📊 The Inflation Rebound: Contextualizing the November 2025 CPI Data

Topic: Analyzing the November 2025 CPI Data: A Reversal of the Recent Trough and Its Implications for Investors

Humor Hook: Don't panic! It's just a little bit of inflation... like finding one extra raisin in your cookie. We'll show you where that raisin came from and what it means for your portfolio.

The latest Consumer Price Index (CPI) numbers for November 2025 show a calculated rebound in overall inflation, following the significant drop seen in the preceding months. For the astute investor, this signals a need to re-evaluate sectors and strategies, specifically asking: Is this the beginning of a new inflationary cycle, or merely a statistical correction?

Let's dive into the core data from the National Statistics Office (NSO) press release and translate it into actionable investment knowledge.

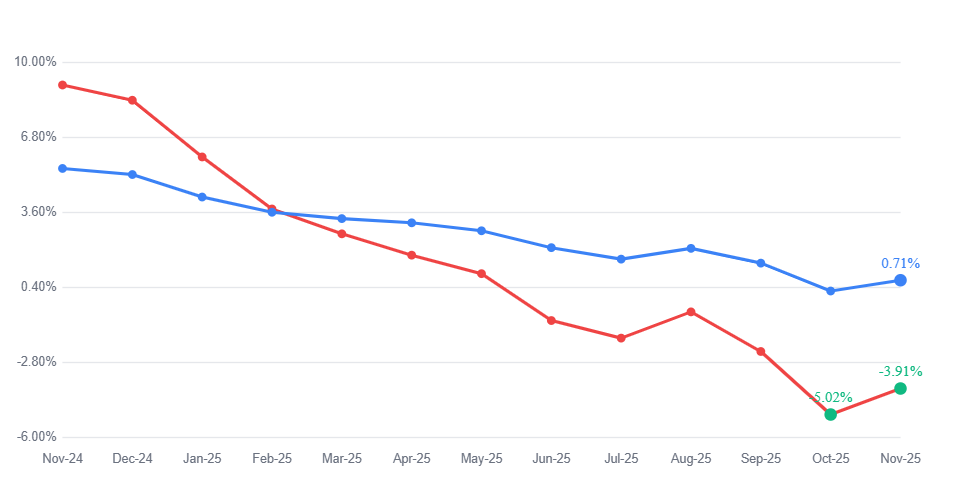

📈 Key Inflation Insights: Headline & Food Inflation - The Rebound Effect

The most crucial takeaway is the upward shift in both key inflation metrics, pulling away from the recent lows:

Headline Inflation Trend: The year-on-year CPI (Combined) inflation rose by 46 basis points (bps), climbing from 0.25% in October to 0.71% in November 2025. When viewed against the multi-month decline (from 9.04% in Nov-24 down to 0.25% in Oct-25), this change appears to be a natural reversal of the recent sharp moderation.

Food Inflation Trend: The Consumer Food Price Index (CFPI) remains in deflationary territory (-3.91% year-on-year) but saw a dramatic increase of 111 bps compared to October's -5.02%. This significant narrowing of deflation is the primary catalyst driving the headline CPI increase.

🥕 What Drove the Rebound? (Core Analysis)

The NSO press release explicitly attributes the increase in headline and food inflation to the rise in inflation of key food items and fuel: Vegetables, Egg, Meat and fish, Spices and Fuel and light.

Vegetables: While still in massive deflation (-22.20% combined), this rate is narrowing, pulling the CFPI upward.

Rural vs. Urban Disparity: The rural sector's CPI shifted from deflation (-0.25% in Oct-25) to positive inflation (0.10% in Nov-25) , indicating that cost pressures are returning to the rural economy.

🍎 Major Drivers & Key Item Inflation

(Rest of the original analysis, with updated citations for clarity.)

1. Description with Highest Inflation (Y-o-Y, Combined)

2. Descriptions with Lowest Inflation (Deflation)

3. Most Weighted Items/Groups

The CPI basket's biggest influences are:

Food and beverages: 45.86% weight

Miscellaneous: 28.32% weight (includes Health, Transport, Education)

Cereals and products: 9.67% weight

🌎 State-Level Inflation: Highs and Lows

For localized investment decisions, analyzing regional inflation is key.

Kerala has the highest inflation, driven significantly by its rural sector (9.34%). Conversely, states like Bihar and Assam are experiencing deflation.

💡 Impact on Stock Market Investing & Related Sectors

As an investor, the primary focus is translating this economic data into stock market strategy.

✅ Conclusion: An Expected Correction, But Watch Food

The November 2025 CPI data is best viewed as a correction or rebound from the exceptionally low inflation levels seen in October, driven primarily by the narrowing of food deflation. The rise from 0.25% to 0.71% is less concerning than the 111 bps jump in food prices, which signals that the steep discounts on vegetables and pulses are ending.

Investors should pivot their strategies to account for the re-emergence of cost pressures in the food basket, favoring companies with durable pricing power, and maintaining exposure to inflation-hedging assets like precious metals.

📜 Disclaimer

This analysis is based solely on the official press release of the National Statistics Office (NSO) and is for informational purposes only. It is not investment advice. Stock market investing involves risk. Always conduct your own analysis before making any investment decision.