HAL Q3 FY26 Analysis: Execution Momentum vs. Rising Employee Liabilities

As the domestic defense indigenization theme plays out, Hindustan Aeronautics Limited (HAL) remains the undisputed bellwether of India's aerospace architecture. For Q3 FY26, HAL delivered a set of numbers that firmly established its execution capabilities, even while navigating sharp, one-off statutory cost spikes.

Here is our elite desk’s comprehensive breakdown of HAL’s Q3 FY26 consolidated performance.

The Snapshot

The 'Wow' Factor

Profit Outpaces Topline: Consolidated Net Profit (PAT) skyrocketed by 29.7% YoY to ₹1,866.66 Cr, massively outpacing the 10.7% YoY growth in operational revenue.

Supreme Dividend Payout: The Board declared a staggering first interim dividend of ₹35 per share (700% on a face value of ₹5), signaling supreme confidence in forward free cash flows.

Order Book Bolstered: Post-Q3, HAL locked in massive operational momentum, signing two mega MoD contracts worth ₹5,213 Crore (₹2,312 Cr for 8 Dornier 228s and ₹2,901 Cr for 6 ALH Mk-III Helicopters) between February and March 2026.

Operational KPI Table

Financial Deep Dive: Quarter at a Glance

(All figures in ₹ Crores, based on Consolidated Financials)

Cost vs. Efficiency: A Test of Operational Leverage

Maintaining a Margin of Safety requires us to be highly critical of operating costs. During Q3 FY26, HAL faced a significant statutory headwind: the government raised the gratuity ceiling from ₹20 Lakhs to ₹25 Lakhs. This forced HAL to recognize a sudden additional employee liability of ₹331.93 Crore.

Despite this heavy blow to the operating expense line, HAL's core operational efficiency absorbed the impact effortlessly. Using the standard formula $EBITDA = Revenue - Operating\ Expenses$, HAL's EBITDA still grew by 11.2% YoY. Better product mix, higher other income (₹913.8 Cr vs ₹631.4 Cr), and excellent tax efficiency actively shielded the bottom line, resulting in an outsized ~30% jump in Net Profit. Management's tone remains highly transparent, accurately provisioning for legacy union and payload issues.

The Forward Curve

Based on management guidance and the heavy recent order flow, we project revenue to compound at 12-14% over the next two quarters. The newly inked ₹2,901 Cr ALH Mk-III (Maritime Role) contract specifically supports a massive network of 200+ MSMEs and guarantees ~65 lakh man-hours of employment, signaling hyper-active shop floors for H1 FY27.

Valuation Guardrails & Shareholding Patterns

Valuation Verdict: Trading at a Slight Premium

HAL currently trades at a P/E of ~27.7x, compared to its 5-year median P/E of 25.4x.

The P/B ratio sits at ~7.4x.

While the stock is undeniably trading at a historical premium, a 26%+ ROE and a zero-debt balance sheet warrant a higher multiple in an elevated defense capex cycle.

Smart Money Movement:

A critical shift has occurred in the shareholding pattern between March 2025 and December 2025:

Promoters: Unchanged at 71.64% (Zero pledged shares).

FIIs: Trimmed positions from 12.08% to 10.86%.

DIIs: Aggressively bought the float, raising their stake from 8.30% to 9.74%.

Public: Stable at ~7.76%.

Takeaway: The "Smart Money" baton is passing from Foreign Institutions to Domestic Institutions, signaling high domestic conviction in India's sovereign defense capital expenditure.

The Advisory Note

Strategic Outlook: HAL remains a strategic anchor for any defense-oriented portfolio. It holds near-monopoly status in India’s military aviation space with revenue visibility extending clearly into 2032.

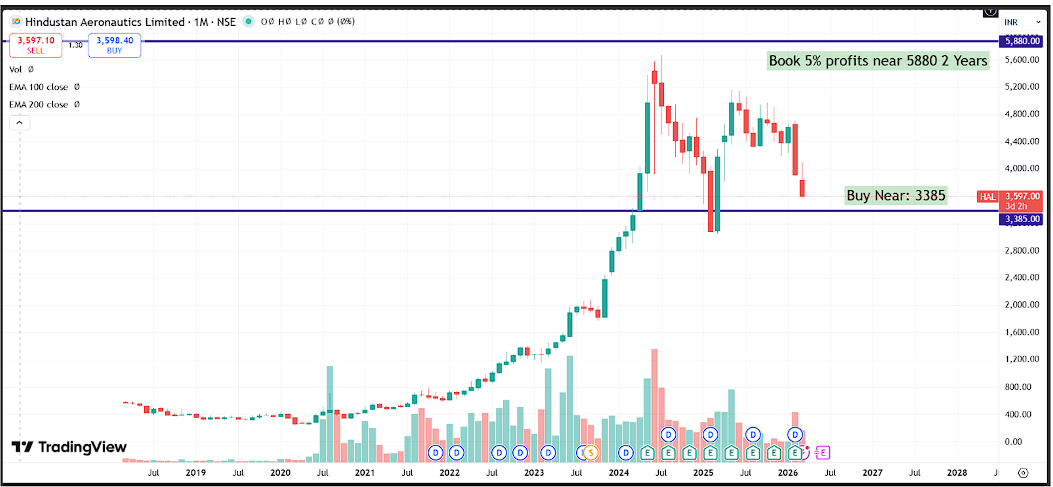

Tactical Action: The stock recently corrected Near to 10% amid sector-wide noise and unverified rumors regarding AMCA contract bidding. We view these transient corrections as high-probability entry points. Wait for minor technical dips to accumulate, adhering strictly to a staggered buying strategy.

Fairvalue:

Financial Disclosure: This report is for educational and informational purposes only and does not constitute direct financial advice.