Investor Snapshot ⚡

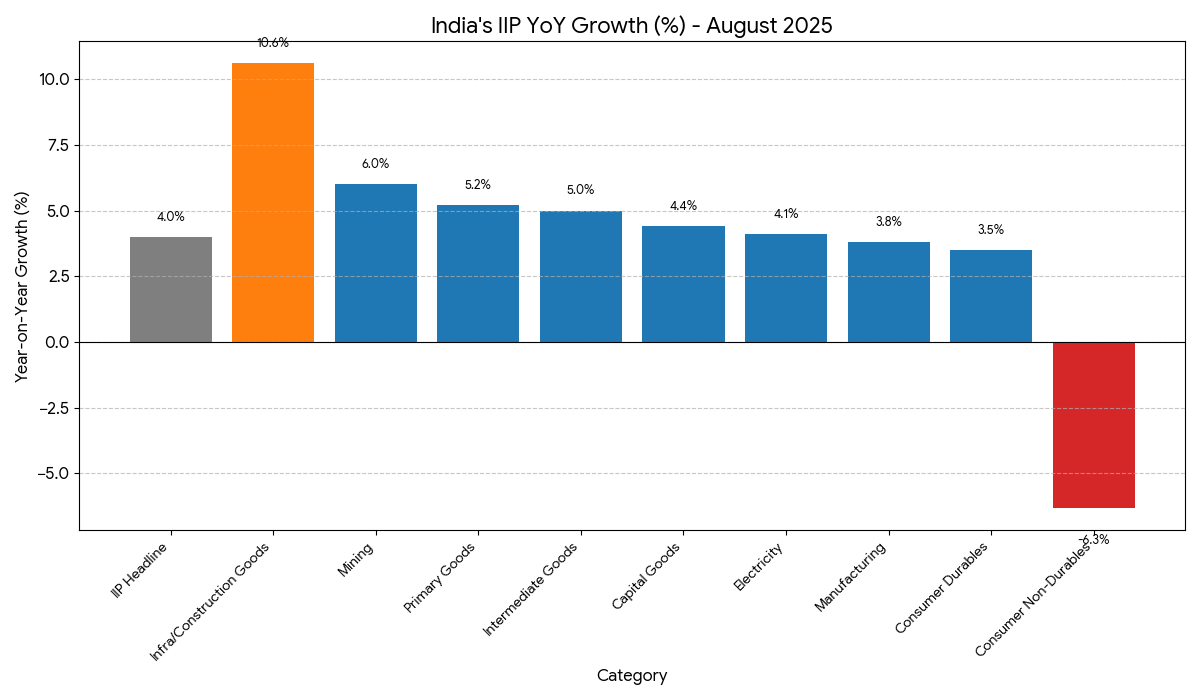

Headline IIP: +4.0% YoY in Aug-2025; better than July’s 3.5%.

By Sector: Mining +6.0%, Manufacturing +3.8%, Electricity +4.1%.

Use-based: Infra/Construction goods +10.6% (star performer), Primary +5.2%, Capital +4.4%, Intermediate +5.0%; Consumer durables +3.5%, Consumer non-durables −6.3%.

Big Movers (Manufacturing): Basic metals +12.2%, Motor vehicles +9.8%, Electrical equipment +11.4%; Weak spots include Pharma −9.2%, Printing −16.3%, Other manufacturing −11.5%.

What moved the needle 🧠

Infrastructure flywheel is spinning 🏗️

Infra/Construction goods up 10.6% → signals ongoing project execution (roads, urban, utilities). Knock-on demand supports metals, cement, electricals, capital goods.

Commodity-linked uptick 🔩

Basic metals +12.2% with items like MS slabs, HR coils/sheets, pipes contributing. This pairs well with infra momentum.

Auto ecosystem healing 🚗

Motor vehicles +9.8% led by components, axles, commercial vehicles. Freight & capex cycles help CVs; replacement & festive pipelines help PVs/2W.

Energy products steady ⛽

Coke & refined petroleum +5.4% with diesel, petrol, LPG lifting output—consistent with mobility & logistics activity.

Consumption is a tale of two wallets 🛍️

Consumer durables +3.5% (discretionary, urban-led) vs Consumer non-durables −6.3% (everyday staples)—a soft spot that hints at mixed rural demand or inventory rationalisation.

Not all healthcare linked 💊

Pharma −9.2% (on a high base and product mix effects). One month doesn’t make a trend; monitor export order books & pricing.

The economy’s at the gym—legs (infra) day is clearly done; arms (staples) need a little protein. 💪🍗

Key data points (Aug-2025 vs Aug-2024) 📊

General IIP: 151.7 vs 145.8 (YoY +4.0%).

Sector indices: Mining 113.5, Manufacturing 151.6, Electricity 221.1.

Use-based indices: Primary 148.9, Capital 112.1, Intermediate 170.4, Infra 200.8, Consumer durables 134.4, Consumer non-durables 132.8.

Top manufacturing contributors: Basic metals +12.2%; Petroleum products +5.4%; Motor vehicles +9.8%.

(Note: Aug-2025 are Quick Estimates and subject to revision as per IIP policy.)

Positives ✅

Capex momentum: Infra goods double-digit growth + strength in metals/electricals → supportive for core industrial cycle.

Auto chain recovery: Wider beneficiary set across OEMs, CVs, and component suppliers.

Energy throughput: Petroleum products output up—aligns with mobility & freight firmness.

Negatives / Watchpoints ⚠️

Staples softness: Non-durables contraction (−6.3%)—track rural cashflow, MSP realisations, and monsoon after-effects.

Selective sector drags: Pharma, printing/media, “other manufacturing” show double-digit declines—monitor order visibility and pricing pressures.

Revisions risk: Quick Estimates undergo revision; avoid over-fitting portfolios to one month.

How to interpret for investments (Beginner → Pro) 🧭

Beginner (Keep it simple):

Prefer sectors aligned to infra & autos.

Avoid chasing every monthly zig-zag; look for 3–6 month confirmation.

Intermediate (Blend fundamentals + IIP):

Cross-check IIP leaders with sales/EBITDA momentum and working capital turns.

For metals/cement/electricals, track order books and capacity utilisation.

Advanced (Cycle & valuation discipline):

Screen: High correlation to infra/auto cycles and improving ROCE.

Validate: Forward earnings (12–24m) vs historical PE/PBV bands; avoid paying peak-cycle multiples.

Hedge: Staples/healthcare weakness → don’t underweight defensives blindly; use staggered allocation.

What to expect next (1–2 quarters) 🔭

Infra carry-through likely as projects execute; supportive for metals, cement, electricals, industrials.

Autos: Festive demand + replacement cycle could keep volumes healthy, esp. in CVs & PVs.

Staples: Watch for a mean-reversion if rural incomes stabilise; base effects could normalise the sharp negative print.

Pharma: Expect choppiness; track export pricing and regulatory updates rather than just IIP.

Action plan 📝

Build a watch-list:

Core cyclicals: Metals, Cement/Building Materials, Electrical Equipment, Capital Goods, CV-linked autos.

Select defensives: Quality staples & healthcare names to balance beta.

Stagger entries in leaders; use pullbacks.

Track the next IIP release (Oct 28, 2025) for confirmation.

Review company results and order-book disclosures alongside IIP for conviction upgrades/downgrades.

Disclosure: This is education-only, not a buy/sell recommendation. Data sourced from the official IIP press release (MoSPI). Figures are Quick Estimates and may be revised.