 36.7% → 30.9% (H1) and 38.9% → 20.9% (Q2) ❌

JustDial: Margin fell from 52.2% → 46.5% (H1) and 54.2% → 39.3% (Q2) ❌

Industry: Margins improved in H1 but declined in Q2, reflecting mixed company-level trends.

⚖️ Weighted Impact Table (H1 FY26)

📌 Takeaway: Naukri alone explains nearly all of the industry’s profit growth, while peers dilute earnings momentum.

🎯 Strategic Positioning for Investors

Overweight Naukri (🚀): Margin expansion and profit momentum make it the clear driver of industry earnings.

Neutral Indiamart (⚖️): Strong sales but profitability drag; monitor cost structures.

Underweight JustDial (⚠️): Limited upside contribution, consistent margin pressure.

Satellite exposure to smaller names (🌱): Too small to materially impact industry aggregates; treat as opportunistic bets.

🌍 Global Internet Retail Industry

Amazon (FY25/26): Market cap ~$2.3 trillion; revenue ~$575 billion FY25. Net profit ~$30 billion, margins ~8–10%.

Alibaba (China): Market cap ~$200 billion; FY25 revenue ~$130 billion, profit ~$13 billion. Margins ~10%.

Pinduoduo (China): FY25 revenue ~$35 billion, profit ~$7 billion, margins ~20% (higher efficiency model).

Industry averages (global e-commerce): Gross margin ~47%, EBITDA margin ~20%, operating margin ~9%.

🛒 Unlisted Indian Giants

Flipkart (FY25): Revenue ₹82,787 Cr (~$10 bn), Loss ₹5,189 Cr. FY24 revenue ₹70,542 Cr, Loss ₹4,248 Cr.

Despite strong sales (boosted by Big Billion Days), profitability remains negative due to discounting and logistics costs.

Amazon India: Not separately disclosed, but India is one of Amazon’s fastest-growing markets. Globally, Amazon’s e-commerce sales exceeded $575 bn FY25, with India contributing significantly to growth.

🔑 Comparative Insights

Scale vs Profitability: Global leaders (Amazon, Alibaba) operate at massive scale with sustainable margins. Indian listed firms are smaller but show sharper swings in profitability due to margin volatility.

Flipkart vs Amazon India: Flipkart drives volume but remains loss-making; Amazon India benefits from global scale and AWS profitability cushioning retail margins.

Investor positioning:

Indian listed firms: Naukri is margin-resilient; Indiamart/JustDial face cost pressure.

Global giants: Amazon offers scale + profitability; Alibaba/Pinduoduo show regional strength.

Unlisted Flipkart: Growth engine but structurally loss-making—strategic exposure only via Walmart (parent).

📝 Conclusion

The Internet & Catalogue Retail industry in H1 FY26 is a story of sales resilience but profit divergence. With Naukri’s outsized contribution, industry-level earnings remain strong, but investors should be selective—focusing on margin-resilient leaders while staying cautious on peers facing cost pressures.

Research by: Kinjal Bhatt

Declaration: The information presented in this report is based on publicly available data and internal analysis as of H1 FY26. While every effort has been made to ensure accuracy, the insights are intended for informational purposes only and do not constitute investment advice.