🎨 Indian Paint Industry: H1 FY26 Performance & Global Context

🏭 Industry Snapshot

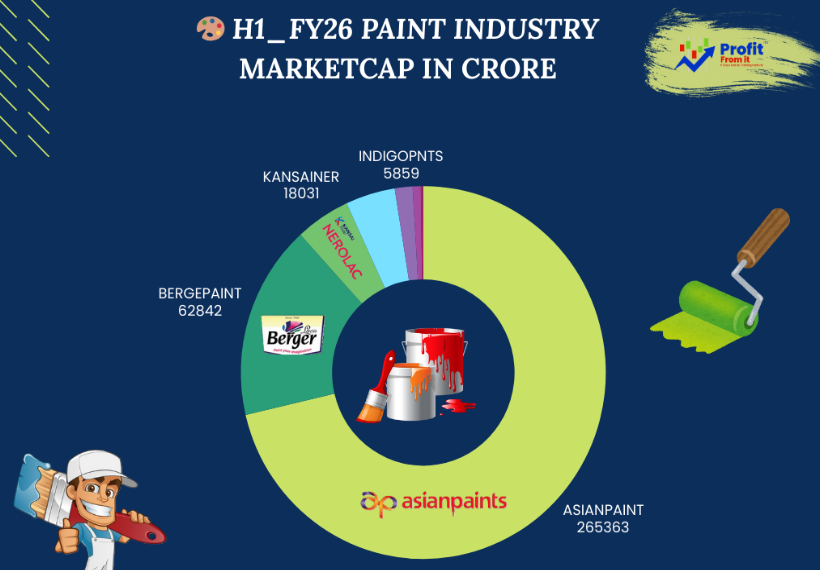

Total Market Cap: ₹386,562 Cr

Sales Growth (H1 FY26): +1.9%

Profit Growth (H1 FY26): +3.1%

Q2 FY26 Profit Growth: +19.9% (sharp rebound)

Long-term trajectory: 8–9% CAGR expected over the next decade, driven by housing, infra, and premiumization.

📈 Company Growth Performance

🔑 Highlights:

🏆 Asian Paints: Strong profit surge, margin expansion

⚠️ Berger & Akzo: Margin stress, profit declines.

📉 Kansai & Indigo: Stable, modest growth with improving profitability.

💹 Margin Trends

💎 Market Cap Concentration

📌 Observation: Industry is highly concentrated — Asian Paints + Berger = ~89% of total market cap.

🌍 Global Peer Comparison

🔮 Decadal Outlook

Base Case: 8–9% CAGR industry growth (value terms).

Upside: 10–12% CAGR if housing + infra cycles align.

Downside: 5–6% CAGR if commodity spikes or competition intensifies.

Structural Drivers: Urbanization, housing demand, infra build-out, premiumization, repaint cycle shortening.

Risks: Input cost volatility, competitive pricing wars, policy execution delays.

🎯 Investor Takeaways

Core Holding: Asian Paints (scale, margin expansion, profit surge).

Caution: Berger & Akzo (margin stress).

Recovery Play: Kansai Nerolac (steady, incremental margin gains).

Global Benchmark: Sherwin-Williams and Nippon Paint show how scale + service ecosystems sustain superior quality and margins.

✨ Conclusion:

The Indian paint industry continues to deliver resilient margins and faster growth than global peers, despite smaller scale. Asian Paints remains the anchor holding, Global leaders provide benchmarks in scale and diversification, but India’s structural housing and infra demand make domestic players uniquely positioned for compounding returns.

📜 Disclosure

This note is for informational purposes only and does not constitute investment advice.