🚧 Larsen & Toubro Q1 FY26 Results – Record Order Book, Global Growth, and Margin Watch Ahead

CMP: ₹3,642 | Result Date: 29 July 2025

1️⃣ Recent Insights & Strategic Highlights

From Management Commentary

✅ Record Order Book: ₹6.13 trillion – highest ever (+25% YoY).

✅ Robust Order Inflow: ₹945 bn (+33% YoY), driven by Infrastructure & CarbonLite Solutions; 46% from overseas.

✅ Strong Prospects Pipeline: ₹14.8 tn for remaining FY26 (+63% YoY), led by Hydrocarbon & Infra opportunities.

✅ Green Hydrogen Leadership: L&T GreenTech to build & operate a 10-KTPA plant for IOCL under a 25-year BOO contract.

✅ ESG Milestone: First Indian corporate to issue ESG bonds under SEBI’s framework; ₹5 bn raised at 6.35% coupon.

✅ L&T Finance Growth: Loan book crosses ₹1 tn; 98% retailization; secured international investment-grade ratings (BBB-).

⚠️ Margin Pressure: Hydrocarbon segment impacted by competitive legacy bids entering peak execution.

⚠️ Infra Softness: Higher costs & overruns in water projects affecting margins.

2️⃣ Consolidated Financial Performance

💡 Growth Drivers:

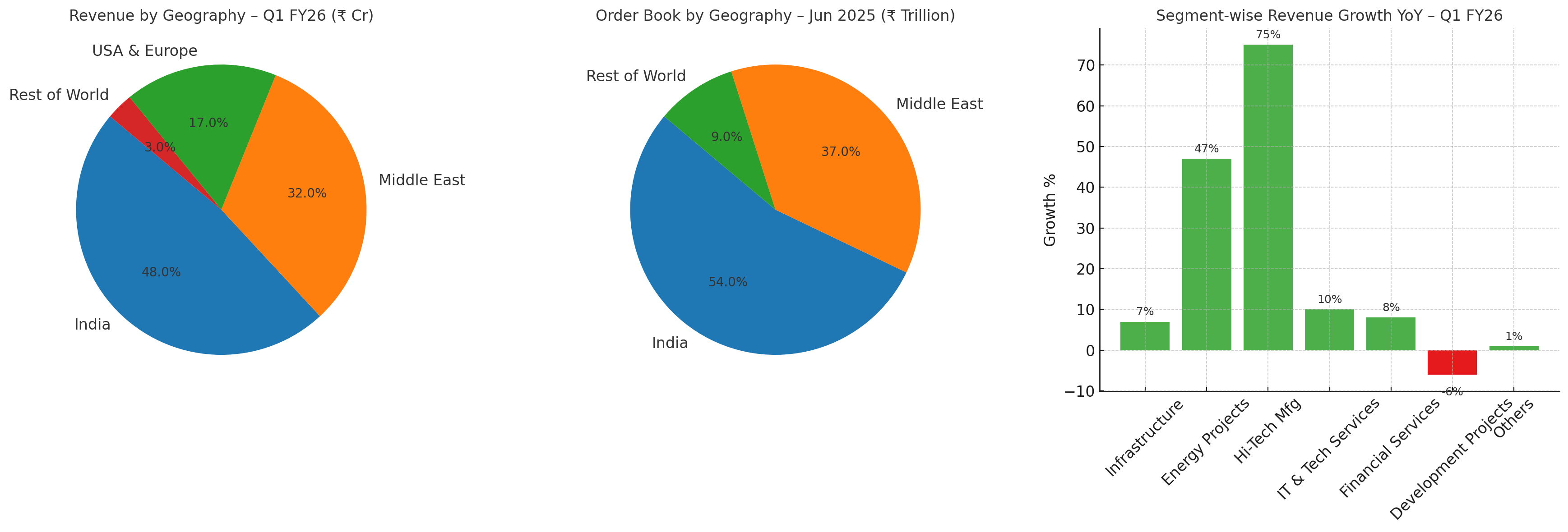

Strong execution in Hydrocarbon (+47% revenue) & Hi-Tech Manufacturing (+75%).

Higher other income (+47% YoY) and efficient treasury management boosted PAT.

3️⃣ Segmental Performance – Q1 FY26

📌 Key Observations:

Energy Projects and Hi-Tech Manufacturing are the biggest growth engines this quarter.

Infra margins remain slightly subdued due to cost overruns in water projects.

4️⃣ Geography-Wise Performance

🌏 Revenue Mix – Q1 FY26

India: ₹30,565 Cr (48%)

Middle East: ₹20,377 Cr (32%)

USA & Europe: ₹10,825 Cr (17%)

Rest of World (ROW): ₹1,912 Cr (3%)

💡 Takeaway: 52% of revenues are from overseas markets, led by Middle East projects in Hydrocarbon & Infra.

📦 Order Book – as of 30 June 2025

India: ₹3.31 tn (54%)

Middle East: ₹2.27 tn (37%)

ROW: ₹0.55 tn (9%)

💡 Takeaway: Balanced domestic-international mix, but Middle East forms 82% of international orders — concentration risk to monitor.

5️⃣ Order Flow & Pipeline

Q1 Order Inflows: ₹945 bn (+33% YoY) – Infra ₹410 bn, Energy ₹314 bn.

Order Book: ₹6.13 tn – well diversified across segments.

Prospect Pipeline: ₹14.8 tn for FY26 balance period, with Hydrocarbon prospects doubling YoY to ₹5.78 tn.

6️⃣ Profitability, Growth & Valuation Ratios

*Estimated from segment data

**TTM EPS ≈ ₹115

7️⃣ FY26 Estimates (Management + Trend-Based)

Sales Growth: ~20% for FY26.

Margins: P&M portfolio targeted at 8.3–8.5%; overall NPM ~6.8%.

Profit Growth: ~18% YoY driven by execution ramp-up & improved working capital.

8️⃣ Outlook

Near Term (Next 1–2 Quarters):

Sustained double-digit revenue growth from Energy & Infra.

Margins remain slightly pressured in Hydrocarbon until competitive bids conclude.

Long Term (FY27–FY30):

Strong alignment with India’s infra capex & global energy transition.

Growth in new-age areas — Green Energy, Semiconductors, Data Centers — will diversify revenue.

9️⃣ Conclusion for Long-Term Investors

Positives 👍

Record order book & strong project pipeline.

Consistent double-digit revenue & profit growth.

Diversified global presence.

Improved ROE, cash flows, and balance sheet position.

Risks ⚠️

Margin pressure from older competitive bids.

Geopolitical & oil price volatility in Middle East.

Execution risks in large, complex projects.

Investment View: Cautiously Optimistic – L&T remains a long-term compounding story, though investors should track margins and Middle East dependency.

Disclosure:

This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making investment decisions.