Titan Company Q4 FY26 Analysis: Massive Revenue Surge vs. Operating Margin Pressures

As corporate investment advisors, we constantly look for structural compounders that can navigate high inflation and volatile commodity prices. Titan Company Limited (TITAN)—the crown jewel of the Tata Group retail ecosystem—released its audited consolidated financial results for Q4 FY26 on May 8, 2026.

The headline is a breathtaking top-line delivery offset by short-term margin compression. Below, we break down the operational realities, forensic details, and valuation guardrails to help our clients and finance students understand if this premium-valued giant is still a "Buy" or a "Hold."

📊 The Snapshot

Note: Market Capitalization is calculated based on $88.78 \text{ Crore}$ outstanding shares at the CMP of ₹4,081.

🔥 The 'Wow' Factor

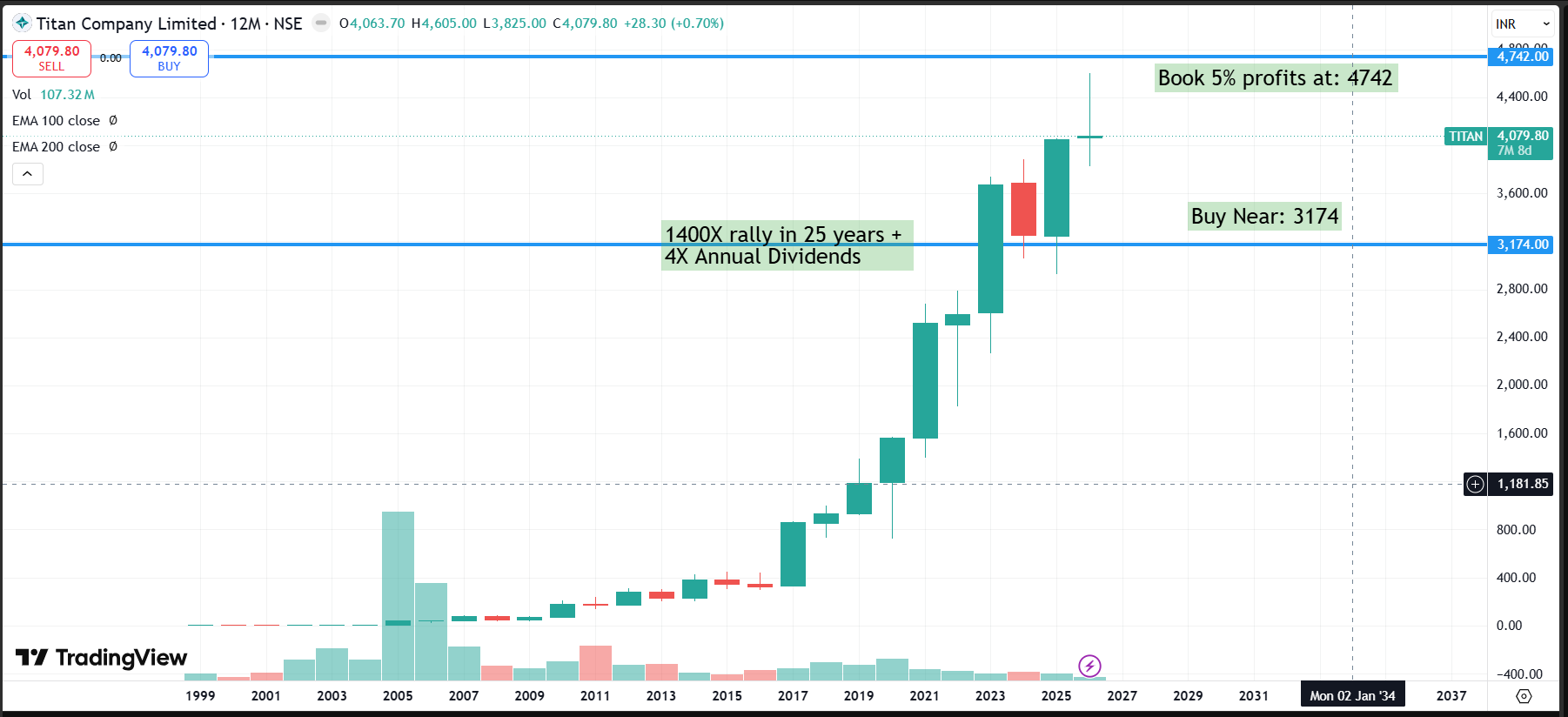

The ₹75,000 Crore Annual Milestone: Titan crossed the historic milestone of ₹75,000 Crore in consolidated annual revenue in FY26, adding an incredible ₹25,000 Crore in a single year. To put this in perspective, it took Titan nearly 40 years to cross the ₹50,000 Crore milestone in FY25!

Surging Bullion Demands: Bullion and digital gold sales skyrocketed to ₹6,699 Crore in Q4 FY26 alone (accounting for nearly $25\%$ of total sales), driven by consumers rushing to buy gold coins and exchange older gold amid record-high gold prices.

The Global Push (Damas Integration): During FY26, Titan completed its $67\%$ acquisition of GCC-based heritage brand Damas Jewellery for a total consideration of ₹2,858 Crore. This added 123 retail stores across the Middle East, transforming Titan into a formidable multinational jeweler.

Superlative Performance Bonuses: Demonstrating high employee-centricity, Titan distributed a one-time "special performance reward" of approximately ₹100–120 Crore to its employees and associates in Q4, celebrating the landmark FY26 performance.

📈 Operational KPIs

To evaluate a retail powerhouse like Titan, we must look past high-level financials and examine sector-specific physical performance metrics:

🔍 Financial Deep Dive (Consolidated)

A forensic examination of the consolidated income statement reveals a clear picture of high growth operating under heavy product-mix headwinds.

Note: Reported PAT includes an exceptional gain of ₹51 Crore from the reversal of labor code provisions.

Cost vs. Efficiency Analysis

While top-line growth is stellar, our Margin of Safety filter flags a few operational cost expansions:

The Raw Material Drag: The ratio of raw materials to revenue expanded from $77.2\%$ in Q4 FY25 to $83.2\%$ in Q4 FY26. This was driven by a negative product mix—mainly a sharp jump in low-margin bullion sales and gold coins (which carry near-zero manufacturing margins).

Special Employee Rewards: Unallocated corporate expenses shot up due to the ₹100–120 Crore special performance payout. This is a temporary headwind, showing management’s high integrity, but it did suppress short-term EBITDA.

GCC Geopolitical Disruptions: Titan's newly acquired international business (Damas and Tanishq GCC) suffered a Q4 operational loss of ₹82 Crore due to severe weather and geopolitical events in March, alongside restructuring and integration outlays.

Transfer Pricing Adjustments: Titan formalized transfer pricing whereby international subsidiaries act as low-risk distributors, generating an ₹80 Crore standalone adjustment that successfully neutralizes on a consolidated basis.

Marketing Efficiencies: On a positive note, advertising costs were managed prudently, dropping as a percentage of revenue to $1.5\%$ (₹394 Crore) from $2.1\%$ (₹320 Crore) YoY.

🤝 Peer Benchmarking: Titan vs. Kalyan Jewellers

To provide perspective for fund clients, we benchmark Titan against its closest listed pure-play competitor, Kalyan Jewellers India Limited (KALYANKJIL), for Q4 FY26:

🔮 The Forward Curve (Outlook for Q1 & Q2 FY27)

Long-Term Guidance Intact: Management reiterated its structurally confident guidance of $15-20\%$ compound annual growth rate (CAGR) for the jewelry segment over the medium term.

Q1 FY27 Projections: On-ground demand during the crucial Akshaya Tritiya festival was highly robust. We project Q1 FY27 consolidated revenue to scale to approximately ₹28,500 Crore ($+18-20\%$ YoY growth), supported by strong wedding season purchase orders.

EBITDA Margin Recovery: We anticipate EBITDA margins to rebound toward the normalized $11.0\% - 11.5\%$ range by Q2 FY27 as integration costs for Damas drop and the retail mix shifts back toward high-margin studded diamond collections.

🛡️ Valuation Guardrails

To determine if Titan is trading with an adequate margin of safety, we look at historical valuations:

$$\text{Current PE} = \frac{\text{CMP}}{\text{TTM EPS}} = \frac{₹4,081}{₹57.14} \approx 71.4\text{x}$$

Historical PE Comparison: Titan's 5-year median PE stands at approximately $75.0\text{x}$. At $71.4\text{x}$, the stock is Fairly Valued to Marginally Discounted relative to its historical premium.

Book Value Status: The stock trades at $\sim 23\text{x}$ book value (Book Value per share $\approx$ ₹177). It remains categorized as Trading at a Premium from an asset-backing perspective, which is typical for asset-light franchisee retail models.

🔑 Shareholding and Integrity Indicators

Promoter Holding: Extremely stable at $52.90\%$ with zero promoter pledges. This highlights top-tier promoter backing and alignment of interests.

Management Tone: Highly transparent. During the earnings call, Managing Director Ajoy Chawla did not shy away from calling out the Q4 margin challenges, GCC disruptions, and the ₹82 Crore overseas loss. This candid nature builds deep institutional trust.

📝 The Advisory Note

1. Strategic Outlook (Long-Term Compounding Thesis)

Titan remains a multi-decade structural growth story. With only an $8\%$ market share in the highly unorganized Indian jewelry market, the runway for formalization remains vast. Tanishq's brand trust, CaratLane's millennial appeal, beYon's entry into Lab-Grown Diamonds (LGD), and Damas' international presence create a solid competitive moat. We advise long-term clients to stay invested.

2. Tactical Outlook (Short-Term Opportunistic Buying)

In the short term, volatile gold rates and margin drag from bullion sales could cap immediate upside. If macro headwinds trigger general market corrections, any decline in Titan’s stock price toward ₹3,200 should be treated as an excellent tactical accumulation opportunity.

⚠️ FairVlaue: https://docs.google.com/spreadsheets/d/e/2PACX-1vSxRsJmaxBA0ShBzS2UT-8Nrikm5cfFyyYmmH0yq4ptuvQeibUotxX8QYUo3Uru9-bOXJbyPj9F7kWA/pubhtml?gid=1002029211&single=true

⚠️ Regulatory Disclosure

This report is generated for educational and client advisory purposes.