ABB India Q4 CY2025 Analysis: Record Order Inflows vs. Margin Headwinds

By the Investment Advisory Team ProfitFromIt

The Snapshot

The 'Wow' Factor

Historic Order Book: ABB clocked its highest Q4 orders in five years, surging 52% YoY to ₹4,096 Cr, pushing the total order backlog to a massive ₹10,471 Cr.

Aggressive Capacity Expansion: The company announced a substantial ~$75 million investment for 2026 across five Indian locations to expand critical R&D and manufacturing capacity.

Unlocking Value: The management successfully executed a Business Transfer Agreement (BTA) to carve out and sell its Robotics Business to ABB Robotics India Pvt Ltd on a slump sale basis for a solid ₹1,568.20 Cr.

Data Center Tailwinds: Approximately 10-11% of the total backlog is now fueled by the hyper-scaling Data Center segment, placing ABB in the sweet spot of the AI and digitalization boom.

Operational KPI Table

Financial Deep Dive (Consolidated)

Note: EBITDA calculated as $PBT + Finance Costs + Depreciation \& Amortization$

Cost vs. Efficiency Analysis

Maintaining our Margin of Safety mindset, it is crucial to dissect why EBITDA and PAT contracted despite top-line growth. The drop is not a demand issue, but a cost-structure anomaly. Material costs spiked to $61\%$ of sales (up from $58\%$). Management made a conscious, strategic decision to use expensive imported materials from the EU to bypass domestic Quality Control Order (QCO) testing bottlenecks and ensure uninterrupted client delivery. Additionally, profitability was dampened by a ₹65.94 Cr one-time provision adapting to the new Labour Code. While top-line efficiency remains stellar, we remain slightly critical of this elevated cost base, which exposes the firm to forex volatility until the imported inventory flushes out over the next two quarters.

Management Integrity and Tone

During the earnings call, the management team, led by MD Sanjeev Sharma, projected a confident yet transparent tone. They were highly defensive and unapologetic about absorbing higher material costs, viewing it as a necessary trade-off to maintain customer trust and market share. Management was refreshingly upfront about the timeline of these margin pressures, guiding that the QCO-imported inventory will take another 1-2 quarters to clear.

Key Risks and Red Flags

Supply Chain Concentration: With ~20% of COGS reliant on EU imports, the company is vulnerable to geopolitical freight disruptions and unfavorable INR/EUR movements.

Margin Compression: The inability to pass on 100% of the input cost inflation immediately shows that pricing power, while strong, has limits in a stabilized demand environment compared to the post-COVID boom.

Peer Benchmarking

When stacked against its closest rival, Siemens Ltd, ABB commands a premium. Siemens currently trades at a P/E of ~66x, while ABB is trading near ~77.5x. However, ABB justifies this premium through a more aggressive localized expansion strategy (the $75M capex) and dominant exposure to high-growth pockets like hyper-scale Data Centers and the transition from IE2 to IE3/IE4 efficiency motors.

The Forward Curve

Looking ahead to Q1 and Q2 CY2026, we project the following trajectory based on management guidance:

Revenue: Expected to maintain a steady 8-10% YoY growth, supported by the execution of the massive ₹10,471 Cr backlog, particularly the large railway and data center orders.

Margins: EBITDA margins will likely remain range-bound between 15.0% - 15.5% in the first half of CY2026 as the expensive QCO-related inventory is consumed. Expect a stronger margin recovery in H2 CY2026.

Valuation Guardrails

Current P/E: ~77.5x

5-Year Median P/E: ~74.4x

Current P/B: ~16.5x

Verdict: Trading at a Premium. While the business fundamentals are exceptionally strong, the stock is currently trading slightly above its 5-year historical median. Much of the multi-year infrastructure growth thesis is already priced in at these levels.

Shareholding Pattern Dynamics

Recent shareholding data (Dec 2025 quarter) reveals intriguing institutional rotation:

Promoters: Rock solid at exactly 75.00% (No pledges).

FIIs: Foreign Institutional Investors took some profit off the table, reducing their stake from 8.29% to 7.64%.

DIIs & MFs: Domestic Mutual Funds absorbed a portion of this liquidity, expanding their footprint slightly from 4.04% to 4.18%.

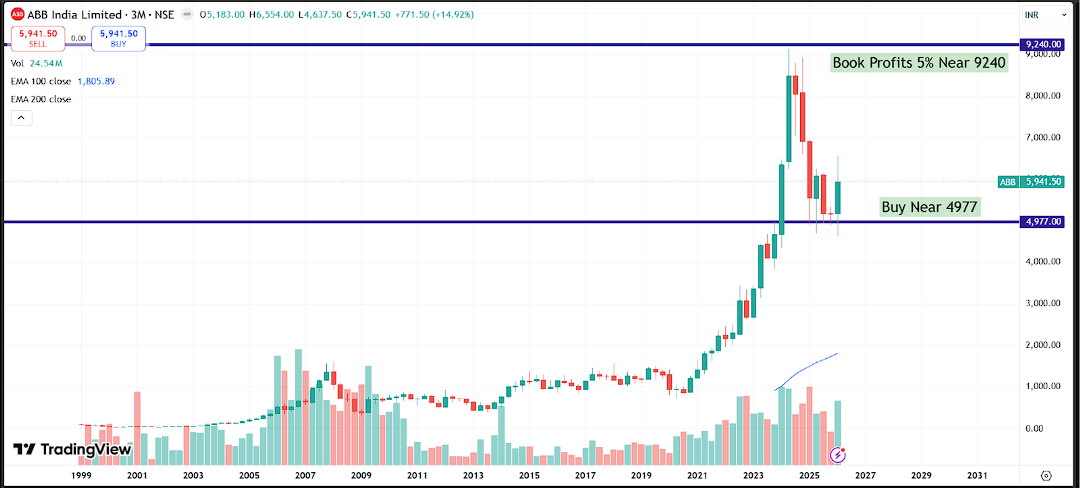

The Advisory Note

Strategic Outlook (Long-Term): The fundamental thesis is intact. With a shift towards automation, railway electrification, and AI-driven data centers, ABB's portfolio is flawlessly aligned with India's capex cycle. The ₹1,568 Cr slump sale of the Robotics division also indicates a sharp focus on capital efficiency.

Tactical Outlook (Short-Term): At ₹5,937, the valuation leaves little room for execution missteps. Investors looking to build fresh positions should ideally wait for the current margin friction to normalize over the next two quarters or look for broader market corrections to accumulate with a better margin of safety.

Disclaimer: This research piece is strictly for educational and informational purposes. It does not constitute direct financial advice.