LG Electronics India Q3 FY26 Analysis: Premium Momentum vs. High-Base Moderation

As the festive dust settles, LG Electronics India (LGEINDIA) has reported its Q3 FY26 numbers. While the company continues to dominate the premium appliances landscape, the quarter reflects a subtle moderation in bottom-line growth due to one-off labor code impacts and a high base effect from the previous year.

The Snapshot

The 'Wow' Factor

OLED Dominance: LG has maintained a staggering 62.4% market share in the OLED TV segment, gaining 2.6% YoY.

Washing Machine Moat: The company has created a massive 15.8% market share gap with its nearest competitor in the washing machine category.

Premium Up-tick: Side-by-Side (SBS) refrigerator market share improved by 2.9% to reach 43.3%.

Shareholder Confidence: FII holding has seen a marginal uptick of 0.25% post-listing, signaling global confidence in the India consumption story.

Operational KPI Table

Financial Deep Dive (Consolidated)

Cost vs. Efficiency:

The significant drop in PAT is primarily attributed to a one-time impact of INR 124.50 Million recognized towards the new Government Labor Code (gratuity and compensated absences). Additionally, higher marketing spends during the festive season and a general moderation in mass-market demand post-Diwali impacted margins. However, we remain impressed by the management's ability to keep other expenses in check, which rose only marginally despite inflationary pressures.

The Forward Curve

We project a high-single-digit revenue growth for the next two quarters (Q4 FY26 & Q1 FY27). The upcoming summer season is expected to drive strong demand for the Air Conditioning and Refrigerator segments. Management's guidance suggests a "Balanced Strategy" between volume in entry-level segments and value in the premium "Life's Good" ecosystem.

Valuation Guardrails

Management Integrity and Tone

Tone: Transparent & Strategic.

The management was forthright about the impact of the labor codes and the slowdown in the entry-level segment. They didn't shy away from discussing market share shifts, showcasing integrity. We perceive their tone as Confidently Defensive—protecting market share while aggressively pursuing premiumization.

Peer Benchmarking: LG vs. Samsung (India)

Key Risks and Red Flags

Labor Code Impact: The INR 12.45 Cr hit might be the first of many as state-level rules are finalized.

Commodity Volatility: Rising copper and aluminum prices could squeeze AC margins in the upcoming summer quarter.

Mass Market Fatigue: While premium is growing, the entry-level refrigerator and washing machine segments remain sluggish.

The Advisory Note

Strategic Outlook (Long-term): LGEINDIA remains a "Core Portfolio" candidate. Its dominance in the OLED and Premium Home Appliance segments provides a high barrier to entry. The transition from a product company to a "Smart Life Solution" company is a strong structural tailwind.

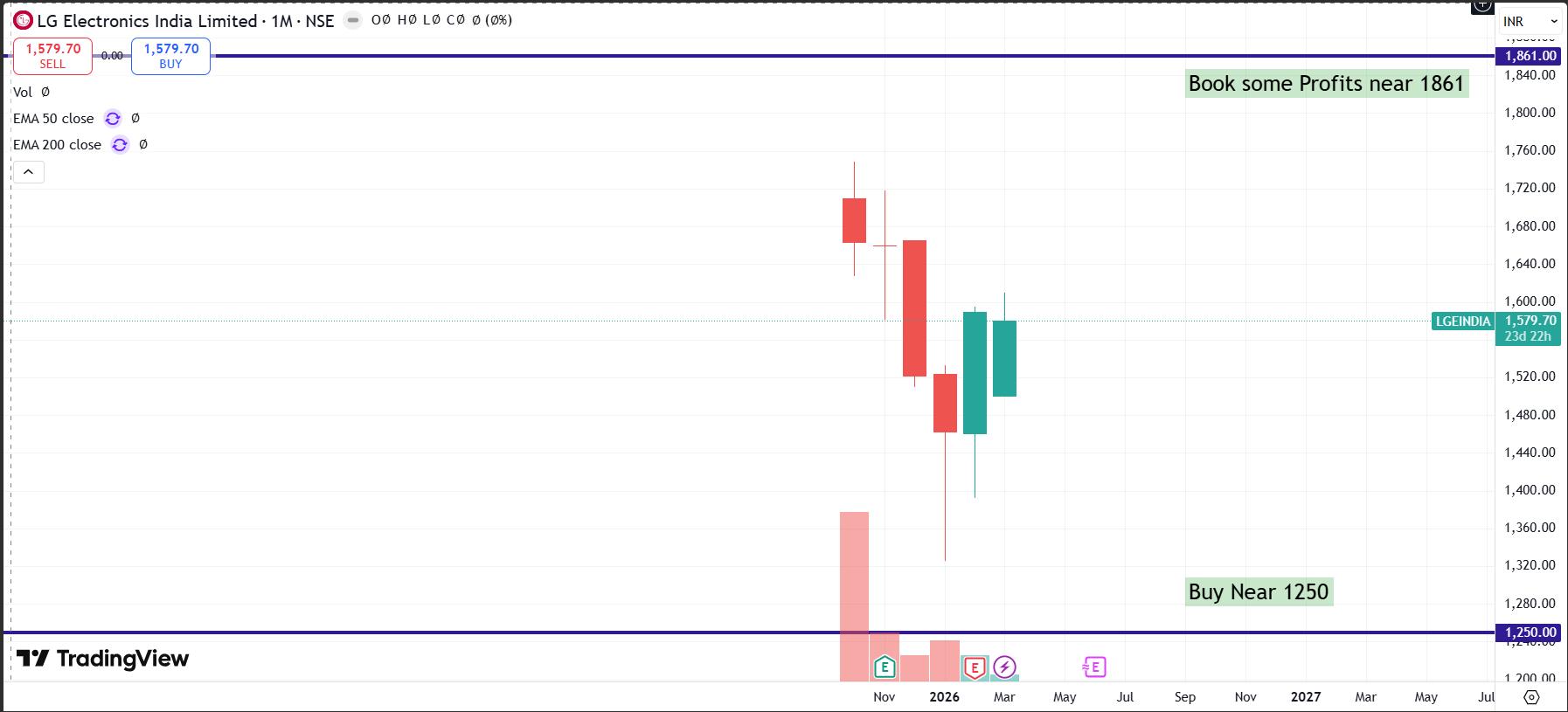

Tactical Outlook (Price Opportunity): At 1,596, the stock is pricing in a lot of future growth. A tactical entry is advised on dips towards the 1250 levels where the Margin of Safety is higher.

FAIRVALUE :

Financial Disclosure: We are SEBI registered investment advisors. This report is for educational purposes only.