Specialty Retail 2026: The $1.6 Trillion Opportunity Decoding India’s Next Multi-Bagger Sector

1. The Macro Thesis: Why Now?

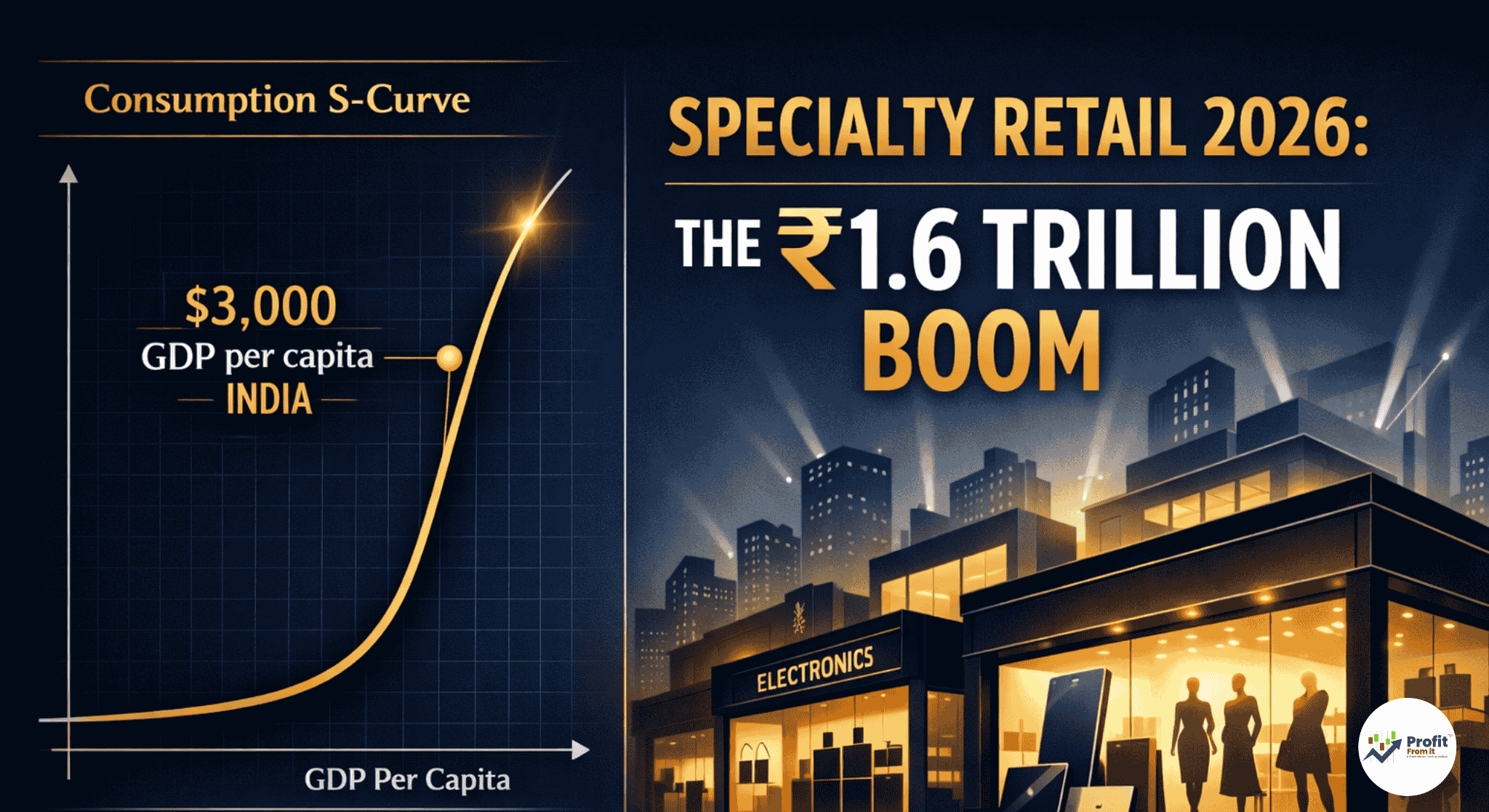

As an investor, the most powerful trend you can follow is the S-Curve of Consumption. Historically, when a nation's GDP per capita crosses the $3,000 threshold, discretionary spending doesn't just grow; it explodes. India is at that exact inflection point today.

Global Benchmarking (CY 2024-2026)

"The incremental rupee in the Indian household is flowing into branded apparel, electronics, and specialized lifestyle categories."

2. Market Size: The "Hockey-Stick" Growth

India's retail market is shifting from a fragmented "Kirana" model to a structured "Organized" model.

Total Market (2024): ₹83 Lakh Cr → (2029P): ₹129 Lakh Cr (+55%)

Organized Share: 21% → 33% (A massive 1,200 bps market share grab)

Non-Discretionary (Essentials): Shrinking from 46% to 43% share.

Category-Wise Opportunity (2024 vs 2029P)

3. Top Listed Players: Market Cap & Weightage

We track the "Industry 95%"—the top players that command the lion's share of the listed specialty retail universe.

4. The Financial "Truth Test"

In our workshops, we focus on the Quality of Earnings. A company must not only grow but also generate cash and maintain solvency.

Profitability Metrics (FY 2024-25)

Solvency & Liquidity

Best ICR (Interest Coverage): Trent (16x) and Manyavar (15x) – Virtually debt-free stress levels.

Best D/E: ABFRL (0.21) and Manyavar (0.27).

Watchlist: ABLBL (2.66 D/E) – High leverage post-demerger needs monitoring.

Cash Flow Analysis (CFO vs CapEx)

5. Growth Velocity: Historical & Trailing Performance

The real "Multi-baggers" are those that compound sales and profits over years.

6. The "Zudio Blueprint" & Future Growth

Trent's store growth is the gold standard of Indian retail. Zudio went from 1 store in 2017 to 854 stores in 2026.

Trent Historical Store Count (Chronological):

FY 2005: 19 stores

FY 2017: 146 stores (Zudio Launch)

FY 2021: 363 stores

FY 2025: 1,091 stores

FY 2026 (9M): 1,164 stores

7. Conclusion: Who Wins the Future of India?

After analyzing the whole industry, we have identified three distinct investment profiles:

The "Safety" Compounder - Trent Ltd: * Why: Positive Free Cash Flow, high ROE (30%+), and self-funding growth. It is the only large-cap growing like a mid-cap.

The "High-Octane" Disruptor - V2 Retail: * Why: Mirroring Zudio's early growth. 64% sales growth in the current "Trial Year" (FY26) suggests it is capturing the massive Tier 2/3 value fashion vacuum.

The "Asset-Light" Niche - Manyavar: * Why: 46% EBITDA margins. It is a "Marriage Proxy" for India. High cash conversion and low CapEx make it a perfect defensive growth play.

Final Verdict: The shift from unorganized to organized retail is a one-way street. Investors should focus on companies with High Asset Turnover and Positive Operating Cash Flows.

Speciality Retail Industry:

Disclaimer: This analysis is for educational purposes only. Please consult with a financial advisor before making any investment decisions.

Trent Limited Q3 FY26 Analysis: Aggressive Expansion vs. Bottom-line Normalization

The Snapshot

The 'Wow' Factor

Store Velocity: Opened 65 stores in a single quarter (17 Westside, 48 Zudio), bringing the total fashion store count to 1,132.

Zudio Dominance: Zudio now represents nearly 75% of the total store portfolio, emphasizing the shift toward value-fashion dominance.

Star Business Transformation: Own-brand contribution in the Star business (grocery) has surged to over 74%, significantly higher than industry averages.

Operational KPI Table (Retail Sector)

Financial Deep Dive (Consolidated)

Cost vs. Efficiency:

While standalone revenues grew by 17%, the consolidated PAT growth of 7% indicates some pressure from the Star business and accounting for new labor code impacts. However, the efficiency in the fashion segment remains top-tier. The operating EBITDA margin expansion to nearly 15.6% (Consolidated) reflects the high operating leverage of the Zudio model. We observe that:

Operating Leverage = EBIT/Sales = approx 1.33

This suggests that for every 1% increase in sales, EBIT is growing by 1.33%, showcasing superior cost management despite rapid store rollouts.

The Forward Curve

Based on management's intent to accelerate the "Star" store expansion and the continued momentum in the UAE (now at 4 Zudio stores), we project:

Q4 FY26: Revenue growth likely to sustain at 14-16% as newly opened stores reach maturity.

Q1 FY27: Expecting margin stabilization around 14% as the "Star" business reaches a critical mass and own-brand contribution peaks.

Valuation Guardrails

Current PE (TTM): ~75.4x

5-Year Median PE: ~98.2x

Verdict: Fairly Valued. While the stock is "historically discounted" relative to its own 5-year peak multiples, it continues to trade at a significant premium to the retail sector average (~32x). The premium is justified by the 18% YoY revenue growth in a sluggish consumption environment.

Shareholding & Pledge Insights

Promoter Holding: Stable at 37.01%.

FII/DII Activity: FIIs marginally decreased stake (from 16.8% to 15.6%), while Domestic Mutual Funds increased stake (from 13.5% to 14.2%), showing strong local institutional confidence.

Pledge: Nil. No promoter shares are pledged.

The Advisory Note

Strategic Outlook (Long-term):

Trent remains the "Gold Standard" of Indian retail. The ability to scale Zudio without diluting margins is a rare feat. The long-term thesis is built on the "Direct-to-Customer" playbook where Trent controls everything from design to distribution.

Tactical Outlook (Short-term):

At ₹3,561, the stock has corrected from its 52-week highs (~₹6,261), offering a "Margin of Safety" for long-term investors. However, the slow expansion of the Star business remains a minor drag on consolidated sentiment.

Fairvalue:

Mandatory Disclosure:

This report is for informational purposes only. Investment in securities involves risks.

Manyavar (Vedant Fashions) Q3 FY26 Analysis: Robust Margin Retention vs. Moderating Same-Store Growth

The Snapshot

Note: CMP updated as of March 10, 2026. Per official filings, the company has no subsidiaries; results are presented as a single entity.

The 'Wow' Factor

Industry-Leading EBITDA Margins: Despite revenue contraction, the company sustained an EBITDA margin of 44.4%, showcasing extreme operational resilience.

Twamev Momentum: The premium brand Twamev continues to outperform, reporting 40% growth in the 9M period, signaling that high-end wedding wear is more resilient than mid-market.

Cash Conversion: Maintained a healthy 95% cash conversion ratio (Operating Cash Flow to PAT), ensuring the business remains self-funded.

Global Footprint: Expanded to 664 EBOs across 253 cities globally, including 16 international stores.

Operational KPI Table

Financial Performance (Reported)

The Q3 performance was significantly impacted by a "wedding date disruption"—fewer auspicious dates in December and none in January—coupled with muted middle-class sentiment.

Key Financial Notes:

GST Impact: Gross margins were pressured (65.7% vs 67.3% last year) primarily due to the GST hike from 12% to 18% on roughly 90% of the product portfolio.

Labour Code Provision: A one-time incremental impact of ₹1.62 Cr was recognized under employee benefits due to new government labour code notifications.

Peer Benchmarking & Market Position

Manyavar remains the largest organized player in the Indian wedding wear market. While competitors like Tasva (ABFRL) and Ethnix (Raymond) are expanding, Manyavar's "Full Price" strategy (no discounting) keeps its brand equity and margins significantly higher than the industry average.

Management Tone & Strategy

Tone: Prudent & Strategic.

Management is focusing on "quality over quantity" for the next few quarters. They are strategically consolidating the retail footprint by closing underperforming smaller stores and focusing on larger flagship formats that can house multiple brands (Manyavar + Mohey + Twamev).

Key Risks:

SSSG Pressure: Negative quarterly SSSG indicates that store-level footfall is struggling.

Consumption Headwinds: The "middle-class" consumer segment is showing signs of fatigue, though the "premium" segment remains strong.

Valuation Guardrails

Current PE: ~16.8x (at ₹356)

5-Year Median PE: ~72x

Verdict: Deep Value. The stock is trading at a massive discount to its historical valuation. While the Q3 profit contraction is a headwind, the industry-leading margins (44%+) and asset-light model make it a compelling long-term play at these price levels.

The Advisory Note

Strategic Outlook: The long-term thesis is driven by the formalization of the ₹1,00,000 Cr+ wedding market. Manyavar’s ability to maintain margins despite a revenue dip suggests a very strong brand moat.

Tactical Outlook: At ₹356, the market is pricing in a prolonged slowdown. For investors with a 2-3 year horizon, this represents a significant margin of safety given the company's historical ability to bounce back during heavy wedding seasons.

FAIRVALUE :

Mandatory Disclosure: This report is for educational purposes only. We are SEBI-registered advisors.