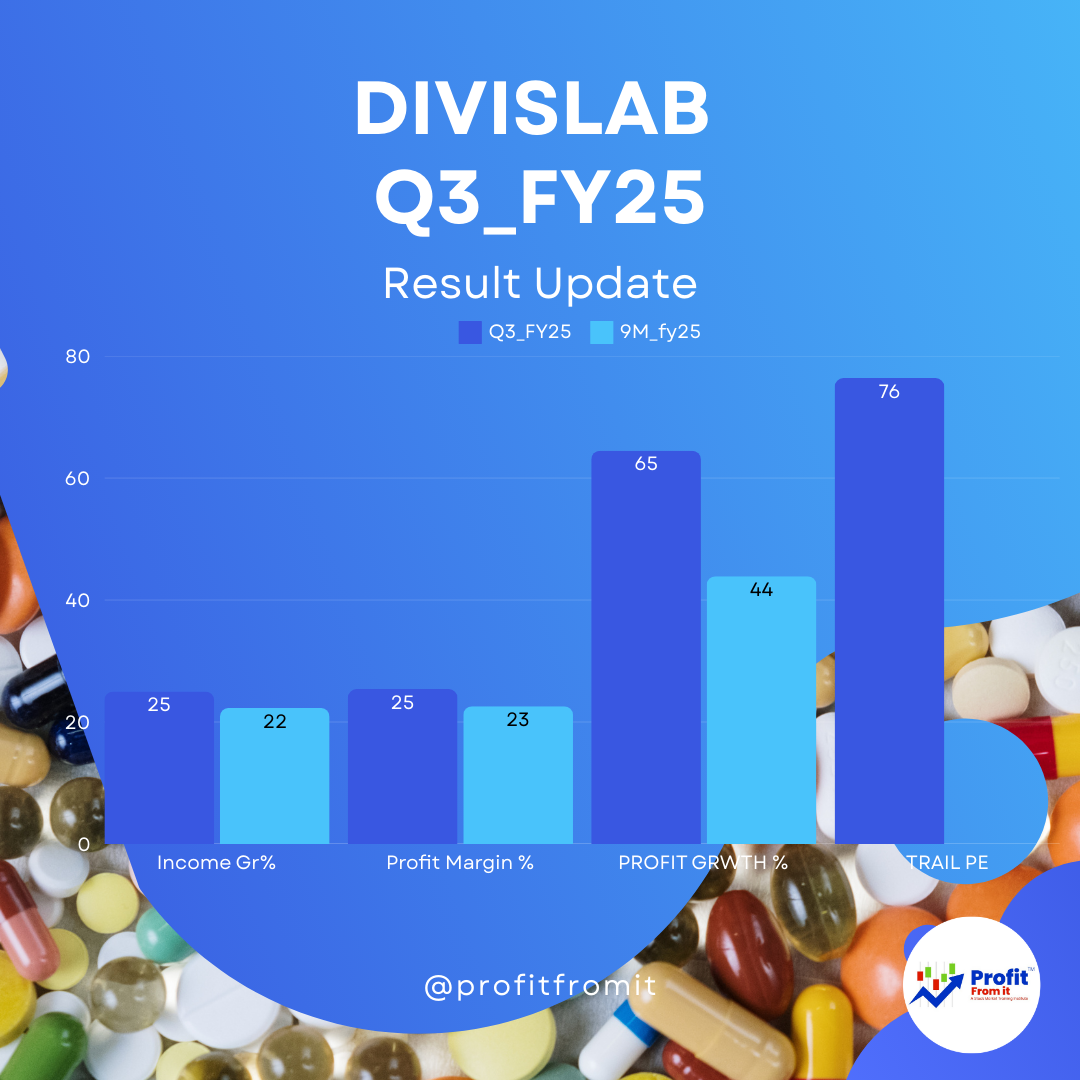

📢 Divis Laboratories Q3 FY25 & 9M FY25 Results - 📊💡

📌 Key Highlights

✅ Revenue Growth: Strong YoY growth in both Q3 FY25 & 9M FY25 📈

✅ Profitability: Higher PAT Margins & EBITDA Expansion 💰

✅ Capex Update: Kakinada Project (Unit-III) started operations from Jan 1, 2025 🏭

✅ Valuation: CMP ₹5,889 – Trading at a premium valuation 📊

1️⃣ Financial Performance 📊

📈 Consolidated Sales & Profit Growth

2️⃣ Margin Analysis 📊💰

📌 Higher EBITDA & PAT Margins indicate efficiency improvements & cost control ✅

📌 Slight dip in Gross Margin due to raw material costs ⚠️

3️⃣ Profitability, Solvency, & Liquidity Analysis 💰📊

📈 Profitability Ratios

🔹 RoE & RoCE show strong earnings growth, making the stock attractive 📈💰

🔹 Solvency & Liquidity 🏦

✅ Minimal debt, strong liquidity, and high cash reserves ensure financial stability 📉

4️⃣ Valuation Analysis 💰 CMP ₹5,889 & Trail EPS of 77.85

📌 Stock trades at a premium due to its strong financials & growth potential 💰📊

5️⃣ Outlook - Short & Long Term 📆

🔹 Near-Term (Next 1 Year)

✅ Revenue Growth Momentum Continues 🚀

✅ Margin Expansion Likely 💰

✅ Capacity Expansion (Kakinada) to Add Further Growth 🏭

⚠️ Risks: Currency fluctuations & raw material price volatility 🌍💰

🔹 Long-Term (2-5 Years)

✅ Strong API & Nutraceuticals Demand 📈

✅ Ongoing Expansion to Boost Production Capacity 🏭

✅ Robust R&D for Future Growth 🧪🔬

6️⃣ Final Verdict 🎯

📢 Exceptional Q3 & 9M FY25 results with strong profitability & growth. ✅

💰 Low debt, strong liquidity & margin expansion make it financially stable. 📊🏆

📈 Premium valuation reflects high growth potential but caution needed at CMP ₹5,889. 🚀

🔹 Investment View:

📍 Near-term traders: Hold, watch valuation risks ⚠️

📍 Long-term investors: Attractive for consistent returns in pharma sector 💼💊

💬 What’s your take on Divis Lab’s growth story? Comment below! 👇

#DivisLabs #StockMarket #Earnings #PharmaStocks #Investment #Q3Results

Class Sessions

1- IREDA’s latest quarterly results

2- Patanjali's Q2 FY25 financials

3- United Breweries Limited - Detailed Q2 FY25 Consolidated Financial Analysis

4- HDFC LIFE Q1 FY 2025

5- DMart Q1 FY 2025

6- HDFC LIFE Q1 FY 2025

7- Bajaj Auto Q1 FY24 Analysis

8- IREDA Q1 FY 2024

9- TCS Q1 FY 2025

10- HDFC Asset Management Company (HDFC AMC) Q1 FY25 Analysis

11- BAJAJ FINANCE | BEL | VOLTAS | LT | MARUTI SUZUKI Q3 Result Update 2024

12- How do you Analyse NBFC companies?

13- Which company is best for home appliances?

14- Who is No 1 construction company in India?

15- Aerospace & Defense Industry

16- Passenger Vehicle Market Share

17- Which is the No 1 small finance bank in India?

18- What is the position of steel market in India?

19- Tyres & Rubber Products INDUSTRY

20- Computers-Software & Consulting_q3_fy24

21- Which is the best stock in Consumer Food? Watch Now

22- Auto Sector Vehicle January Data

23- Telecom Industry in India: Sector Overview

24- Comparision: Reliance Retail | Dmart | ShoppersStop | Spencer | Vmart

25- ICICI GI, Supreme Industry, Asian Paint & Ultratech Cement | Q3 FY2024 Result Update

26- TCS, Dmart, HDFC AMC & HDFC LIFE Q3 FY2024 Result Update

27- LTTS, MAPMYINDIA, HDFC BANK Q3 FY2024 Result Update

28- Hospital Industry Analysis

29- Industry Update

30- Tata Consultancy Services Ltd Q4 Result Update 2023

31- Ultratech Cement Latest News | Q4 Result 2023

32- Q4 Result 2023

33- Q3 Result Update 2023

34- Student Page Video

35- Live Query Sessions Video Updated

36- TCS's Q3 FY25: (Leading Company from Computers - Software & Consulting Industry)

37- TATAELXSI's Q3 FY25:

38- IREDA's Q3 FY25:

39- Avenue Supermarts Limited's (DMart) financial results for the third quarter ended December 31, 2024:

40- HDFC Asset Management Company's financial results for Q3 FY25:

41- HDFC Life Q3 FY25 Analysis 📊

42- L&T Technology Services Q3 FY25

43- Havells Q3 FY25 Analysis 📊

44- Reliance Industries' Financial Results for Q3 FY25 📊

45- ICICI Lombard's performance for Q3 FY25”

46- Q3 FY25 Supreme Industries Ltd. 📊

47- Indian Railway Finance Corporation Limited (IRFC) for Q3 FY25:

48- Zomato's Q3 FY25 financial results:

49- Dixon Technologies (India) Ltd. Q3 FY25 Results 📊

50- HDFC BANK Q3 FY25 Results 📊

51- Hindustan Unilever Q3 FY25 Results 📊

52- Pidilite Industries Limited's Q3 FY25:

53- UltraTech Cement Limited for the third quarter (Q3) and the first nine months (9MFY) of the financial year 2025:

54- Indian Energy Exchange (IEX) Q3 FY25:

55- AU Small Finance Bank Limited's Q3 FY25:

56- Indigo Airlines' performance for Q3 FY25: Overview: 🚀

57- Balkrishna Industries Q3 FY25 Performance Analysis 📊

58- CDSL's financial results for Q3 FY25: Key Insights and Highlights

59- EMS Limited's financial results for Q3 FY25:

60- JSW Steel's Q3 FY25 financial performance:

61- Wonderla Holidays Limited Q3 FY25 Analysis 📊

62- Bajaj Housing Finance's latest results for Q3 FY25;

63- Route Mobile's latest financial results for Q3 FY25:

64- Bajaj Auto Q3 FY25 Consolidated Financial Analysis:

65- Maruti Suzuki India Limited (MSIL) - Q3 FY25 Financial Highlights and Analysis 📊

66- Q3 FY25 results for C.E. Info Systems Limited (MapMyIndia)

67- Bajaj Finance's Q3 FY25: 📊

68- Voltas' Q3 FY25 financial results:

69- 📢 BEL Q3 FY25 Results – Key Insights & Analysis 🚀

70- 📊 Waaree Energies Q3 FY25 and 9M FY25 Performance Analysis 🚀

71- 📊 Dr Lal PathLabs - Q3 FY25 & 9M FY25 Financial Analysis & Insights 🚀

72- Larsen & Toubro Q3 FY 25: 🚀📊📈

73- 📊 Analysis of Tata Consumer Products Q3 FY25 & 9M FY25 Results 📈

74- 📊 Manyavar (Vedant Fashions Ltd.) Q3 FY25 Earnings

75- Nestlé India Q3 FY25 results:

76- 📢 Divis Laboratories Q3 FY25 & 9M FY25 Results - 📊💡

77- 🎨 Asian Paints Q3 FY25 & 9M FY25 Financial Analysis & Insights 📊

78- 📊 Godrej Properties Q3 FY25 Analysis 🏗️

79- 📊 Kajaria Ceramics Q3 FY25 Analysis 📊

80- 📊 Titan Q3 FY25 & 9M FY25 Performance Analysis 🔥🚀

81- 🚀 InfoEdge Q3FY25 Results Analysis & Insights 📊

82- 📊 Page Industries Q3 FY25 Analysis & Investment Insights 🏭📈

83- 📢 SBI Q3FY25 Earnings Analysis & Insights 📊🏦

84- 📊 PI Industries Q3 FY25 Results - Analysis & Insights 🔍

85- 🚀 Amara Raja Batteries (ARE&M) Q3 FY25 Results Analysis and Insights 📊

86- 📊 Affle (India) Limited Q3 & 9M FY2025 Earnings Analysis & Insights 🚀

87- 📊 Patanjali Foods Limited Q3 FY25 Financial Analysis & Key Insights 🚀

88- 📊 Apollo Hospitals Q3FY25 & 9MFY25 Financial and Operational Analysis

89- 🚄 IRCTC Q3FY25 Earnings Analysis & Insights 📊💡

90- 🎯 Jubilant FoodWorks Q3FY25 & 9MFY25 Key Highlights 🚀🔥

91- 📊 UBL Q3 FY25 & 9M FY25 Performance Analysis – Investor Insights 💹

92- 🚢 Mazagon Dock Shipbuilders: Q3FY25 & 9MFY25 Analysis

93- 📈 TCS FY25 Results: Muted CC Growth, Hence Low Sales & Profit Growth in Headwind Environment, but valuations near to favourable.

94- 🔋 IREDA Q4FY25 Results: Powered by Growth, Poised for the Future

95- 📊 ICICI Lombard General Insurance – FY25 & Q4 FY25 Results Update

96- 🔍 HDFC AMC Q4FY25 & FY25 Results: Strong Performance, Robust Growth & Healthy Margins

97- 📈 HDFC Life FY25 Results: Strong Growth, Steady Profits & Enhanced Market Position

98- 📊 Tata Elxsi Q4FY25 & FY25 Review: Growth Foundations Amidst Headwinds

99- 🔍 HDFC Bank – FY25 & Q4FY25 Results Highlights

100- 📊 Havells FY25 Results Analysis: Robust Growth with Strategic Resilience

101- Waaree Energies Ltd. (WAAREEENER) FY25 Results Update & Investor Insights

102- 📊 AU Small Finance Bank Q4 & FY25 Results – Growth Anchored by Profitability & Prudent Risk Management

103- Bajaj Housing Finance Ltd. – FY25 Financial Performance Highlights and Analysis

104- Tata Consumer FY25 & Q4FY25 Summary: Strong Growth with Margin Recovery on the Horizon

105- L&T Technology Services (LTTS) Q4 FY25 & FY25 Results Analysis

106- Hindustan Unilever Limited (HUL) FY25 & Q4FY25 Results Update

107- 📊 Nestlé India Limited – FY25 & Q4FY25 Results Analysis

108- 📊 IEX FY25 and Q4FY25 Results Analysis

109- Supreme Industries Limited – FY25 Financial Results Update

110- Maruti Suzuki FY25 Results Update: Key Insights and Strategic Highlights

111- Reliance Industries Limited – FY25 Results Update

112- UltraTech Cement FY25 Results Update: Driving Consolidated Growth Amidst Strategic Expansions

113- Bajaj Finance Limited – Q4FY25 and FY25 Financial Results Update

114- 📊 Eternal Limited – Q4FY25 & FY25 Financial and Strategic Performance Update

115- 🏢 Godrej Properties Q4 & FY25 Result Analysis: Booking Boom & Financial Resilience

116- 🧾 DMart Q4 FY25 & FY25 Result Highlights – Resilient Growth Amid Operational Pressures

117- 📊 CDSL Q4 & FY25 Result Analysis

118- 📊 Kajaria Ceramics Q4 FY25 Results Analysis 📈

119- Manyavar (Vedant Fashions Limited) Q4 FY25 Financial Analysis

120- Wonderla Holidays Q4FY25 & FY25 Financial Analysis: Strong Footfalls Despite Market Headwinds

121- 📊 Voltas Q4 FY25 Financial Analysis: Detailed Investor Insights

122- 📊 Route Mobile Q4 FY25 & FY25 Financial Analysis

123- United Breweries Limited (UBL) Q4 FY25 Financial Analysis

124- Asian Paints Q4 FY25 Financial Analysis: Detailed Investor Insights

125- Pidilite Industries Q4 FY25 Financial Analysis

126- Larsen & Toubro (L&T) Q4 FY25 & FY25 Financial Analysis

127- 📊 Titan Company Ltd. Q4 FY25 & FY25 Financial Performance Analysis

128- Affle 3I Q4 & FY25 Results: Strong Growth

129- Divi's Laboratories Q4 & FY25 Results: ₹2,209 Cr Profit, ₹30 Dividend, CMP ₹6,539 | Long-Term Outlook & Valuation

130- ITC Hotels Q4 & FY25 Results: 73% Profit Growth | ₹202 CMP Valuation & Expansion Outlook

131- Patanjali Foods Q4 FY25 Results: 70% PAT Growth | Highest Ever Revenue Achieved

132- Jubilant FoodWorks Q4 & FY25 Results: Delivery Growth, Store Expansion & Financial Insights

133- 🚗 MapmyIndia Q4 FY25 & FY25 Results: Strong Momentum in Tech & Mobility

134- 🧾 Page Industries Q4 & FY25 Result Update Brand:

135- 🇮🇳 Bharat Electronics Ltd – Q4 & FY25 Financial Results & Investor Insights 🔍

136- 🔬 PI Industries Ltd – Q4 & FY25 Results Review | Growth, Margins, and Outlook

137- 📊 Dixon Technologies (India) Ltd – Q4 FY25 & FY25 Financial Results Analysis

138- 🧬 Dr. Lal PathLabs Q4 & FY25 Results: Strategic Growth Beyond Metro Markets

139- 🛫 IndiGo Q4 FY25 Results: Record Profits, Rising Passengers & Strong Outlook

140- 🚜 Balkrishna Industries Ltd – Q4 & FY25 Results Update: Strong Long-Term Strategy Despite Soft Q4

141- Info Edge (India) Ltd. Q4 FY25 & FY25 Results Analysis: Detailed Investor Insights

142- 📊 Bajaj Auto Q4 FY25 & FY25 Financial Highlights: Growth, Resilience, & Green Momentum

143- IRCTC Q4 & FY25 Results: Insights for Investors

144- 🚢 Mazagon Dock Q4 & FY25 Results:

145- 🏥 Apollo Hospitals FY25 Results: Strong Performance Backed by Expansion Plans

146- 📊 TCS Q1 FY26 Financial Performance: Comprehensive Investor Guide

147- United Breweries Ltd (UBL) Q4 & FY25 Results Analysis: Brewing Growth with Consistency

148- Q1 FY26 Financial Analysis of IREDA

149- Tata Elxsi Q1 FY26 Financial Results: Comprehensive Analysis

150- 🏪 DMart Q1 FY26 Financial Results: Stable Growth Amid Margin Pressure

151- HDFC Life Q1 FY26 Results: Strong Momentum Continues in Life Insurance

152- ICICI Lombard General Insurance Q1 FY26 Results Analysis: Stable Growth Amid Regulatory Changes

153- ITC Hotels Q1 FY26 Results: Record Performance, Robust Growth, and Long-Term Outlook

154- L&T Technology Services Ltd (LTTS) Q1 FY26 Results: Investor Analysis

155- HDFC AMC Q1 FY26 Results Analysis: Strong Performance & Strategic Positioning

156- Reliance Q1 FY26 Results: Record-Breaking Profits & Multi-Engine Growth 🚀

157- HDFC Bank Q1 FY26 Results: Growth Resilient, Bonus Announced! 🚀🏦

158- 🚦 AU Small Finance Bank (AUBank) Q1 FY26 Results Analysis: Strengths & Concerns at CMP ₹795

159- 📊 Havells India Q1 FY26 Results Analysis at CMP ₹1532

160- 🏗️ UltraTech Cement Q1 FY26 Results: Strong Growth, Margin Recovery & Capacity Expansion 🚀

161- Eternal Limited (Zomato) Q1 FY26 Results: Revenue Surges 70%, Quick Commerce Leads Growth

162- 🏭 Kajaria Ceramics Q1 FY26 Results: Margins Improve Amidst Soft Demand 📊

163- 🚆 IRFC Q1 FY26 Results: Strongest-Ever Quarterly Performance! 📈

164- ⚡ IEX in Flux: Q1 FY26 Results Amid Market Coupling Shock

165- 📊 Dixon Technologies Q1 FY26: Strong Growth Amid Strategic Expansions

166- 🏠 Bajaj Housing Finance – Q1 FY26 Result Highlights

167- 📊 Tata Consumer Products – Q1 FY26 Results: Steady Topline, Margin Challenges

168- 📊 Bajaj Finance Q1 FY26 Results: Solid Growth, AI-led Efficiency, and Asset Quality Focus! 💼

169- 📊 Nestlé India Q1 FY26 Results Analysis

170- 🏭 Supreme Industries Q1 FY26 Results: Volume Up, Profit Down — What’s Next? 📊

171- 📊 CDSL Q1 FY26 Results: Marginal Growth in Revenue, Digital Strategy Intact 🧾🔍

172- 🧾 Balkrishna Industries Q1 FY26 Result Analysis 🛞

173- 📊 Affle Q1 FY26 Financial Performance: Resilient Growth with Focused Execution

174- Bharat Electronics Limited (BEL) Q1 FY26 Results Analysis 📊

175- Waaree Energies Ltd Q1 FY26 Results Analysis

176- Asian Paints Q1 FY26 Results: Analysis with Key Insights & Outlook 🏭🎨

177- 🚧 Larsen & Toubro Q1 FY26 Results – Record Order Book, Global Growth, and Margin Watch Ahead

178- 🚗 Maruti Suzuki Q1 FY26 Results – Steady Profit, Strong Exports, But Margins Under Pressure

179- 👔 Manyavar (Vedant Fashions Ltd) Q1 FY26 Results – Steady Growth Amidst Mixed Market Sentiments

180- ✈️ IndiGo Q1 FY26 Results – Navigating Headwinds, Flying Towards Growth!

181- Intrinsic Valuation & Wealth Building – After Class Review

182- 🎥 Session Replay (YouTube Live): Intrinsic Valuation & Wealth Building: Fair Value, Margin of Safety & Allocation Strategy

183- Godrej Properties Q2 FY2026 Analysis: Scaling New Heights 🏙️📈

184- ✈️ IndiGo Q2 FY26: Currency Turbulence vs. Operational Resilience

185- IREDA Q3FY26 Results: Green Energy Giant Hits Record Profits—Time to Buy?

186- DMart (Avenue Supermarts) Q3 FY26 Results Analysis: Margin Expansion Amidst Steady Growth

187- TCS Q3 FY26 Results Analysis: AI Momentum vs. Statutory Headwinds

188- Tata Elxsi Q3 FY26 Results Analysis: Healthy Margin Expansion Amidst Steady Revenue Growth

189- ICICI Lombard (ICICIGI) Q3FY26 Analysis: Navigating Industry Shifts with Resilience

190- HDFC AMC Q3 FY26 Results Analysis: Steady Growth Amid Industry Tailwinds

191- HDFC Life: Driving Protection Momentum in Q3 FY26

192- LTTS Q3FY26 Analysis: Strategic Pivot Towards "Engineering Intelligence"

193- Reliance Industries Q3 FY26 Financial Analysis & Investment Insights

194- AU Small Finance Bank Q3FY26 Results: A Deep Dive into 26% Profit Growth and Strategic Expansion

195- HDFC Bank Q3FY26 Analysis: Navigating the Glide Path with Disciplined Growth

196- Havells Q3 FY26 Analysis: Robust Revenue Growth Amidst Margin Headwinds

197- IRFC Q3FY26 Results: Record Profits and Strategic Pivot Under "IRFC 2.0"

198- ITC Hotels Q3FY26 Analysis: Record Revenues & Strategic Scalability

199- Supreme Industries Q3 FY26: Resilient Volumes Amid Pricing Headwinds

200- Eternal Limited Q3FY26 Results: Quick Commerce Turns Profitable!

201- Waaree Q3 FY26 Analysis: Record-Breaking Growth Fuels Aggressive 'Waaree 2.0' Expansion

202- IndiGo Q3FY26 Results Analysis: Navigating Turbulence with Resilient Fundamentals

203- UltraTech Cement Q3FY26 Results: A Masterclass in Operational Efficiency

204- What is the policy repo rate as decided by the Monetary Policy Committee in its February 2026 meeting?

205- Asian Paints Q3FY26: Resilience Amidst Competitive Intensity

206- Tata Consumer Q3FY26: Strong Volume Growth and Margin Expansion Steer Performance

207- Bharat Electronics Ltd (BEL): A High-Octane Q3 Performance Analysis

208- BKT Q3FY26 Results: Resilient Volume Rebound Amid Global Headwinds

209- L&T Q3 FY26 Analysis: A ₹7 Lakh Crore Milestone in Engineering Excellence

210- Maruti Suzuki Q3 FY'26 Results: A Deep Dive into "The GST Bounce Back"

211- Dixon Technologies Q3 FY26 Analysis: Transitioning to a Design-Led Component Giant

212- IEX Q3FY26 Results: Powering Through Energy Transitions

213- Voltas Q3 FY26 Results Analysis: Leadership Strengthened Amid Seasonality

214- Bajaj Auto Q3 FY26 Analysis: Record-Breaking Performance as Exports and EVs Scale New Peaks

215- Dr. Lal PathLabs Q3 FY26 Analysis: Steady Revenue Amidst Seasonal Headwinds & One-Off Costs

216- Nestle India Q3FY26 Results: Record Turnover and Five-Year High Volume Growth

217- Kajaria Ceramics Q3 FY26 Analysis: Efficiency Gains Meet Muted Demand

218- Affle 3i Limited Q3 FY2026 Analysis: AI-Driven Milestone Performance

219- CDSL Q3FY26 Analysis: Demat Dominance Continues Amidst Shifting Revenue Mix

220- Bajaj Housing Finance Ltd. (BAJAJHFL) Q3 FY26 Results Analysis

221- Bajaj Finance Q3 FY26 Analysis: Robust AUM Scaling vs. Rising Cost of Funds

222- Pidilite Q3 FY26 Consolidated Analysis: Volume-Led Mastery Amidst Input Cost Tailwinds

223- Wonderla Holidays Ltd. Q3 FY26 Analysis: Record Revenue vs. Margin Pressure from New Launches

224- Godrej Properties Q3 FY26 Analysis: Blockbuster Pre-Sales vs. Operational Revenue Paradox

225- Page Industries Q3 FY26 Analysis: Steady Growth Meets One-Time Regulatory Hurdles

226- Mazagon Dock Shipbuilders Q3 FY26 Analysis: Order Book Execution vs. Margin Normalization

227- State Bank of India Q3 FY26 Analysis: Credit Engine Fires Up vs. Margin Compression Concerns

228- Apollo Hospitals Q3 FY26 Analysis:

229- Titan Company Q3 FY26 Analysis: Dominant Revenue Surge vs. Margin Compression Tailwinds

230- Jubilant FoodWorks Q3 FY26 Analysis: Robust Topline Growth vs. Margin Compression Challenges

231- Amara Raja Energy & Mobility Q3 FY26 Analysis: New Energy Resilience vs. Profitability Headwinds

232- LG Electronics India Q3 FY26 Analysis: Premium Momentum vs. High-Base Moderation

233- Patanjali Foods Q3 FY26 Analysis: Record Revenue Surge vs. Operating Margin Pressure

234- Divi's Laboratories Q3 FY26 Analysis: Custom Synthesis Resilience vs. Margin Pressure from Labor Transitions

235- IRCTC Q3 FY26 Analysis: Robust Ticketing Momentum vs. Tourism Segment Volatility

236- PI Industries Q3 FY26 Analysis: Navigating a Challenging Global Cycle

237- Manyavar (Vedant Fashions) Q3 FY26 Analysis: Robust Margin Retention vs. Moderating Same-Store Growth

238- Info Edge (Naukri) Q3 FY26 Analysis: Recruitment Resilience vs. Non-Recruitment Cash Burn

239- EMS Limited Q3 FY26 Analysis: Order Book Resilience vs. Bottom-line Pressure

240- MapmyIndia (C.E. Info Systems) Q3 FY26: Seasonal Headwinds vs. Record Order Book

241- Q3fy26_Results Update for 55 Focused Companies Spread Sheet

242- Q3 FY26 Earnings Masterclass: The Turning Point for Indian Corporates

243- Trent Limited Q3 FY26 Analysis: Aggressive Expansion vs. Bottom-line Normalization

244- NIIT Learning Systems Q3 FY26 Analysis: Scaling AI-Led L&D vs. Margin Dilution Risks

245- Bharti Airtel Q3 FY26 Analysis: Premiumization Lead vs. High Capex Intensity

246- HAL Q3 FY26 Analysis: Execution Momentum vs. Rising Employee Liabilities

247- Siemens Energy India (ENRIN) Q1 FY26 Analysis: Robust Backlog Execution vs. Elevated Valuations & One-Off Labor Costs

248- ABB India Q4 CY2025 Analysis: Record Order Inflows vs. Margin Headwinds

249- Siemens Limited Q5 FY25 Analysis: Structural Tailwinds vs. Capital Allocation Discipline

250- Polycab Q3 FY26 Analysis: Record Top-line Growth vs. Margin Compression

251- Solar Industries Q3 FY26 Analysis: Record Defense Execution vs. Sluggish Domestic Mining

252- Mahindra & Mahindra Q3 FY26 Analysis: Breakthrough Services vs. Commodity Inflation Headwinds

253- Cummins India Q3 FY26 Analysis: Steady Domestic Growth Meets Export Headwinds

254- Timken India Limited Q3 FY26 Analysis: Revenue Resiliency vs. Transitional Margin Pressure

255- 🚜 Investment Report: Construction Vehicles Industry

256- TCS Q4 FY26 Analysis: The AI Growth Engine vs. Macro Headwinds

257- Action Construction Equipment (ACE) Q3 FY26 Analysis: Margin Mastery vs. Volume Headwinds

258- Netweb Technologies Q3 FY26 Analysis: AI Tsunami vs. Supply Chain Headwinds

259- ICICI Lombard Q4 FY26 Analysis: Growth Momentum vs. Loss Ratio Headwinds

260- HDFC AMC Q4 FY26 Analysis: Market Share Gains vs. Yield Pressure

261- HDFC Life Q4 FY26 Analysis: Robust Premium Growth vs. Regulatory Margin Pressures

262- CRISIL Q1 FY26 Analysis: 46% Profit Surge vs. Dynamic Operating Costs

263- HDFC Bank Q4 FY26 Analysis: Liquidity Rebound vs. Margin Compression Resistance

264- Nestlé India Q4 FY26 Analysis

265- Tata Elxsi Q4 FY26 Analysis: Resilient Revenue Growth vs. The Exceptional Cost Hurdle

266- Havells India Q4 FY26 Analysis: Steady Cable Demand vs. The Summer Letdown

267- IEX Q4 FY26 Analysis: Record Volumes vs. Regulatory Overhang

268- Trent Limited Q4 FY26 Analysis: Aggressive Expansion vs. Consumption Softness

269- Reliance Industries Q4 FY26 Analysis: Telecom & Retail Resilience vs. O2C Margin Headwinds

270- UltraTech Cement Q4 FY26 Analysis: Historic 200 MTPA Milestone vs. Geopolitical Cost Headwinds

271- Bajaj Housing Finance Q4 FY26 Analysis: Record Earnings vs. Margin Pressure

272- AU Small Finance Bank Q4 FY26 Analysis: Universal Ambitions vs. NIM Pressure

273- Supreme Industries Q4 FY26 Analysis: Volume Leadership vs. Margin Expansion

274- Maruti Suzuki Q4 FY26 Analysis: Record Top-line Growth vs. Margin Pressure

275- Eternal Limited (formerly Zomato Ltd)

276- Bajaj Finance Q4 FY26 Analysis: Milestone AUM Growth & Robust Topline Performance

277- Waaree Energies Q4 FY26 Analysis: Blockbuster Topline Growth vs. Contracting Margins

278- Dr. Lal PathLabs Q4 FY26 Analysis: Volume-Led Growth vs. Rising Competitive Intensity

279- Kajaria Ceramics Q4 FY26 Analysis: Volume Resilience vs. Realization Headwinds

280- Mazagon Dock Q4 FY26 Analysis: Order Execution Powerhouse vs. Depleting Order Backlog

281- CDSL Q4 FY26 Analysis: Robust Account Additions vs. Surging IT & Compliance Costs

282- Avenue Supermarts (DMart) Q4 FY26 Analysis: Relentless Expansion vs. Normalizing Margin Efficiencies

283- Computer Age Management Services (CAMS) Q4 FY26 Analysis: Expanding Non-MF Moat vs. Regulatory Yield Compression

284- Godrej Properties (GODREJPROP) Q4 FY26 Analysis: Record Pre-Sales Surge vs. Execution Delays

285- Larsen & Toubro (L&T) Q4 FY26 Analysis: Record Execution Scale vs. Enduring Manpower Bottlenecks

286- Mahindra & Mahindra Q4 FY26 Analysis

287- Bajaj Auto Q4 FY26 Analysis

288- Polycab India Q4 FY26 Analysis

289- BSE Limited Q4 FY26 Analysis: Unprecedented F&O Traction vs. Elevated Regulatory Constraints

290- Wonderla Holidays Q4 FY26 Analysis: Premiumisation and Chennai Expansion vs. Climate Risks and Labor Codes

291- Pidilite Industries Ltd Q4 FY26 Analysis: Volume-Led Margin Expansion vs. Export Sluggishness & VAM Volatility

292- Balkrishna Industries (BKT) Q4 FY26 Analysis: Record Volume Expansion vs. Margin Contraction

293- Titan Company Q4 FY26 Analysis: Massive Revenue Surge vs. Operating Margin Pressures

294- ABB India Q1 CY2026 Analysis: Order Book Hits Record ₹11,000 Cr as Margins Suffer from Commodity Shock

295- Tata Consumer Products Q4 FY26 Analysis: Robust Margin Expansion vs. International Geopolitical Headwinds

296- Vedant Fashions Limited Q4 FY26 Analysis: Margin Resilience vs. Sluggish Store Expansion

297- Affle 3i Limited Q4 FY2026 Analysis: Resilient AI-Led Growth vs. Gross Margin Compression

298- State Bank of India (SBIN) Q4 FY26 Analysis: Historic Asset Quality vs. Unrelenting Margin Pressures

299- Dixon Technologies Q4 FY26 Analysis: Strong FY26 Finish vs. Near-Term Mobile Headwinds

300- NIITMTS Q4 FY26 Analysis: AI-Driven Strategic Pipeline vs. Macro-Induced Budget Pullbacks

301- Bharti Airtel Q4 FY26 Analysis: Strong Operational Momentum vs. ARPU Headwinds

302- HAL Q4 FY26 Analysis: Decisive Order Book Expansion vs. Engine-Supply Bottlenecks

303- Indian Railway Finance Corporation (IRFC) Q4 & FY26 Analysis: High-Margin Diversification Gains vs. Flat Quarterly Profit Growth

304- Voltas Limited Q4 FY26 Analysis: Progressive Volume Recovery vs. Sticky Margin Compression

305- ITC Hotels Q4 FY26 Analysis: Accelerating 'Asset-Right' Scale vs. Geopolitical Demand Headwinds

306- Solar Industries India Limited Q4 FY26 Analysis

307- Timken India Q4 FY26 Analysis: Historic Revenue Breakout vs. Margin Contraction Pressures

308- C.E. Info Systems Ltd (MapmyIndia) Q4 & FY26 Analysis: Decisive Q4 Sequential Inflection vs. Elongated Working Capital Cycles

309- Bharat Electronics Ltd (BEL) Q4 FY26 Analysis: Stellar Full-Year Revenue Beat vs. Near-Term Margin Contraction

310- PI Industries Q4 FY26 Analysis: Pharma CRAMS Resurgence vs. Agrochemical Downcycle Headwinds

311- Action Construction Equipment Ltd (ACE) Q4 FY26 Analysis: Robust Agriculture & Defence Ramping vs. Steel Inflation & Geopolitical Pressures

312- Apollo Hospitals Enterprise Ltd (APOLLOHOSP) Q4 FY26 Analysis: Robust Healthcare Services Growth vs. Digital Integration and Bed Expansion Costs

313- Jubilant FoodWorks Ltd Q4 FY26 Analysis: Stellar International Scale-Up vs. Near-Term Margin Inflation

314- LG Electronics India Q4 & FY26 Analysis: Record Revenue Scaling vs. EBITDA Margin Pressures

315- Page Industries Ltd Q4 FY26 Analysis: Robust Volume-Led Recovery vs. Persisting Input Inflation

316- Kwality Wall's (India) Q4 FY26 Analysis: Post-Demerger Scale vs. Profitability Squeeze

317- Info Edge (India) Ltd Q4 FY26 Analysis: Core Profitability Sustains Amidst Strategic Scaling

318- Netweb Technologies India Limited: Q4 & FY26 Performance Analysis

319- Siemens Energy India Limited (ENRIN): H1 FY26 Performance Analysis

320- NTPC FY26 Results: Why the Green Energy Pivot is a Game Changer for Investors.

321- Divi's Laboratories (DIVISLAB) Q4 FY26 Analysis: Custom Synthesis Moat vs. Supply Chain Headwinds

322- TCS Q1 FY27 Analysis: Scaling AI-Led Growth vs. Persistent Macro Headwinds

323- Amara Raja Energy & Mobility Q4 FY26 Analysis