TCS Q4 FY26 Analysis: The AI Growth Engine vs. Macro Headwinds

As the global macroeconomic landscape continues to test the resilience of the IT sector, Tata Consultancy Services (TCS) has delivered its Q4 FY26 numbers. While the broader demand environment remains cautious, TCS's aggressive pivot towards Enterprise AI and relentless operational efficiency tell a compelling story.

Let's break down the financials, analyze the management's tone, and determine if the current valuation offers a genuine margin of safety for investors.

The Snapshot

The 'Wow' Factor

The AI Hyper-Scale: Annualized AI Revenue crossed the $US\$ 2.3$ billion mark this quarter, proving that GenAI is moving from proof-of-concept to real-world billing.

Margin Expansion: Operating Margin soared to $25.3\%$ ($+70$ bps YoY for the full year)—touching a 4-year high despite severe macro volatility.

Blockbuster Order Book: TCS locked in a mammoth $US\$ 40.7$ billion TCV for FY26, with $US\$ 12$ billion secured in Q4 alone, anchoring immense forward visibility.

Client Mining Excellence: The company added 65 new clients in the $US\$ 1M+$ revenue band and 2 new clients in the $US\$ 100M+$ band YoY, showcasing tremendous pipeline conversion.

Operational KPI Table

Here is how TCS performed on its core industry-specific operating metrics:

Financial Deep Dive (Consolidated)

(Note: EBITDA is approximated by adding Segment Operating Results/Profit Before Unallocable Expenses to Depreciation).

Cost vs. Efficiency: A Masterclass in Optimization

TCS demonstrated exceptional operational rigor this quarter. While employee benefit expenses naturally scaled to ₹40,143 crore (up from ₹36,762 crore YoY) to sustain talent retention and build AI competency, management drastically optimized their external dependencies.

$$Operating\ Margin = \frac{Operating\ Income}{Total\ Revenue}$$

Cost of equipment and software licenses was ruthlessly slashed to ₹1,444 crore in Q4 (down from ₹2,748 crore YoY). This fierce cost-efficiency, combined with better utilization rates and high-margin AI integration, propelled the operating margin to a robust $25.3\%$. We love to see a company that defends its bottom line when top-line growth is challenged.

The Forward Curve

Management's tone during the earnings call was remarkably confident regarding their 'Build-Partner-Acquire' strategy, yet appropriately transparent about persistent macroeconomic softness in North America.

With a formidable $US\$ 40.7$ billion TCV booked in FY26, TCS is structurally shifting from legacy maintenance to high-yield "Infrastructure-to-Intelligence" transformations. The integration of high-margin acquisitions like Coastal Cloud and ListEngage, combined with mega strategic alliances (OpenAI, AMD, ABB), provides a strong tailwind. We project modest yet accelerating constant currency (CC) growth in H1 FY27, transitioning to mid-to-high single-digit revenue expansion by Q3 as macro headwinds potentially soften and AI platforms like TCS HyperVault begin to scale.

Valuation Guardrails

Let's run the math on the current valuation using the Reported (Ind AS) metrics:

$$EPS_{FY26} = ₹136.01$$

$$P/E = \frac{CMP}{EPS} = \frac{2588}{136.01} = 19.03x$$

Valuation Verdict: Historically Discounted.

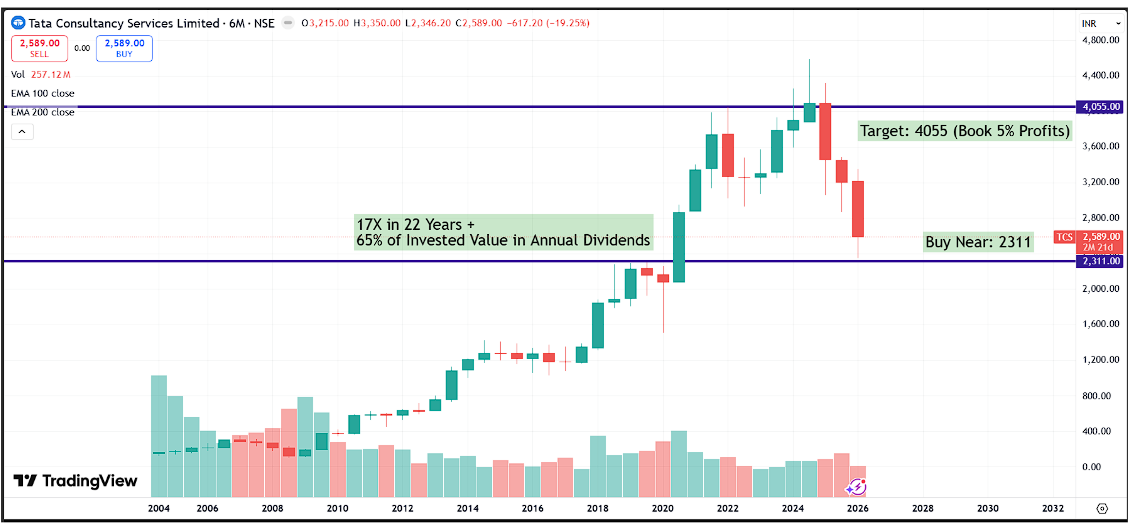

At $19.03x$ trailing earnings, TCS is still trading at a significant discount to its 5-year median P/E, which typically hovers around $26.8x$. Buying an elite, cash-rich IT giant with a $25\%+$ operating margin at roughly $19x$ earnings provides an unparalleled margin of safety for value-conscious allocators.

The Ownership Structure

Changes in shareholding patterns often reveal the "smart money" sentiment:

Promoters: Holding remains steadfast at $71.77\%$ with $0.00\%$ pledged shares—a hallmark of the Tata Group's governance integrity.

FIIs: Foreign Institutional Investors slightly increased their stake to $10.37\%$, signaling returning institutional confidence in TCS's AI narrative.

DIIs/Mutual Funds: Trimmed slightly to $5.52\%$, rebalancing across sectors, while Public holding remains stable at $~4.98\%$.

The Advisory Note

Strategic Outlook: TCS is executing a textbook strategy to dominate the upcoming AI super-cycle. Their proactive workforce upskilling (270k+ AI-trained employees) and aggressive partnerships make this a core, sleep-well-at-night portfolio holding for the next decade.

Tactical Opportunity: The current multiple compression creates a highly asymmetric risk-reward scenario. Furthermore, the Board has recommended a final dividend of ₹31/share (bringing the FY26 total to a massive ₹110/share). This creates a highly attractive yield buffer while you wait for the broader IT sector re-rating to play out.

Disclosure: TCS is part of our main fund and NayaBharat Investment Basket given below:

https://profitfromit.co.in/baskets_pms/investment/baskets

Financial Disclosure: This research note is for educational and informational purposes only. It does not constitute localized financial advice. TCS is part of our Main fund and in our NayaBharat Basket.