Tata Elxsi Q4 FY26 Analysis: Resilient Revenue Growth vs. The Exceptional Cost Hurdle

As the curtains close on FY26, Tata Elxsi continues to demonstrate its dominance in the ER&D (Engineering Research and Development) space. While the top-line growth remains healthy, a significant one-time exceptional item related to the New Labour Codes has impacted the bottom-line optics this quarter. We dive deep to see if the "Design Digital" story still holds its premium.

📊 The Snapshot

🌟 The 'Wow' Factor

Revenue Milestone: Operating revenue reached ₹993.81 Cr, showing strong sequential momentum of 4.2% QoQ and nearly hitting the 1,000 Cr mark.

Dividend Bonanza: The Board has recommended a generous final dividend of ₹75 per share, reflecting management's confidence in long-term cash flows.

Profit Resilience: Despite a massive one-time provision, the company reported a Net Profit of ₹220 Cr, showcasing the high-margin nature of its core design services.

Exceptional Transparency: A one-time provision of ₹95.69 Cr for New Labour Codes was recognized this quarter. Excluding this, operational profitability reached record highs.

📈 Operational KPI Table

🔍 Financial Deep Dive (Consolidated)

*Note: Q4 FY26 PAT includes a mandatory one-time exceptional provision of ₹95.69 Cr. On a normalized basis, the bottom-line growth is even more robust than the reported 27.9% YoY increase.

Cost vs. Efficiency: The jump from ₹172 Cr (Q4FY25) to ₹220 Cr (Q4FY26) represents a stellar 27.9% YoY growth in net profit. This was achieved despite the ₹95.69 Cr provision, highlighting a significant expansion in operational efficiency and higher-value project mix compared to the previous year.

🚀 The Forward Curve

Based on management guidance and the current deal pipeline:

Next 2 Quarters: We expect a revenue CAGR of 3-4% per quarter as large deals in the pipeline begin to scale.

Growth Drivers: Continued deal wins in Software Defined Vehicles (SDV) and a recovery in the Media & Communication vertical (up 1.2% QoQ) will provide the necessary tailwinds.

Margin Guidance: We expect margins to bounce back to the 26-28% range in Q1 FY27 once the legislative one-time costs are behind us.

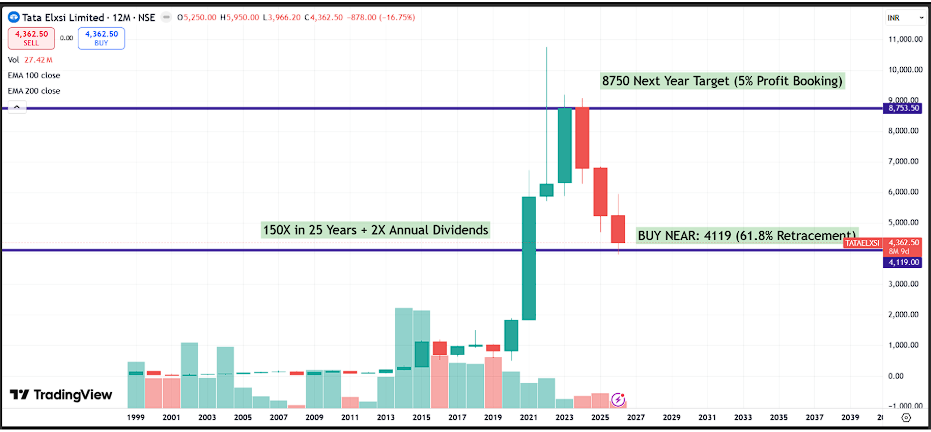

🛡️ Valuation Guardrails

Current P/E: ~31x (Based on FY26 earnings).

5-Year Median P/E: 48.5x.

Category: Significantly Undervalued. The company is trading well below its 5-year historical average P/E, offering a rare entry point into a high-growth Tata group entity.

🤝 Shareholding & Integrity

Promoter Stake: Remains steady at 43.92%. No shares are pledged.

FII/DII Activity: Slight increase in DII holding (+0.45%), suggesting domestic institutional confidence in the structural story.

Management Tone: Transparent. By taking the full hit of the Labour Code provision in a single quarter, management has "cleared the decks" for a high-growth FY27 without lingering liability overhangs.

💡 The Advisory Note

Strategic (Long-term): Tata Elxsi remains a top-tier play on the digitisation of the physical world. Their deep-rooted expertise in Automotive and Medical Devices creates a moat that traditional IT services lack.

Tactical (Short-term): Don't let the "exceptional item" headlines distract you. The 27.9% YoY PAT growth is the real story here. The stock remains a "Buy on Dips" for long-term compounding.