🔋 India Energy Sector Outlook (FY 2025–2035): Where the Next Decade is Headed

India is in the midst of an energy revolution. With an ambitious vision of achieving net-zero emissions by 2070, the country is rapidly transitioning to renewables while modernizing its infrastructure. If you're an investor eyeing India’s energy sector, this blog is your roadmap to future-proof opportunities through 2035.

🔍 Key Current Highlights (FY 2023–24)

📊 Energy Supply & Consumption

Total Primary Energy Supply (TPES) grew by 7.8%, reaching 9,03,158 KToE.

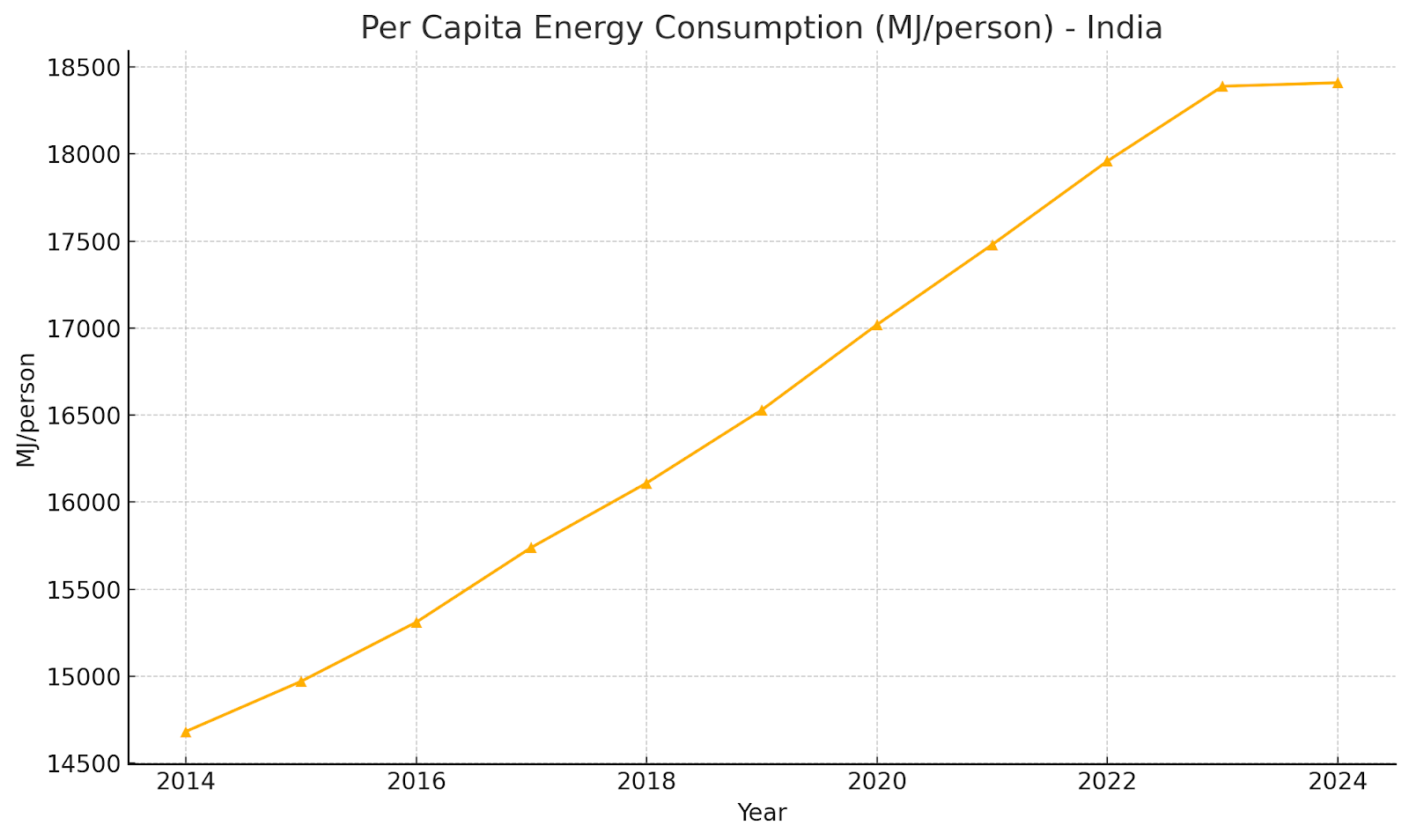

Per capita energy consumption increased to 18,410 MJ/person, with a CAGR of 2.55% over the past decade.

⚡ Electricity Generation

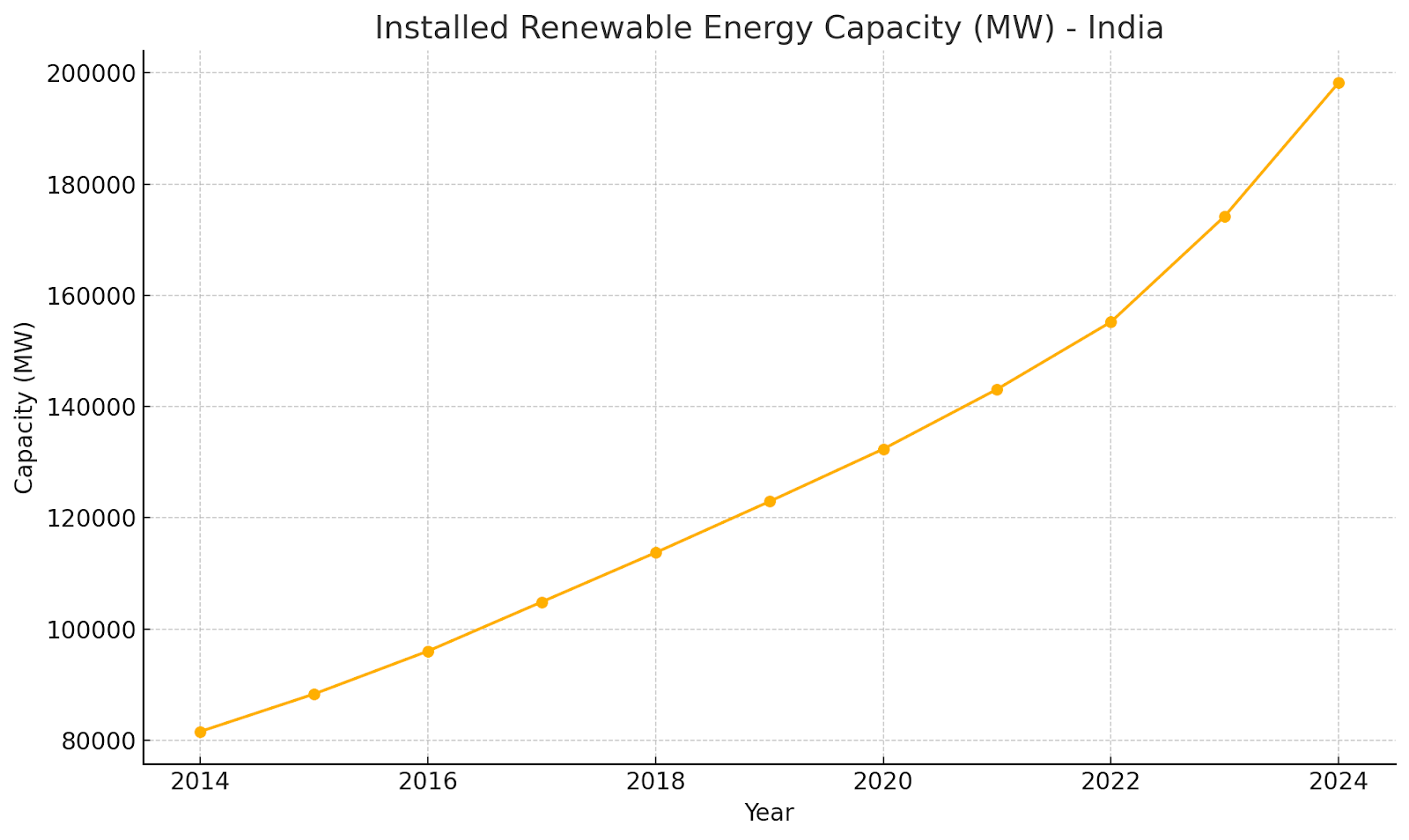

Renewable energy installed capacity grew from 81,593 MW in FY15 to 1,98,213 MW in FY24 — a CAGR of 10.36%.

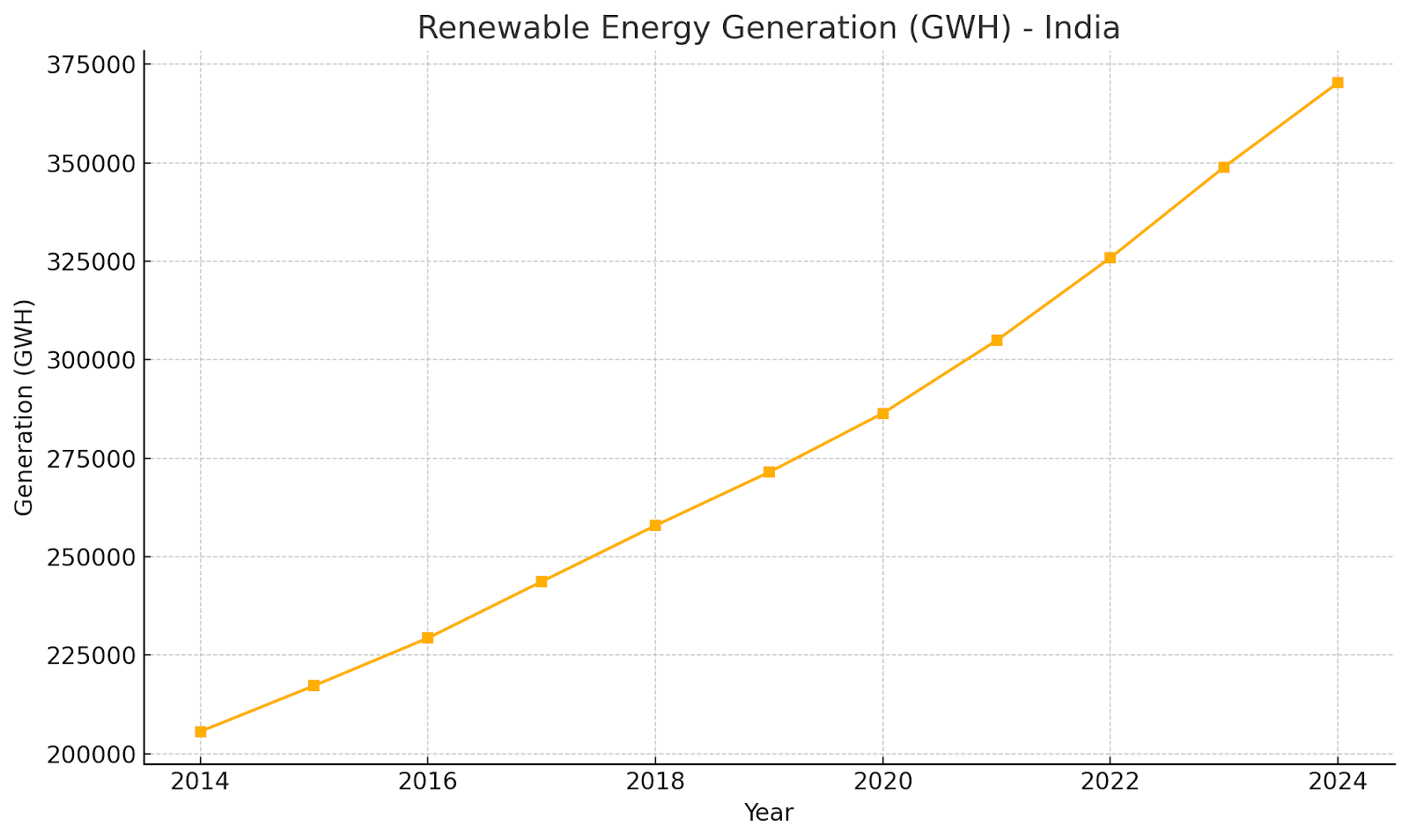

Renewable electricity generation rose from 2,05,608 GWH in FY15 to 3,70,320 GWH in FY24 — CAGR: 6.76%.

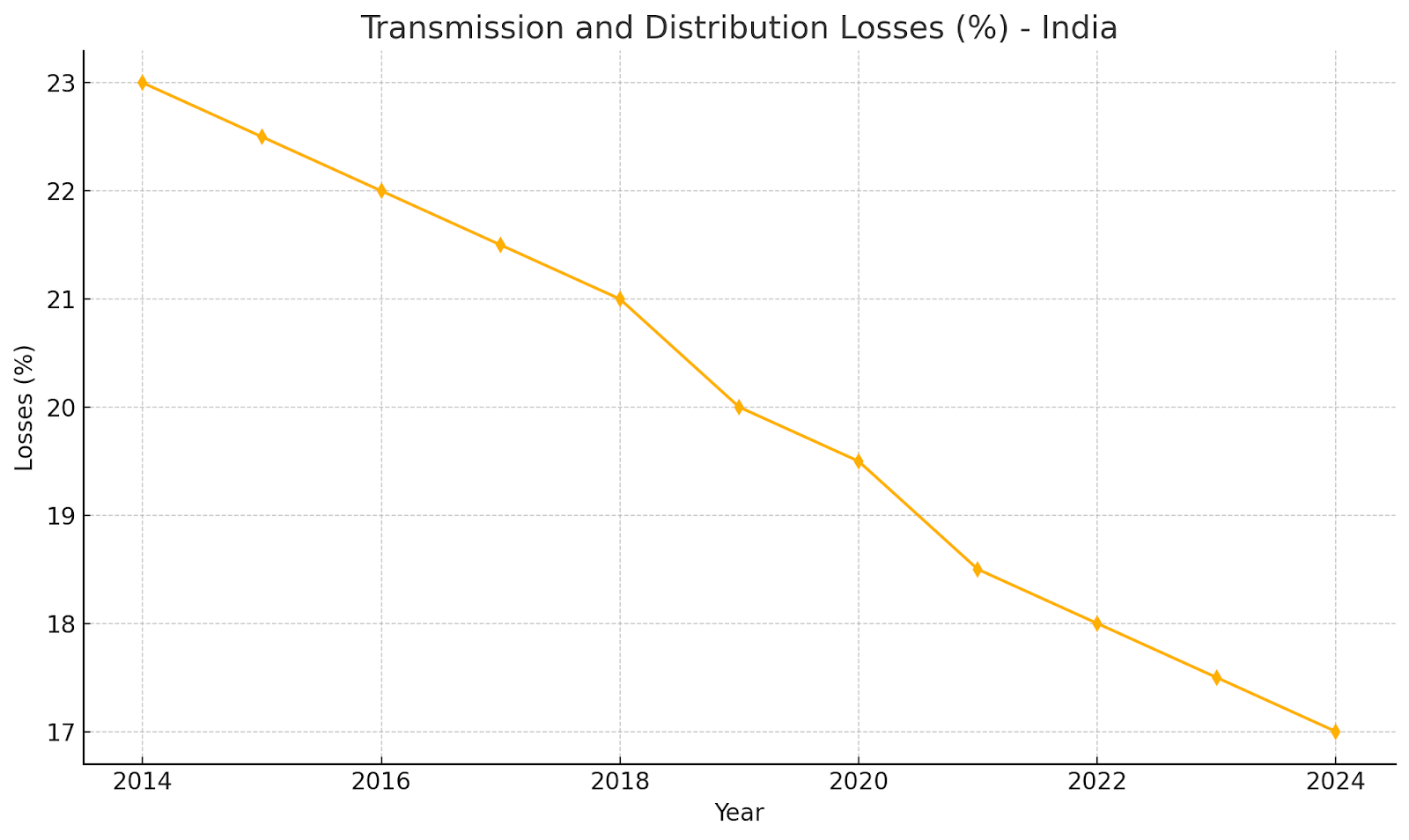

T&D losses improved significantly: down from 23% to 17% in the last decade.

🏭 Sector-wise Energy Use

Industry remains the dominant energy-consuming sector:

Consumption grew from 2,42,418 KToE (FY15) to 3,11,822 KToE (FY24).

🔮 Projections and Trends to FY 2035

🌞 Top Growth Segment: Renewables

India's renewable energy potential is pegged at ~2,109 GW, with:

Wind: 55% (~1,163 GW)

Solar: 35% (~749 GW)

Hydro & Others: ~197 GW

Projection for FY 2035:

Installed renewable capacity could exceed 500 GW, supported by:

Government targets (Net Zero by 2070, 500 GW non-fossil by 2030)

State-level implementation (Rajasthan, Maharashtra, Gujarat, Karnataka lead)

📈 Growth KPIs by Segment

🌍 Sector Growth Snapshot

India's energy ecosystem has seen phenomenal growth across multiple metrics:

📈 Visual Insights

1. Installed Renewable Energy Capacity (MW)

2. Renewable Energy Generation (GWH)

3. Per Capita Energy Consumption (MJ/person)

4. Transmission & Distribution Losses (%)

🚀 Sub-Sectors Poised for Growth

📊 Company KPI Comparison (FY24)

📌 Key Insight:

🔍 Waaree Energies stands out with a Debt-to-Equity ratio of just 0.2, signaling robust solvency — a major strength for a capital-intensive business.

🔍 IREDA's D/E is higher because it's a lending institution (NBFC), which is normal and healthy in that context.

🔍 Companies like Suzlon and Reliance have notably improved solvency.

🔍 Company like Powergrid Stable regulated returns.

🔍 Hydro Power Company like NHPC Cash-rich PSU with balanced leverage, but miss the sales growth.

🔍 Diversified Company like Reliance with balanced debt & consistent in Profits.

📊 Suggested FY 2035 Goals for Investors

💡 Investor Takeaways

Top Opportunities: Solar, Green Hydrogen, EV Infra, Renewable Finance

Top KPIs to Watch: Revenue CAGR, ROE, Net Profit Margin, D/E Ratio

Strategy Tip: Diversify across manufacturing, power generation, and finance

Policy Tailwinds: Net Zero 2070 target, 500 GW non-fossil by 2030, PLI schemes

📌 Final Word

India’s energy transformation is a multi-decade megatrend. As capital flows toward clean and scalable solutions, early-stage investments in leading and emerging players can generate long-term alpha.