Godrej Properties Ltd (GPL) – Riding India’s Real Estate Growth Wave

📌 Company Overview

Godrej Properties Ltd (GPL), part of the 128-year-old Godrej Group, is among India’s leading listed real estate developers. The company focuses on residential, commercial, and township projects across major metros, leveraging the Godrej brand’s trust, design excellence, and sustainability commitments.

In recent years, GPL has emerged as India’s #1 developer by residential sales value (FY2024 & FY2025).

🏗 Industry & Growth Prospects

Indian Real Estate Outlook: Residential real estate in India has been robust for four years, supported by rising urbanization, affordability, and government infrastructure initiatives.

CAGR Potential: Industry estimates suggest a 15–18% CAGR growth in residential demand till FY2030, with affordable and premium housing driving momentum.

Sustainability Edge: GPL is a founding member of the Sustainable Housing Leadership Consortium and ranks #1 globally in GRESB (Global Real Estate Sustainability Benchmark) among listed residential developers.

📊 Historical Performance

Sales, Profit & Booking Value

Key Takeaway: From FY21 losses, GPL has staged a strong turnaround with 7x profit growth between FY22–FY26.

💹 Valuations & Market Behavior

Price Multiples History

P/E Band (last 10 years): 18x – 190x (extreme volatility in FY21–22 due to pandemic impact).

PBV Band: 1.7x – 16.9x.

Current (Tr. FY26): P/E 38–50, PBV 3.3–4.4 – slightly above historical averages.

Long-Term Growth Metrics

🔎 Q1 FY26 Highlights

Booking Value: ₹7,082 Cr (down 18% YoY, but 77% 2-yr CAGR).

Net Profit: ₹600 Cr (+15% YoY, highest-ever quarterly).

Sales: ₹1,620 Cr (-5% YoY).

Margin: 36.9% (vs 30.5% YoY).

Key Projects: Godrej MSR City (Bengaluru, ₹2,426 Cr), Godrej Majesty (Greater Noida, ₹925 Cr), Godrej Tiara (Bengaluru, ₹470 Cr).

Geography: Bengaluru contributed >₹3,000 Cr; MMR & NCR >₹1,600 Cr each.

🌍 Segment & Regional Growth

Real Estate: Core business with 94% share in Q1FY26, but down 43% YoY due to base effect.

Hospitality: Small but growing – up 22% YoY.

Geography: Bengaluru remains the growth driver, followed by NCR & MMR.

🏢 Strategic Outlook

Pipeline: 5 new projects added in Q1FY26 worth ~₹11,400 Cr.

Business Development: Achieved 57% of FY26 guidance in Q1 itself.

Collections: ₹3,670 Cr in Q1FY26, +22% YoY.

Net Zero Commitment: Approved by SBTi (Science Based Targets initiative).

📈 Estimates & Fair Value Projections

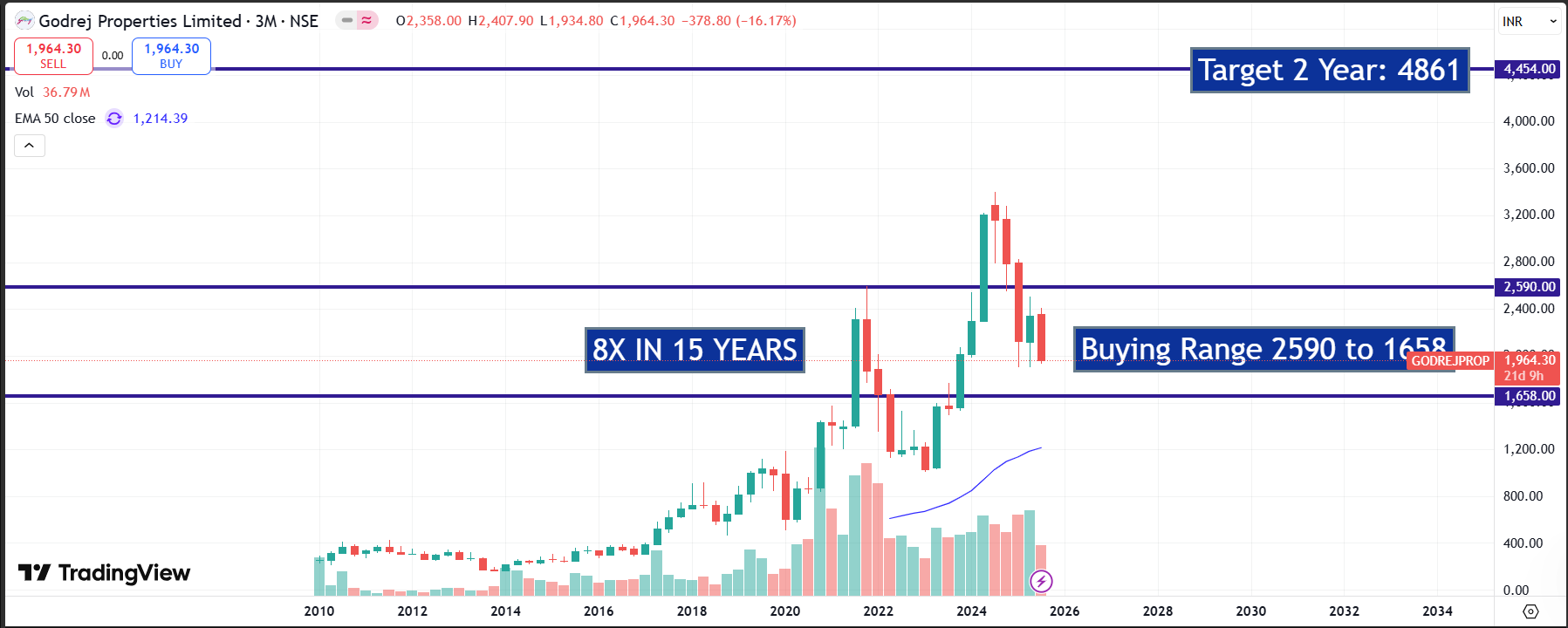

👉 Current Price: ~₹1,969 | Near fair value for FY26, but long-term compounding opportunity till FY2035 remains strong.

⚖ Peer & Global Comparison

Peers (India): DLF, Prestige Estates, Oberoi Realty.

GPL leads in brand trust, sustainability, and consistent booking value.

Global Developers: Compared to China’s Evergrande (debt crisis) and US REITs, GPL’s asset-light, JV-driven model looks more resilient.

📌 Risks & Rewards

Key Risks:

Cyclical demand in real estate.

Regulatory delays (RERA approvals, land acquisition).

Valuations currently above long-term average.

Key Rewards:

Strong balance sheet & collections.

Godrej brand equity with nationwide presence.

Consistent booking pipeline and sustainability leadership.

🧭 Portfolio Weightage Suggestion

At CMP ₹1,969, allocation of ~0.5–1% in long-term portfolios may be considered, with a buy-on-dips strategy.

✅ Conclusion

Godrej Properties has transformed from a cyclical player into a steady compounder, with industry-leading booking growth, strong financials, and brand-backed execution. Long-term prospects till FY2035 remain robust.

📢 Disclosure: This blog is for educational purposes only and not investment advice.