Rate Cut, Higher Growth, and Lower Inflation – What Does it Mean for Your Portfolio?

Date: December 5, 2025 | By: Profit From It

The Reserve Bank of India’s (RBI) Monetary Policy Committee (MPC) wrapped up its December review with a unanimous, market-moving decision. The message is clear: the Indian economy is in a 'Rare Goldilocks Period', boasting high growth and exceptionally low inflation.

This is the data-driven breakdown of the key announcements and the correlating strategy for you, the astute investor.

🔔 Key Decisions: The Investor's Cheat Sheet

Humor Alert! 💡 The RBI essentially told us the economy is like that perfectly cooked dish: "Not too hot (inflation is low) and not too cold (growth is robust)!" A rare treat in the global kitchen.

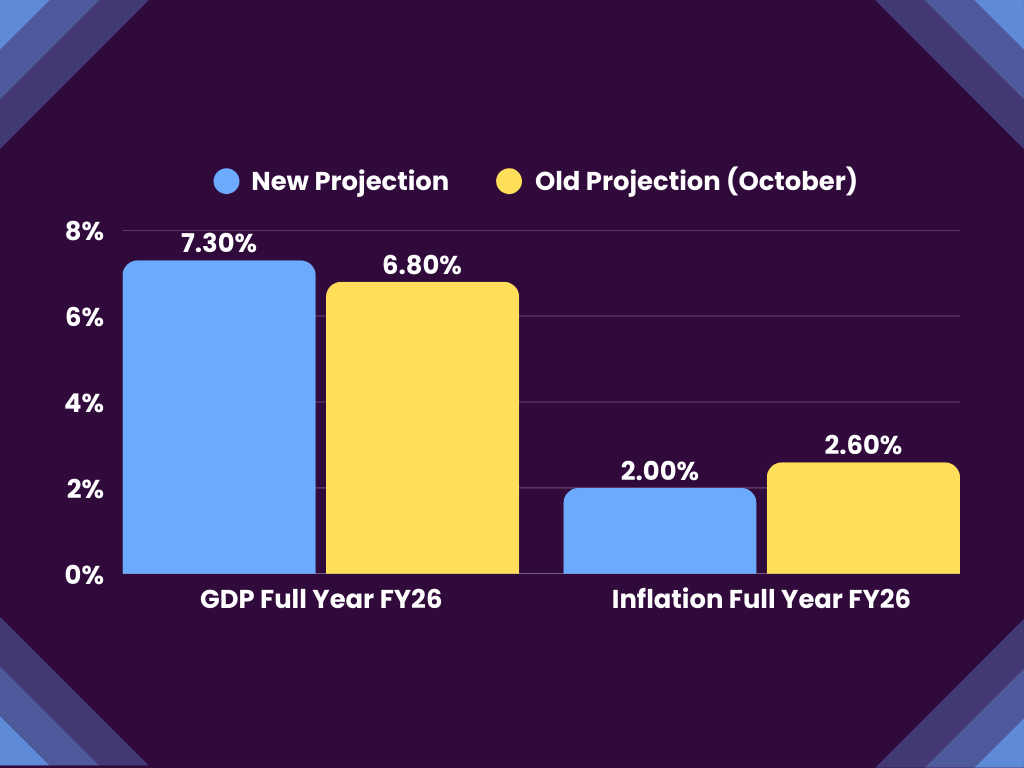

📈 Economic Projections: The New Base for Analysis

The MPC significantly revised its key forecasts, giving investors a strong new baseline for fundamental valuation.

Real GDP Growth Outlook (FY 2025-26)

Growth Drivers:

Resilient domestic demand, driven by festival spending and GST rationalisation.

Healthy rural demand and recovering urban demand.

Strong private investment, as non-food bank credit expands.

Consumer Price Index (CPI) Inflation Outlook (FY 2025-26)

Inflation Insight: The decline is faster than anticipated, largely due to a correction in food prices. Core inflation is also contained. This benign inflation outlook gives the RBI policy space to support growth.

💰 Additional Measures: Liquidity Boost

Beyond the rate decision, the RBI announced two major liquidity-injecting measures:

OMO Purchases: ₹1,00,000 crore (One Lakh Crore) Open Market Operations (OMO) of government securities this month.

Forex Swap: A 3-year USD/INR Buy Sell swap of USD 5 billion.

These actions are designed to inject durable liquidity into the system, ensuring smooth monetary transmission.

💡 Investor Correlation: How to Position Your Portfolio

This combination of a rate cut, higher GDP projection, and lower inflation is highly constructive for the stock market, especially for credit-sensitive sectors.

The Bottom Line for Investors

The RBI has delivered a policy that prioritizes growth momentum without compromising its inflation mandate. This environment of lower interest rates combined with strong economic forecasts (upgraded GDP) is highly supportive of equity markets. We advise investors to continue focusing on Fundamental Analysis, paying close attention to companies with strong market share in the domestic consumption and credit cycle space.

⚠️ Disclaimer ⚠️

Disclosure/Disclaimer: This post is for informational and educational purposes only. It is based on the Reserve Bank of India's Monetary Policy Committee announcements made on December 5, 2025, and our professional investment analysis. It should not be considered as personalized investment advice. Stock market investing involves risk. We are SEBI Registered Investment Advisor. The information provided is subject to change based on evolving economic and market conditions.