IndiGo Airlines: Investment Story ✈️

✨ About IndiGo

IndiGo, owned by InterGlobe Aviation Ltd., is India’s largest airline. It follows a low-cost carrier model — meaning it keeps fares low by running a young fleet, keeping costs tight, and flying frequently.

🏢 Headquarters: Gurugram, India

🌍 Destinations: 91 domestic + 41 international (as of June 2025)

🚀 Fleet: 416 aircraft, including Airbus A320/321s, ATRs, and freighters

🎯 Focus: On-time flights, affordable fares, and expanding its reach

📈 Industry Outlook

Why this matters: India is one of the fastest-growing air travel markets in the world.

Rising middle-class incomes + tourism boom = more passengers each year.

Government’s regional air connectivity scheme is opening new smaller airports.

Competition exists (Air India, Vistara, Akasa), but IndiGo’s 60%+ market share keeps it far ahead.

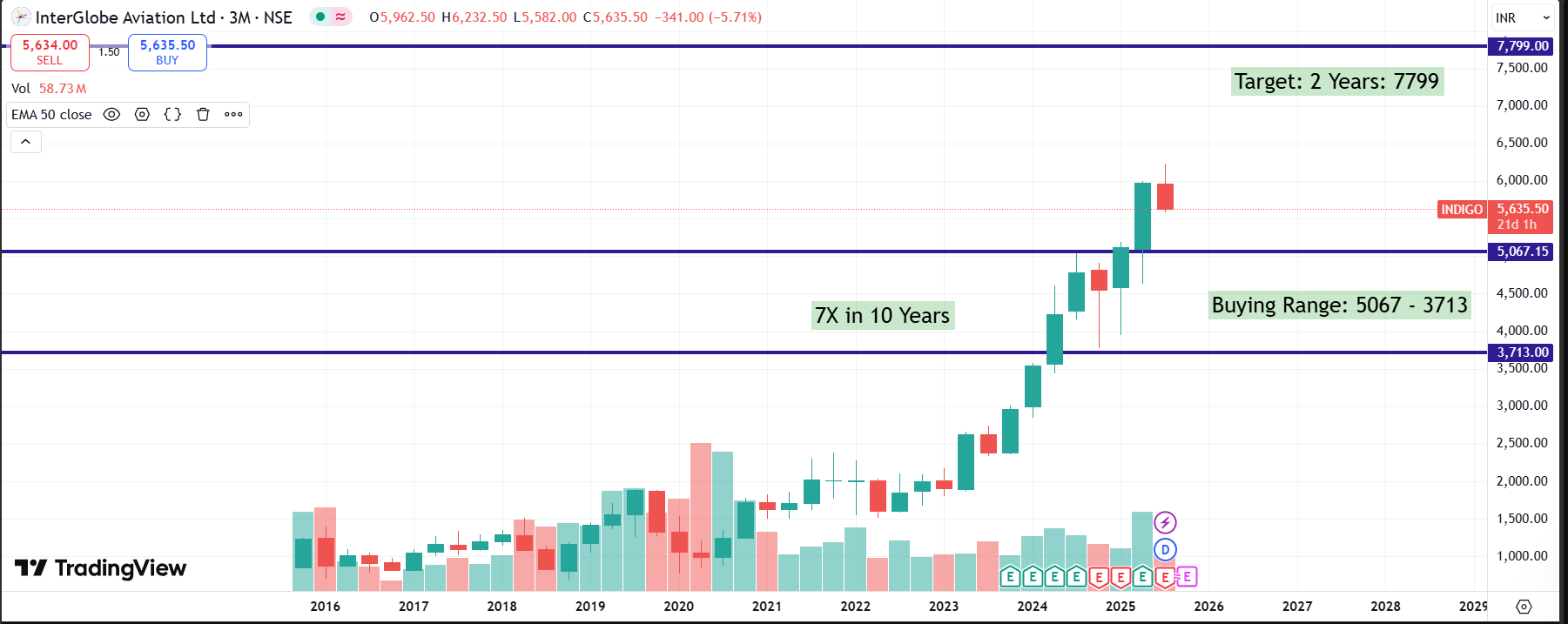

🏛 Historical Journey – Sales & Profit

🔎 Takeaway:

COVID years (FY21–22) = heavy losses.

Bounce back in FY24–25 with strong profits.

FY26 expected to be steady growth with ~11% profit margin.

🔍 Latest Q1 FY26 (Apr–Jun 2025) Snapshot

✈️ Passengers: 31 million (+12% YoY)

💰 Revenue: ₹2.05 lakh Cr (+5% YoY)

🏦 Net Profit: ₹2,176 Cr (↓20% YoY due to higher costs)

🎯 Margins: 10.6% (still healthy for aviation)

📌 Costs: Fuel down -9% YoY, but employee & airport fees up sharply

🌍 How IndiGo Compares

Domestic: IndiGo has ~60% share vs Air India (25%), Vistara & Akasa (small players).

Global: Among world’s top 10 airlines by passengers carried.

Peers: Ryanair (Europe) and Southwest (US) have similar low-cost strategies.

🔮 Growth Outlook

FY26E: Sales ~₹91,300 Cr; Profit ~₹10,000 Cr; EPS ~260.

FY30 Target: Sales ~₹1,77,000 Cr; Profit ~₹12,400 Cr; EPS ~321.

FY35 Target: Sales ~₹3,56,000 Cr; Profit ~₹24,900 Cr; EPS ~645.

💡 What this means: IndiGo has potential to double in 10 years if it maintains leadership.

⚖️ Risks vs Rewards

Risks:

High dependency on fuel prices & INR vs USD.

Debt-heavy due to leasing model.

Rising competition in international routes.

Rewards:

Strong brand trust in India.

Youngest and largest fleet in India.

Massive Airbus order book (1,000+ planes on order).

Growing demand from Tier-2 & Tier-3 cities.

📌 Conclusion for Long-Term Investors

IndiGo is a clear leader in Indian aviation. It has weathered crises, built the biggest network, and remains highly efficient.

Short term: Expect margin pressures from costs.

Long term: Structural story intact → steady compounding.

Best strategy: Accumulate on market corrections.

📢 Disclosure

This is for educational purposes only. Not investment advice. Do your own research before investing.