🛡️ HDFC Life Insurance: Long-Term Investment Analysis for FY2026 & Beyond

🏢 Company Overview

HDFC Life Insurance Company Limited, one of India’s leading private life insurers, offers a robust portfolio of individual and group insurance solutions. Founded in 2000 as a joint venture between HDFC Ltd. and Standard Life, the company has consistently evolved to cater to India’s growing middle-class needs for financial protection and wealth creation.

🌍 Industry Landscape

India’s life insurance industry is at a transformative stage:

Insurance penetration in India (Life) is just ~3.2%, offering huge untapped potential.

The industry is expected to grow at a CAGR of 12–15% over the next decade driven by:

Rising middle-class income

Higher awareness of protection needs

Digital channel growth

Regulatory push for term insurance and annuities

📈 Historical Performance Snapshot

🔍 Observations:

Gross Premium has grown 12x over 15 years.

Profit has turned from negative in early years to a sustainable ₹1,700+ Cr range.

Profit margins peaked in FY2014–2016 and have gradually normalized to ~2.5–3.8%.

📊 Latest Q1 FY26 Results Highlights

🔍 Segmental Cost Breakdown – Q1 FY26

Actuarial Liability: ₹17,404 Cr (📈 +19%)

Commission: ₹1,752 Cr (📈 +19%)

Employee Benefit: ₹880 Cr (📈 +26%)

🔮 FY26 and Long-Term Growth Estimates

💰 Valuation Analysis – PE & PBV Bands

🔎 Historical PE & PBV Ranges:

PE Range (FY18–TRAIL FY26): 53x to 120x

PBV Range (FY18–TRAIL FY26): 7x to 21x

📊 Estimated Price Ranges Based on EPS & Book Value:

🧠 Portfolio Weighting Strategy

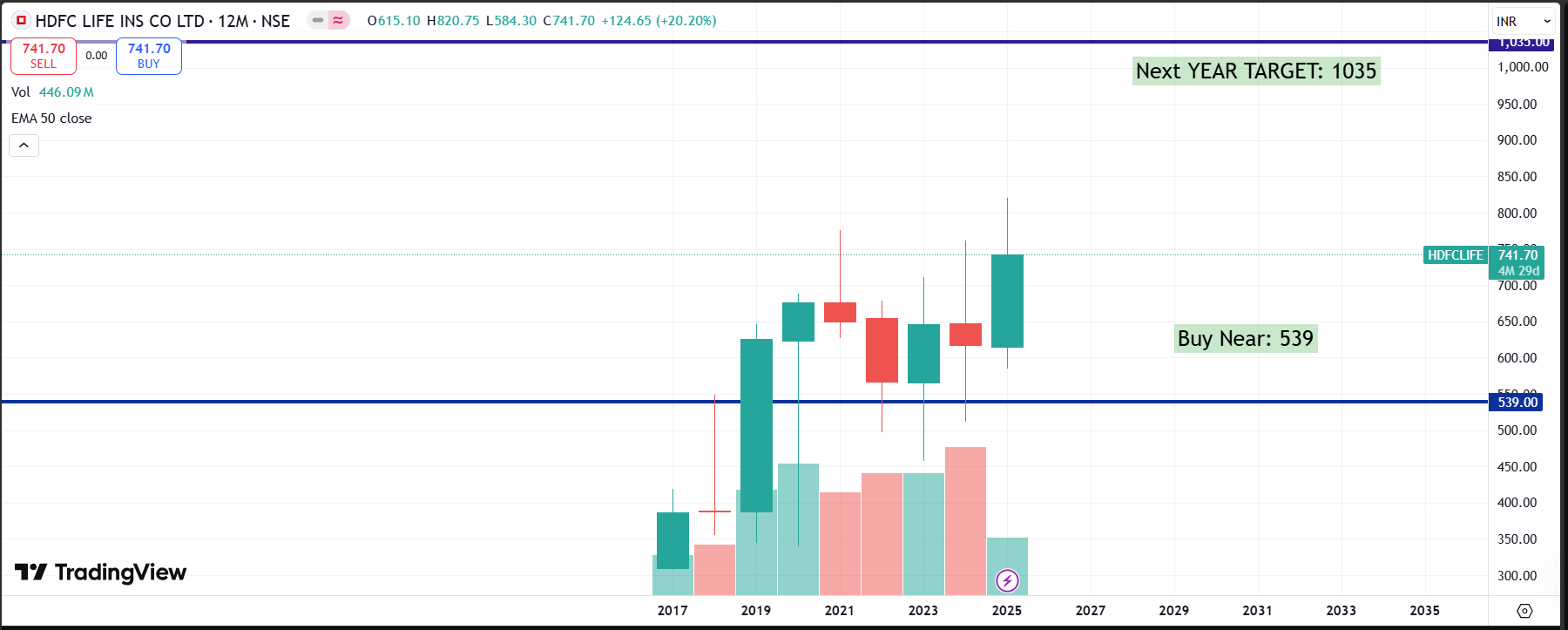

📉 Technical View

📌 CMP: ₹742

📈 Uptrend support near ₹539

🎯 Target at ₹1035

🧾 Conclusion: Is HDFC Life a Long-Term Compounder?

✅ Strengths:

Consistent premium growth

Expanding margins post FY23

Strong brand trust & distribution via HDFC ecosystem

Structural industry tailwinds

⚠️ Risks:

Margin compression due to rising actuarial liabilities

Competition from other large insurers & digital players

Regulatory changes in tax benefits or distribution commissions

🎯 Investor View:

With a 15% CAGR expected in profit and premium, a strong presence in a structurally growing industry, and normalization of margin trends, HDFC Life remains a core portfolio stock for long-term investors with a 5–10 year horizon.

Faiorvalue: HDFCLIFE

📢 Disclosure

This blog is for educational purposes only. The views expressed are unbiased and based on historical data and forward estimates. Investors must conduct their own research before making investment decisions.