🚢 Mazagon Dock Shipbuilders: Q3FY25 & 9MFY25 Analysis

🔍 1. Key Insights & Highlights:

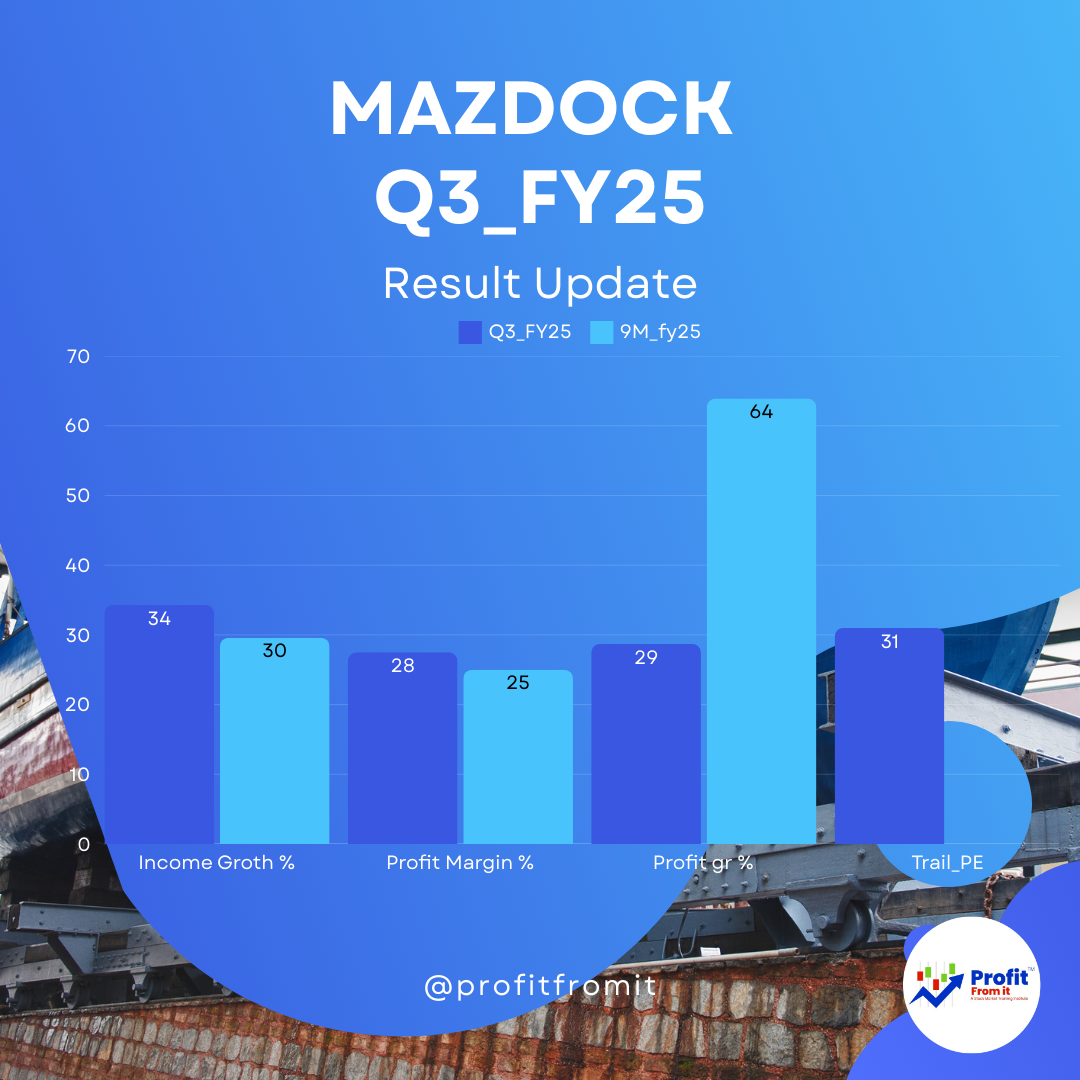

📈 Record Revenue: ₹3,144 crore in Q3FY25 🆙 34.3% YoY (₹2,362 crore in Q3FY24).

💥 Profit Surge: Consolidated PAT hit ₹807 crore 💹 +28.7% YoY (₹627 crore in Q3FY24).

🇮🇳 Historic Event: Tri-commissioning of 🇮🇳 INS Surat, INS Nilgiri & INS Vaghsheer on 🗓️ Jan 15, 2025.

🏆 Navratna Status: Awarded by the Department of Public Enterprises – boosting operational flexibility.

💸 Zero Debt: Maintains a debt-free balance sheet, showcasing financial prudence.

📑 2. Order Book Analysis (as of Dec 31, 2024):

📦 Total Order Book: ₹34,787 crore 🏗️.

🔹 Key Projects:

⚓ P15B Destroyers: ₹4,301 crore delivered; ₹26,803 crore pending.

🛳️ P17A Frigates: ₹14,518 crore still in the pipeline.

🐋 P75 Submarines: ₹2,838 crore left to execute.

🌊 ONGC Offshore Vessels: ₹5,955 crore in progress.

📊 3. Consolidated Revenue Growth:

📢 Key Driver: Timely delivery & execution of high-value defense projects. 🚀

💹 4. Profit Margins Comparison:

📈 Margin Boost: Cost efficiencies & higher revenue realization from strategic defense projects.

🏦 5. Consolidated Profit Growth:

💡 Key Insight: Profits fueled by higher execution and operational excellence.

⚖️ 6. Financial Ratios (at CMP ₹2,082):

📊 Profitability:

🔹 ROCE: ~28%

🔹 ROE: ~26%

💪 Solvency:

⚖️ Debt/Equity: 0.00 (Debt-Free)

💧 Liquidity:

💲 Current Ratio: 2.5x (Strong liquidity position)

📉 Valuation:

🧮 EPS (TTM): ₹65.77

📊 P/E: ~32x (Valuation reflects growth prospects)

🛠️ 7. Outlook & Budget Impact:

🟢 Near-Term:

Continued growth expected from ongoing defense projects.

Enhanced production from the new facilities, like the Nhava Yard Concrete Batching Plant.

🔵 Long-Term:

Government's 'Make-in-India' push & defense modernization plans provide strong tailwinds.

🛳️ International defense orders are likely to rise post Modi-Trump defense discussions.

🏛️ Union Budget 2025 Impact:

🚀 Higher defense allocations support long-term growth.

📡 Naval modernization will continue to favor Mazagon Dock.

🎯 Conclusion:

📌 Mazagon Dock stands strong with:

🚢 Robust Order Book: ₹34,787 crore.

📈 Record Revenue & Profit: All-time high quarterly performance.

💪 Debt-Free & Efficient: Margins & returns improving consistently.

🏆 Future Outlook:

Short-Term: Order execution, new vessel deliveries.

Long-Term: Growth aligned with India's defense & manufacturing ambitions.

📊 Investment Consideration: At CMP ₹2,082, valuations are reasonable considering growth potential & zero-debt status.

⚓ Anchoring India's Naval Supremacy! 🇮🇳 💥🚀🛳️

Conclusion:

Mazagon Dock Shipbuilders continues to exhibit strong financial and operational performance with an expanding order book, improved profitability, and strategic growth initiatives aligned with India's defense ambitions. The stock’s current valuation appears reasonable given its growth trajectory and zero-debt status.

📢 Disclaimer & Disclosure Statement

Important Investor Advisory Notice

This research analysis is for informational purposes only and should not be considered as financial, investment, or legal advice. The information provided herein is based on publicly available financial reports, market data, and our analysis. Investors are advised to exercise caution and discretion before making any investment decisions.

Class Sessions

1- IREDA’s latest quarterly results

2- Patanjali's Q2 FY25 financials

3- United Breweries Limited - Detailed Q2 FY25 Consolidated Financial Analysis

4- HDFC LIFE Q1 FY 2025

5- DMart Q1 FY 2025

6- HDFC LIFE Q1 FY 2025

7- Bajaj Auto Q1 FY24 Analysis

8- IREDA Q1 FY 2024

9- TCS Q1 FY 2025

10- HDFC Asset Management Company (HDFC AMC) Q1 FY25 Analysis

11- BAJAJ FINANCE | BEL | VOLTAS | LT | MARUTI SUZUKI Q3 Result Update 2024

12- How do you Analyse NBFC companies?

13- Which company is best for home appliances?

14- Who is No 1 construction company in India?

15- Aerospace & Defense Industry

16- Passenger Vehicle Market Share

17- Which is the No 1 small finance bank in India?

18- What is the position of steel market in India?

19- Tyres & Rubber Products INDUSTRY

20- Computers-Software & Consulting_q3_fy24

21- Which is the best stock in Consumer Food? Watch Now

22- Auto Sector Vehicle January Data

23- Telecom Industry in India: Sector Overview

24- Comparision: Reliance Retail | Dmart | ShoppersStop | Spencer | Vmart

25- ICICI GI, Supreme Industry, Asian Paint & Ultratech Cement | Q3 FY2024 Result Update

26- TCS, Dmart, HDFC AMC & HDFC LIFE Q3 FY2024 Result Update

27- LTTS, MAPMYINDIA, HDFC BANK Q3 FY2024 Result Update

28- Hospital Industry Analysis

29- Industry Update

30- Tata Consultancy Services Ltd Q4 Result Update 2023

31- Ultratech Cement Latest News | Q4 Result 2023

32- Q4 Result 2023

33- Q3 Result Update 2023

34- Student Page Video

35- Live Query Sessions Video Updated

36- TCS's Q3 FY25: (Leading Company from Computers - Software & Consulting Industry)

37- TATAELXSI's Q3 FY25:

38- IREDA's Q3 FY25:

39- Avenue Supermarts Limited's (DMart) financial results for the third quarter ended December 31, 2024:

40- HDFC Asset Management Company's financial results for Q3 FY25:

41- HDFC Life Q3 FY25 Analysis 📊

42- L&T Technology Services Q3 FY25

43- Havells Q3 FY25 Analysis 📊

44- Reliance Industries' Financial Results for Q3 FY25 📊

45- ICICI Lombard's performance for Q3 FY25”

46- Q3 FY25 Supreme Industries Ltd. 📊

47- Indian Railway Finance Corporation Limited (IRFC) for Q3 FY25:

48- Zomato's Q3 FY25 financial results:

49- Dixon Technologies (India) Ltd. Q3 FY25 Results 📊

50- HDFC BANK Q3 FY25 Results 📊

51- Hindustan Unilever Q3 FY25 Results 📊

52- Pidilite Industries Limited's Q3 FY25:

53- UltraTech Cement Limited for the third quarter (Q3) and the first nine months (9MFY) of the financial year 2025:

54- Indian Energy Exchange (IEX) Q3 FY25:

55- AU Small Finance Bank Limited's Q3 FY25:

56- Indigo Airlines' performance for Q3 FY25: Overview: 🚀

57- Balkrishna Industries Q3 FY25 Performance Analysis 📊

58- CDSL's financial results for Q3 FY25: Key Insights and Highlights

59- EMS Limited's financial results for Q3 FY25:

60- JSW Steel's Q3 FY25 financial performance:

61- Wonderla Holidays Limited Q3 FY25 Analysis 📊

62- Bajaj Housing Finance's latest results for Q3 FY25;

63- Route Mobile's latest financial results for Q3 FY25:

64- Bajaj Auto Q3 FY25 Consolidated Financial Analysis:

65- Maruti Suzuki India Limited (MSIL) - Q3 FY25 Financial Highlights and Analysis 📊

66- Q3 FY25 results for C.E. Info Systems Limited (MapMyIndia)

67- Bajaj Finance's Q3 FY25: 📊

68- Voltas' Q3 FY25 financial results:

69- 📢 BEL Q3 FY25 Results – Key Insights & Analysis 🚀

70- 📊 Waaree Energies Q3 FY25 and 9M FY25 Performance Analysis 🚀

71- 📊 Dr Lal PathLabs - Q3 FY25 & 9M FY25 Financial Analysis & Insights 🚀

72- Larsen & Toubro Q3 FY 25: 🚀📊📈

73- 📊 Analysis of Tata Consumer Products Q3 FY25 & 9M FY25 Results 📈

74- 📊 Manyavar (Vedant Fashions Ltd.) Q3 FY25 Earnings

75- Nestlé India Q3 FY25 results:

76- 📢 Divis Laboratories Q3 FY25 & 9M FY25 Results - 📊💡

77- 🎨 Asian Paints Q3 FY25 & 9M FY25 Financial Analysis & Insights 📊

78- 📊 Godrej Properties Q3 FY25 Analysis 🏗️

79- 📊 Kajaria Ceramics Q3 FY25 Analysis 📊

80- 📊 Titan Q3 FY25 & 9M FY25 Performance Analysis 🔥🚀

81- 🚀 InfoEdge Q3FY25 Results Analysis & Insights 📊

82- 📊 Page Industries Q3 FY25 Analysis & Investment Insights 🏭📈

83- 📢 SBI Q3FY25 Earnings Analysis & Insights 📊🏦

84- 📊 PI Industries Q3 FY25 Results - Analysis & Insights 🔍

85- 🚀 Amara Raja Batteries (ARE&M) Q3 FY25 Results Analysis and Insights 📊

86- 📊 Affle (India) Limited Q3 & 9M FY2025 Earnings Analysis & Insights 🚀

87- 📊 Patanjali Foods Limited Q3 FY25 Financial Analysis & Key Insights 🚀

88- 📊 Apollo Hospitals Q3FY25 & 9MFY25 Financial and Operational Analysis

89- 🚄 IRCTC Q3FY25 Earnings Analysis & Insights 📊💡

90- 🎯 Jubilant FoodWorks Q3FY25 & 9MFY25 Key Highlights 🚀🔥

91- 📊 UBL Q3 FY25 & 9M FY25 Performance Analysis – Investor Insights 💹

92- 🚢 Mazagon Dock Shipbuilders: Q3FY25 & 9MFY25 Analysis

93- 📈 TCS FY25 Results: Muted CC Growth, Hence Low Sales & Profit Growth in Headwind Environment, but valuations near to favourable.

94- 🔋 IREDA Q4FY25 Results: Powered by Growth, Poised for the Future

95- 📊 ICICI Lombard General Insurance – FY25 & Q4 FY25 Results Update

96- 🔍 HDFC AMC Q4FY25 & FY25 Results: Strong Performance, Robust Growth & Healthy Margins

97- 📈 HDFC Life FY25 Results: Strong Growth, Steady Profits & Enhanced Market Position

98- 📊 Tata Elxsi Q4FY25 & FY25 Review: Growth Foundations Amidst Headwinds

99- 🔍 HDFC Bank – FY25 & Q4FY25 Results Highlights

100- 📊 Havells FY25 Results Analysis: Robust Growth with Strategic Resilience

101- Waaree Energies Ltd. (WAAREEENER) FY25 Results Update & Investor Insights

102- 📊 AU Small Finance Bank Q4 & FY25 Results – Growth Anchored by Profitability & Prudent Risk Management

103- Bajaj Housing Finance Ltd. – FY25 Financial Performance Highlights and Analysis

104- Tata Consumer FY25 & Q4FY25 Summary: Strong Growth with Margin Recovery on the Horizon

105- L&T Technology Services (LTTS) Q4 FY25 & FY25 Results Analysis

106- Hindustan Unilever Limited (HUL) FY25 & Q4FY25 Results Update

107- 📊 Nestlé India Limited – FY25 & Q4FY25 Results Analysis

108- 📊 IEX FY25 and Q4FY25 Results Analysis

109- Supreme Industries Limited – FY25 Financial Results Update

110- Maruti Suzuki FY25 Results Update: Key Insights and Strategic Highlights

111- Reliance Industries Limited – FY25 Results Update

112- UltraTech Cement FY25 Results Update: Driving Consolidated Growth Amidst Strategic Expansions

113- Bajaj Finance Limited – Q4FY25 and FY25 Financial Results Update

114- 📊 Eternal Limited – Q4FY25 & FY25 Financial and Strategic Performance Update

115- 🏢 Godrej Properties Q4 & FY25 Result Analysis: Booking Boom & Financial Resilience

116- 🧾 DMart Q4 FY25 & FY25 Result Highlights – Resilient Growth Amid Operational Pressures

117- 📊 CDSL Q4 & FY25 Result Analysis

118- 📊 Kajaria Ceramics Q4 FY25 Results Analysis 📈

119- Manyavar (Vedant Fashions Limited) Q4 FY25 Financial Analysis

120- Wonderla Holidays Q4FY25 & FY25 Financial Analysis: Strong Footfalls Despite Market Headwinds

121- 📊 Voltas Q4 FY25 Financial Analysis: Detailed Investor Insights

122- 📊 Route Mobile Q4 FY25 & FY25 Financial Analysis

123- United Breweries Limited (UBL) Q4 FY25 Financial Analysis

124- Asian Paints Q4 FY25 Financial Analysis: Detailed Investor Insights

125- Pidilite Industries Q4 FY25 Financial Analysis

126- Larsen & Toubro (L&T) Q4 FY25 & FY25 Financial Analysis

127- 📊 Titan Company Ltd. Q4 FY25 & FY25 Financial Performance Analysis

128- Affle 3I Q4 & FY25 Results: Strong Growth

129- Divi's Laboratories Q4 & FY25 Results: ₹2,209 Cr Profit, ₹30 Dividend, CMP ₹6,539 | Long-Term Outlook & Valuation

130- ITC Hotels Q4 & FY25 Results: 73% Profit Growth | ₹202 CMP Valuation & Expansion Outlook

131- Patanjali Foods Q4 FY25 Results: 70% PAT Growth | Highest Ever Revenue Achieved

132- Jubilant FoodWorks Q4 & FY25 Results: Delivery Growth, Store Expansion & Financial Insights

133- 🚗 MapmyIndia Q4 FY25 & FY25 Results: Strong Momentum in Tech & Mobility

134- 🧾 Page Industries Q4 & FY25 Result Update Brand:

135- 🇮🇳 Bharat Electronics Ltd – Q4 & FY25 Financial Results & Investor Insights 🔍

136- 🔬 PI Industries Ltd – Q4 & FY25 Results Review | Growth, Margins, and Outlook

137- 📊 Dixon Technologies (India) Ltd – Q4 FY25 & FY25 Financial Results Analysis

138- 🧬 Dr. Lal PathLabs Q4 & FY25 Results: Strategic Growth Beyond Metro Markets

139- 🛫 IndiGo Q4 FY25 Results: Record Profits, Rising Passengers & Strong Outlook

140- 🚜 Balkrishna Industries Ltd – Q4 & FY25 Results Update: Strong Long-Term Strategy Despite Soft Q4

141- Info Edge (India) Ltd. Q4 FY25 & FY25 Results Analysis: Detailed Investor Insights

142- 📊 Bajaj Auto Q4 FY25 & FY25 Financial Highlights: Growth, Resilience, & Green Momentum

143- IRCTC Q4 & FY25 Results: Insights for Investors

144- 🚢 Mazagon Dock Q4 & FY25 Results:

145- 🏥 Apollo Hospitals FY25 Results: Strong Performance Backed by Expansion Plans

146- 📊 TCS Q1 FY26 Financial Performance: Comprehensive Investor Guide

147- United Breweries Ltd (UBL) Q4 & FY25 Results Analysis: Brewing Growth with Consistency

148- Q1 FY26 Financial Analysis of IREDA

149- Tata Elxsi Q1 FY26 Financial Results: Comprehensive Analysis

150- 🏪 DMart Q1 FY26 Financial Results: Stable Growth Amid Margin Pressure

151- HDFC Life Q1 FY26 Results: Strong Momentum Continues in Life Insurance

152- ICICI Lombard General Insurance Q1 FY26 Results Analysis: Stable Growth Amid Regulatory Changes

153- ITC Hotels Q1 FY26 Results: Record Performance, Robust Growth, and Long-Term Outlook

154- L&T Technology Services Ltd (LTTS) Q1 FY26 Results: Investor Analysis

155- HDFC AMC Q1 FY26 Results Analysis: Strong Performance & Strategic Positioning

156- Reliance Q1 FY26 Results: Record-Breaking Profits & Multi-Engine Growth 🚀

157- HDFC Bank Q1 FY26 Results: Growth Resilient, Bonus Announced! 🚀🏦

158- 🚦 AU Small Finance Bank (AUBank) Q1 FY26 Results Analysis: Strengths & Concerns at CMP ₹795

159- 📊 Havells India Q1 FY26 Results Analysis at CMP ₹1532

160- 🏗️ UltraTech Cement Q1 FY26 Results: Strong Growth, Margin Recovery & Capacity Expansion 🚀

161- Eternal Limited (Zomato) Q1 FY26 Results: Revenue Surges 70%, Quick Commerce Leads Growth

162- 🏭 Kajaria Ceramics Q1 FY26 Results: Margins Improve Amidst Soft Demand 📊

163- 🚆 IRFC Q1 FY26 Results: Strongest-Ever Quarterly Performance! 📈

164- ⚡ IEX in Flux: Q1 FY26 Results Amid Market Coupling Shock

165- 📊 Dixon Technologies Q1 FY26: Strong Growth Amid Strategic Expansions

166- 🏠 Bajaj Housing Finance – Q1 FY26 Result Highlights

167- 📊 Tata Consumer Products – Q1 FY26 Results: Steady Topline, Margin Challenges

168- 📊 Bajaj Finance Q1 FY26 Results: Solid Growth, AI-led Efficiency, and Asset Quality Focus! 💼

169- 📊 Nestlé India Q1 FY26 Results Analysis

170- 🏭 Supreme Industries Q1 FY26 Results: Volume Up, Profit Down — What’s Next? 📊

171- 📊 CDSL Q1 FY26 Results: Marginal Growth in Revenue, Digital Strategy Intact 🧾🔍

172- 🧾 Balkrishna Industries Q1 FY26 Result Analysis 🛞

173- 📊 Affle Q1 FY26 Financial Performance: Resilient Growth with Focused Execution

174- Bharat Electronics Limited (BEL) Q1 FY26 Results Analysis 📊

175- Waaree Energies Ltd Q1 FY26 Results Analysis

176- Asian Paints Q1 FY26 Results: Analysis with Key Insights & Outlook 🏭🎨

177- 🚧 Larsen & Toubro Q1 FY26 Results – Record Order Book, Global Growth, and Margin Watch Ahead

178- 🚗 Maruti Suzuki Q1 FY26 Results – Steady Profit, Strong Exports, But Margins Under Pressure

179- 👔 Manyavar (Vedant Fashions Ltd) Q1 FY26 Results – Steady Growth Amidst Mixed Market Sentiments

180- ✈️ IndiGo Q1 FY26 Results – Navigating Headwinds, Flying Towards Growth!

181- Intrinsic Valuation & Wealth Building – After Class Review

182- 🎥 Session Replay (YouTube Live): Intrinsic Valuation & Wealth Building: Fair Value, Margin of Safety & Allocation Strategy

183- Godrej Properties Q2 FY2026 Analysis: Scaling New Heights 🏙️📈

184- ✈️ IndiGo Q2 FY26: Currency Turbulence vs. Operational Resilience

185- IREDA Q3FY26 Results: Green Energy Giant Hits Record Profits—Time to Buy?

186- DMart (Avenue Supermarts) Q3 FY26 Results Analysis: Margin Expansion Amidst Steady Growth

187- TCS Q3 FY26 Results Analysis: AI Momentum vs. Statutory Headwinds

188- Tata Elxsi Q3 FY26 Results Analysis: Healthy Margin Expansion Amidst Steady Revenue Growth

189- ICICI Lombard (ICICIGI) Q3FY26 Analysis: Navigating Industry Shifts with Resilience

190- HDFC AMC Q3 FY26 Results Analysis: Steady Growth Amid Industry Tailwinds

191- HDFC Life: Driving Protection Momentum in Q3 FY26

192- LTTS Q3FY26 Analysis: Strategic Pivot Towards "Engineering Intelligence"

193- Reliance Industries Q3 FY26 Financial Analysis & Investment Insights

194- AU Small Finance Bank Q3FY26 Results: A Deep Dive into 26% Profit Growth and Strategic Expansion

195- HDFC Bank Q3FY26 Analysis: Navigating the Glide Path with Disciplined Growth

196- Havells Q3 FY26 Analysis: Robust Revenue Growth Amidst Margin Headwinds

197- IRFC Q3FY26 Results: Record Profits and Strategic Pivot Under "IRFC 2.0"

198- ITC Hotels Q3FY26 Analysis: Record Revenues & Strategic Scalability

199- Supreme Industries Q3 FY26: Resilient Volumes Amid Pricing Headwinds

200- Eternal Limited Q3FY26 Results: Quick Commerce Turns Profitable!

201- Waaree Q3 FY26 Analysis: Record-Breaking Growth Fuels Aggressive 'Waaree 2.0' Expansion

202- IndiGo Q3FY26 Results Analysis: Navigating Turbulence with Resilient Fundamentals

203- UltraTech Cement Q3FY26 Results: A Masterclass in Operational Efficiency

204- What is the policy repo rate as decided by the Monetary Policy Committee in its February 2026 meeting?

205- Asian Paints Q3FY26: Resilience Amidst Competitive Intensity

206- Tata Consumer Q3FY26: Strong Volume Growth and Margin Expansion Steer Performance

207- Bharat Electronics Ltd (BEL): A High-Octane Q3 Performance Analysis

208- BKT Q3FY26 Results: Resilient Volume Rebound Amid Global Headwinds

209- L&T Q3 FY26 Analysis: A ₹7 Lakh Crore Milestone in Engineering Excellence

210- Maruti Suzuki Q3 FY'26 Results: A Deep Dive into "The GST Bounce Back"

211- Dixon Technologies Q3 FY26 Analysis: Transitioning to a Design-Led Component Giant

212- IEX Q3FY26 Results: Powering Through Energy Transitions

213- Voltas Q3 FY26 Results Analysis: Leadership Strengthened Amid Seasonality

214- Bajaj Auto Q3 FY26 Analysis: Record-Breaking Performance as Exports and EVs Scale New Peaks

215- Dr. Lal PathLabs Q3 FY26 Analysis: Steady Revenue Amidst Seasonal Headwinds & One-Off Costs

216- Nestle India Q3FY26 Results: Record Turnover and Five-Year High Volume Growth

217- Kajaria Ceramics Q3 FY26 Analysis: Efficiency Gains Meet Muted Demand

218- Affle 3i Limited Q3 FY2026 Analysis: AI-Driven Milestone Performance

219- CDSL Q3FY26 Analysis: Demat Dominance Continues Amidst Shifting Revenue Mix

220- Bajaj Housing Finance Ltd. (BAJAJHFL) Q3 FY26 Results Analysis

221- Bajaj Finance Q3 FY26 Analysis: Robust AUM Scaling vs. Rising Cost of Funds

222- Pidilite Q3 FY26 Consolidated Analysis: Volume-Led Mastery Amidst Input Cost Tailwinds

223- Wonderla Holidays Ltd. Q3 FY26 Analysis: Record Revenue vs. Margin Pressure from New Launches

224- Godrej Properties Q3 FY26 Analysis: Blockbuster Pre-Sales vs. Operational Revenue Paradox

225- Page Industries Q3 FY26 Analysis: Steady Growth Meets One-Time Regulatory Hurdles

226- Mazagon Dock Shipbuilders Q3 FY26 Analysis: Order Book Execution vs. Margin Normalization

227- State Bank of India Q3 FY26 Analysis: Credit Engine Fires Up vs. Margin Compression Concerns

228- Apollo Hospitals Q3 FY26 Analysis:

229- Titan Company Q3 FY26 Analysis: Dominant Revenue Surge vs. Margin Compression Tailwinds

230- Jubilant FoodWorks Q3 FY26 Analysis: Robust Topline Growth vs. Margin Compression Challenges

231- Amara Raja Energy & Mobility Q3 FY26 Analysis: New Energy Resilience vs. Profitability Headwinds

232- LG Electronics India Q3 FY26 Analysis: Premium Momentum vs. High-Base Moderation

233- Patanjali Foods Q3 FY26 Analysis: Record Revenue Surge vs. Operating Margin Pressure

234- Divi's Laboratories Q3 FY26 Analysis: Custom Synthesis Resilience vs. Margin Pressure from Labor Transitions

235- IRCTC Q3 FY26 Analysis: Robust Ticketing Momentum vs. Tourism Segment Volatility

236- PI Industries Q3 FY26 Analysis: Navigating a Challenging Global Cycle

237- Manyavar (Vedant Fashions) Q3 FY26 Analysis: Robust Margin Retention vs. Moderating Same-Store Growth

238- Info Edge (Naukri) Q3 FY26 Analysis: Recruitment Resilience vs. Non-Recruitment Cash Burn

239- EMS Limited Q3 FY26 Analysis: Order Book Resilience vs. Bottom-line Pressure

240- MapmyIndia (C.E. Info Systems) Q3 FY26: Seasonal Headwinds vs. Record Order Book

241- Q3fy26_Results Update for 55 Focused Companies Spread Sheet

242- Q3 FY26 Earnings Masterclass: The Turning Point for Indian Corporates

243- Trent Limited Q3 FY26 Analysis: Aggressive Expansion vs. Bottom-line Normalization

244- NIIT Learning Systems Q3 FY26 Analysis: Scaling AI-Led L&D vs. Margin Dilution Risks

245- Bharti Airtel Q3 FY26 Analysis: Premiumization Lead vs. High Capex Intensity

246- HAL Q3 FY26 Analysis: Execution Momentum vs. Rising Employee Liabilities

247- Siemens Energy India (ENRIN) Q1 FY26 Analysis: Robust Backlog Execution vs. Elevated Valuations & One-Off Labor Costs

248- ABB India Q4 CY2025 Analysis: Record Order Inflows vs. Margin Headwinds

249- Siemens Limited Q5 FY25 Analysis: Structural Tailwinds vs. Capital Allocation Discipline

250- Polycab Q3 FY26 Analysis: Record Top-line Growth vs. Margin Compression

251- Solar Industries Q3 FY26 Analysis: Record Defense Execution vs. Sluggish Domestic Mining

252- Mahindra & Mahindra Q3 FY26 Analysis: Breakthrough Services vs. Commodity Inflation Headwinds

253- Cummins India Q3 FY26 Analysis: Steady Domestic Growth Meets Export Headwinds

254- Timken India Limited Q3 FY26 Analysis: Revenue Resiliency vs. Transitional Margin Pressure

255- 🚜 Investment Report: Construction Vehicles Industry

256- TCS Q4 FY26 Analysis: The AI Growth Engine vs. Macro Headwinds

257- Action Construction Equipment (ACE) Q3 FY26 Analysis: Margin Mastery vs. Volume Headwinds

258- Netweb Technologies Q3 FY26 Analysis: AI Tsunami vs. Supply Chain Headwinds

259- ICICI Lombard Q4 FY26 Analysis: Growth Momentum vs. Loss Ratio Headwinds

260- HDFC AMC Q4 FY26 Analysis: Market Share Gains vs. Yield Pressure

261- HDFC Life Q4 FY26 Analysis: Robust Premium Growth vs. Regulatory Margin Pressures

262- CRISIL Q1 FY26 Analysis: 46% Profit Surge vs. Dynamic Operating Costs

263- HDFC Bank Q4 FY26 Analysis: Liquidity Rebound vs. Margin Compression Resistance

264- Nestlé India Q4 FY26 Analysis

265- Tata Elxsi Q4 FY26 Analysis: Resilient Revenue Growth vs. The Exceptional Cost Hurdle

266- Havells India Q4 FY26 Analysis: Steady Cable Demand vs. The Summer Letdown

267- IEX Q4 FY26 Analysis: Record Volumes vs. Regulatory Overhang

268- Trent Limited Q4 FY26 Analysis: Aggressive Expansion vs. Consumption Softness

269- Reliance Industries Q4 FY26 Analysis: Telecom & Retail Resilience vs. O2C Margin Headwinds

270- UltraTech Cement Q4 FY26 Analysis: Historic 200 MTPA Milestone vs. Geopolitical Cost Headwinds

271- Bajaj Housing Finance Q4 FY26 Analysis: Record Earnings vs. Margin Pressure

272- AU Small Finance Bank Q4 FY26 Analysis: Universal Ambitions vs. NIM Pressure

273- Supreme Industries Q4 FY26 Analysis: Volume Leadership vs. Margin Expansion

274- Maruti Suzuki Q4 FY26 Analysis: Record Top-line Growth vs. Margin Pressure

275- Eternal Limited (formerly Zomato Ltd)

276- Bajaj Finance Q4 FY26 Analysis: Milestone AUM Growth & Robust Topline Performance

277- Waaree Energies Q4 FY26 Analysis: Blockbuster Topline Growth vs. Contracting Margins

278- Dr. Lal PathLabs Q4 FY26 Analysis: Volume-Led Growth vs. Rising Competitive Intensity

279- Kajaria Ceramics Q4 FY26 Analysis: Volume Resilience vs. Realization Headwinds

280- Mazagon Dock Q4 FY26 Analysis: Order Execution Powerhouse vs. Depleting Order Backlog

281- CDSL Q4 FY26 Analysis: Robust Account Additions vs. Surging IT & Compliance Costs

282- Avenue Supermarts (DMart) Q4 FY26 Analysis: Relentless Expansion vs. Normalizing Margin Efficiencies

283- Computer Age Management Services (CAMS) Q4 FY26 Analysis: Expanding Non-MF Moat vs. Regulatory Yield Compression

284- Godrej Properties (GODREJPROP) Q4 FY26 Analysis: Record Pre-Sales Surge vs. Execution Delays

285- Larsen & Toubro (L&T) Q4 FY26 Analysis: Record Execution Scale vs. Enduring Manpower Bottlenecks

286- Mahindra & Mahindra Q4 FY26 Analysis

287- Bajaj Auto Q4 FY26 Analysis

288- Polycab India Q4 FY26 Analysis

289- BSE Limited Q4 FY26 Analysis: Unprecedented F&O Traction vs. Elevated Regulatory Constraints

290- Wonderla Holidays Q4 FY26 Analysis: Premiumisation and Chennai Expansion vs. Climate Risks and Labor Codes

291- Pidilite Industries Ltd Q4 FY26 Analysis: Volume-Led Margin Expansion vs. Export Sluggishness & VAM Volatility

292- Balkrishna Industries (BKT) Q4 FY26 Analysis: Record Volume Expansion vs. Margin Contraction

293- Titan Company Q4 FY26 Analysis: Massive Revenue Surge vs. Operating Margin Pressures

294- ABB India Q1 CY2026 Analysis: Order Book Hits Record ₹11,000 Cr as Margins Suffer from Commodity Shock

295- Tata Consumer Products Q4 FY26 Analysis: Robust Margin Expansion vs. International Geopolitical Headwinds

296- Vedant Fashions Limited Q4 FY26 Analysis: Margin Resilience vs. Sluggish Store Expansion

297- Affle 3i Limited Q4 FY2026 Analysis: Resilient AI-Led Growth vs. Gross Margin Compression

298- State Bank of India (SBIN) Q4 FY26 Analysis: Historic Asset Quality vs. Unrelenting Margin Pressures

299- Dixon Technologies Q4 FY26 Analysis: Strong FY26 Finish vs. Near-Term Mobile Headwinds

300- NIITMTS Q4 FY26 Analysis: AI-Driven Strategic Pipeline vs. Macro-Induced Budget Pullbacks

301- Bharti Airtel Q4 FY26 Analysis: Strong Operational Momentum vs. ARPU Headwinds

302- HAL Q4 FY26 Analysis: Decisive Order Book Expansion vs. Engine-Supply Bottlenecks

303- Indian Railway Finance Corporation (IRFC) Q4 & FY26 Analysis: High-Margin Diversification Gains vs. Flat Quarterly Profit Growth

304- Voltas Limited Q4 FY26 Analysis: Progressive Volume Recovery vs. Sticky Margin Compression

305- ITC Hotels Q4 FY26 Analysis: Accelerating 'Asset-Right' Scale vs. Geopolitical Demand Headwinds

306- Solar Industries India Limited Q4 FY26 Analysis

307- Timken India Q4 FY26 Analysis: Historic Revenue Breakout vs. Margin Contraction Pressures

308- C.E. Info Systems Ltd (MapmyIndia) Q4 & FY26 Analysis: Decisive Q4 Sequential Inflection vs. Elongated Working Capital Cycles

309- Bharat Electronics Ltd (BEL) Q4 FY26 Analysis: Stellar Full-Year Revenue Beat vs. Near-Term Margin Contraction

310- PI Industries Q4 FY26 Analysis: Pharma CRAMS Resurgence vs. Agrochemical Downcycle Headwinds

311- Action Construction Equipment Ltd (ACE) Q4 FY26 Analysis: Robust Agriculture & Defence Ramping vs. Steel Inflation & Geopolitical Pressures

312- Apollo Hospitals Enterprise Ltd (APOLLOHOSP) Q4 FY26 Analysis: Robust Healthcare Services Growth vs. Digital Integration and Bed Expansion Costs

313- Jubilant FoodWorks Ltd Q4 FY26 Analysis: Stellar International Scale-Up vs. Near-Term Margin Inflation

314- LG Electronics India Q4 & FY26 Analysis: Record Revenue Scaling vs. EBITDA Margin Pressures

315- Page Industries Ltd Q4 FY26 Analysis: Robust Volume-Led Recovery vs. Persisting Input Inflation

316- Kwality Wall's (India) Q4 FY26 Analysis: Post-Demerger Scale vs. Profitability Squeeze

317- Info Edge (India) Ltd Q4 FY26 Analysis: Core Profitability Sustains Amidst Strategic Scaling

318- Netweb Technologies India Limited: Q4 & FY26 Performance Analysis

319- Siemens Energy India Limited (ENRIN): H1 FY26 Performance Analysis

320- NTPC FY26 Results: Why the Green Energy Pivot is a Game Changer for Investors.

321- Divi's Laboratories (DIVISLAB) Q4 FY26 Analysis: Custom Synthesis Moat vs. Supply Chain Headwinds

322- TCS Q1 FY27 Analysis: Scaling AI-Led Growth vs. Persistent Macro Headwinds

323- Amara Raja Energy & Mobility Q4 FY26 Analysis