✈️ H1/Q2 FY26 Tour & Travel Services Industry – Investor Insights

🌍 Industry Overview

The Indian Tour & Travel Services industry delivered mid-teens growth in H1 FY26:

Sales growth: +18%

Profit growth: +15%

Margins: Slight compression (H1 margin 13.0%, down 32 bps YoY)

Despite margin pressure, the industry continues to expand, driven by rising travel demand and digital adoption.

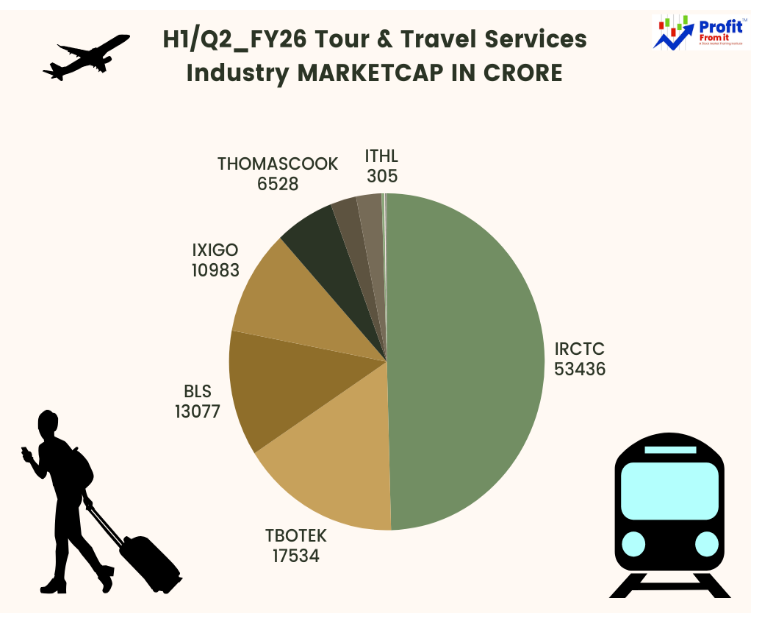

💰 Market Cap Concentration

Industry total: ₹108,155 cr

IRCTC: ₹53,730 cr (~50% of industry) – the anchor stock

Top 3 (IRCTC, TBOTEK, BLS): ~78% of industry market cap

Mid-caps (IXIGO, Yatra, Thomas Cook): high growth but smaller liquidity base

➡ IRCTC dominates, providing stability, while mid-caps offer tactical growth opportunities.

📊 Comparative Growth Snapshot

📉 Margin Dynamics

Expanding: IRCTC (+128–144 bps), Yatra (+209–103 bps)

Compressing: TBOTEK (-186 bps), BLS (-166 to -416 bps)

Stress: IXIGO slipped into negative Q2 margin

➡ Margin discipline separates quality plays (IRCTC, Yatra) from riskier growth bets (IXIGO, TBOTEK).

🧮 Quality Ratios: Debt-to-Equity Focus

➡ IRCTC and BLS are the most financially sound, with near-zero debt and strong liquidity.

Yatra and TBOTEK carry moderate leverage, while Thomas Cook is the most leveraged among peers.

🌐 Global Peer Benchmark

Booking Holdings (US): Growth ~12%, EBITDA margin ~30%

Expedia (US): Growth ~9%, margin ~15%

Trip.com (China): Growth ~15%, margin ~20%

MakeMyTrip (India): Growth ~20%, margin ~12%, EV/Sales ~8.3x

➡ Indian players (Yatra, BLS, IXIGO) are outpacing global peers in topline growth, but lag in margin quality.

IRCTC is closest to global benchmarks in efficiency.

🟢🟡🔴 Traffic-Light Positioning

🟢 Overweight / Core Holdings:

IRCTC – dominant, debt-free, margin leader.

BLS International – strong growth + profitability, low debt.

🟡 Monitor / Tactical Plays:

Yatra – explosive growth, small-cap risk.

TBOTEK – growth story, margin pressure.

🔴 Underweight / Avoid:

IXIGO – profit collapse, negative margins.

Thomas Cook – weak growth, higher leverage.

✅ Investor Recommendation

Core portfolio: IRCTC (stability, quality ratios)

Tactical exposure: Yatra (alpha potential, but liquidity risk).

Caution: TBOTEK (valuation/margin risk), IXIGO (profit collapse).

Avoid: Thomas Cook (leverage, weak fundamentals).

✨ Conclusion

The Tour & Travel Services industry is in a growth phase, but quality matters.

IRCTC remains the best investment from a stability and quality perspective.

BLS International is the best complement, offering strong growth with healthy margins and balance sheet strength.

Selective exposure to Yatra can add alpha, while caution is warranted on IXIGO and TBOTEK.

➡ For investors, the optimal strategy is a core holding in IRCTC with tactical bets in Yatra, ensuring balance between stability, growth, and quality.

📜 Disclosure

This note is for informational purposes only and does not constitute investment advice.