Pidilite Industries Limited's Q3 FY25:

📈 Insights and Highlights

Revenue and Volume Growth:

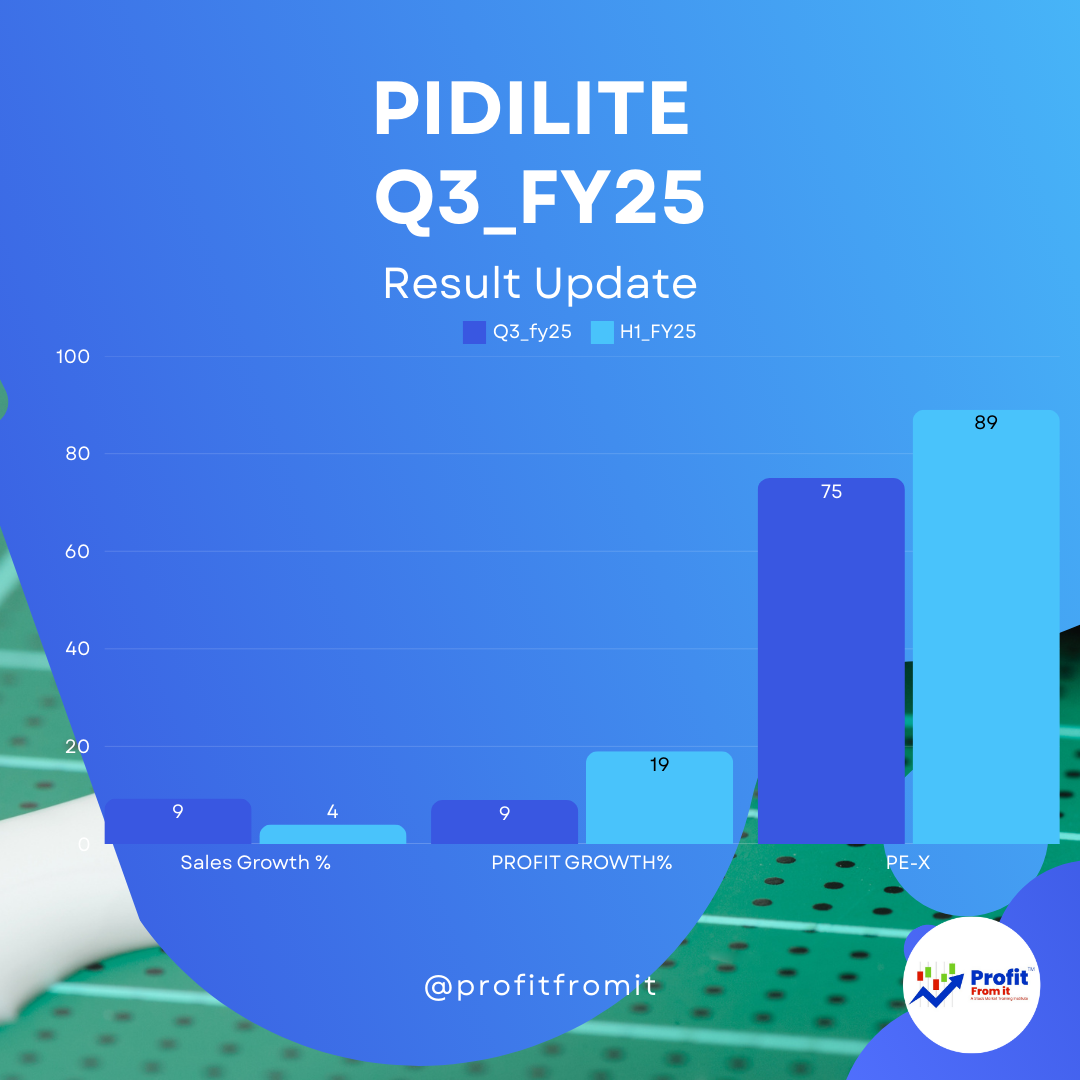

Revenue growth 📊: 9.3% increase with Underlying Volume Growth (UVG) of 9.7% across categories and regions.

Consumer and Bazaar (C&B) 🏠: UVG at 7.3%

Business to Business (B2B) 🏢: Strong momentum with UVG at 21.7%.

Profitability:

Gross margins ➕: Improved by 100 basis points year-over-year due to benign input prices.

EBITDA Margins 📉: 24.3% (a slight drop from 25.1% in Q3 FY24) due to increased A&SP spends.

Segmental and Regional Growth:

Domestic 🇮🇳: Double-digit revenue growth with better EBITDA margins.

International 🌍: Modest sales growth amidst global economic uncertainties.

💰 Financial Performance Q3 FY25 vs. Q3 FY24:

Profit Margins:

Profit Before Tax (PBT) 💵: ₹752 crore, up by 9%.

Profit After Tax (PAT) 💸: ₹557 crore, also up by 9%.

📊 Industry Key Performance Indicators (KPIs):

Valuation Ratios:

Consistent profitability supports an attractive valuation outlook. Trail EPS comes to 38.4 giving the Trail PE of 75 while F_Eps comes to 45 giving the F_PE of 64.

🔮 Long-Term Outlook:

Future Prospects:

🌧️ Anticipating improved demand post-good monsoon and more construction activities.

🎯 Strategic investments in brands, supply chain, and personnel indicate a focus on sustained, volume-led growth.

This analysis encapsulates the recent financial performance and forward-looking statements indicating Pidilite Industries' strong market positioning and strategic initiatives aimed at long-term value creation.