Indian Railway Finance Corporation (IRFC) Q4 & FY26 Analysis: High-Margin Diversification Gains vs. Flat Quarterly Profit Growth

The structural transformation of Indian Railway Finance Corporation (IRFC) has entered its most critical phase. Historically operating as the sole, captive financing arm of the Ministry of Railways ($MoR$), IRFC has embarked on a new era—IRFC 2.0—built on multi-client diversification.

As we dissect the Q4 and FY26 earnings, a clear operational theme emerges: improving structural interest spreads via high-margin non-railway assets is successfully under way, but it brings new provisioning realities that have temporarily flattened quarterly bottom-line growth.

For fund clients looking for yield stability and students seeking to understand sovereign-backed infrastructure finance, here is our institutional-grade deep dive.

1. The Snapshot

The following table summarizes the fundamental metrics of IRFC as of May 2026.

2. The 'Wow' Factor (Key Highlights)

Structural Spread Expansion: Diversified loan pipelines under "IRFC 2.0" yield margins of 100bps to 120bps, which are more than 2.5times to 3times the flat 35 - 40 bps margins traditionally earned on Ministry of Railways ($MoR$) assets.

Refinancing Transit Giants: Signed a landmark ₹13,527 Crore refinancing deal for the Hyderabad Metro Rail project (May 2026) and a ₹12,842 Crore deal for Hindustan Urvarak & Rasayan Limited (HURL), establishing itself as a dominant player in public-private partnerships ($PPP$).

Pristine Balance Sheet: Maintained an impeccable 0.0% Gross NPA ratio on a record-high Assets Under Management ($AUM$) of ₹4.85 Lakh Crore.

Dilution in Promoter Stake: Promoter shareholding was pared from 86.36% to 84.65% in Q4 FY26 to align with Minimum Public Shareholding ($MPS$) norms, triggering strong accumulation from domestic and foreign institutions.

3. Operational KPI Table

IRFC’s shift to a diversified, multi-client system is changing its operational profile, notably its Capital Adequacy Ratio ($CRAR$).

*Note: The drop in CRAR from historical highs is an expected outcome of the diversification strategy. Assets lent to non-sovereign entities (non-MoR CPSEs, State JVs) carry higher risk-weights compared to the zero-risk sovereign-backed lease agreements with MoR.

4. Financial Deep Dive

IRFC stands as a sole operating entity with no subsidiaries. The following standalone financials present the quarterly and full-year performance.

*EBITDA (Operating Profit) is computed as Total Income (including other income) minus Operating & Other Expenses (excluding finance costs/interest).

Cost vs. Efficiency Analysis

Our sequential profitability (QoQ) fell by $6.54\%$ in Q4 FY26, highlighting the structural trade-offs of the new business model. Unlike sovereign-backed $MoR$ lending, diversified loans to CPSEs and state-level projects fall under Ind AS 109, requiring mandatory provisioning. The rise of a large new loan pipeline led to higher provisioning, which, along with a seasonal spike in CSR expenses (₹45.51 Crore in Q4 vs ₹32.10 Crore in Q3), flatlined bottom-line growth.

Applying our Margin of Safety filter, we view this temporary friction as highly productive. IRFC is successfully converting ultra-low-yield captive assets into high-margin diversified assets, structurally strengthening its Net Interest Income ($NII$) over a multi-year horizon.

5. Peer Benchmarking

How does IRFC stack up against its principal PSU power-finance peers, PFC and REC?

The NIM-Risk Trade-off: PFC and REC enjoy much wider $NIMs$ of $3.0\% \text{ to } 3.5\%$, but they carry heavy exposures to debt-laden power distribution companies ($DisComs$) and private developers. IRFC's $NIM$ at $1.50\%$ is structurally safer and growing, backed by a flawless $0.0\%$ NPA track record.

The Valuation Gap: At CMP ₹95.7, IRFC trades at a considerable premium relative to its peers:

IRFC: Trailing $P/E$ of $17.85\text{x}$ | $P/B$ of $2.20\text{x}$

PFC: Trailing $P/E$ of $4.13\text{x}$ | $P/B$ of $1.38\text{x}$

REC: Trailing $P/E$ of $5.35\text{x}$ | $P/B$ of $1.05\text{x}$

While IRFC's sovereign status and zero-risk history command a premium, it narrows the short-term valuation Margin of Safety compared to REC and PFC.

6. The Forward Curve (Outlook & Projections)

Crossing the Milestone: We expect IRFC's total Assets Under Management ($AUM$) to comfortably breach the ₹5.00 Lakh Crore threshold in H1 FY27 (currently ₹4.85 Lakh Crore).

Double-Digit Guidance: Management is targeting double-digit expansion across top-line, bottom-line, $NIM$, and $EPS$ in FY27, driven entirely by non-MoR disbursements.

Margin Accretion: $NIM$ is projected to expand by over $10\%$ to land around $1.65\%$ by the end of FY27 as older, low-yield lease agreements with the railways naturally amortize and are replaced by higher-yield transit assets.

7. Valuation Guardrails

P/E Evaluation: With an $EPS$ of ₹5.36, the current $P/E$ stands at $17.85\text{x}$, which is above the 5-year historical median of $16.8\text{x}$.

P/B Evaluation: The current price-to-book ratio ($P/B$) stands at $2.20\text{x}$ compared to its historical median of $1.40\text{x}$.

Valuation Category: Trading at a Premium.

8. The Advisory Note

Strategic vs. Tactical Verdict

Strategic Long-Term Thesis (Buy on Dips): The structural pivot to "IRFC 2.0" is fundamentally positive. Moving beyond a single-client captive model expands IRFC's addressable market to ports, metro lines, and CPSE capex. This structural shift towards higher-margin assets will permanently expand $ROE$ and $ROA$ over the next five years.

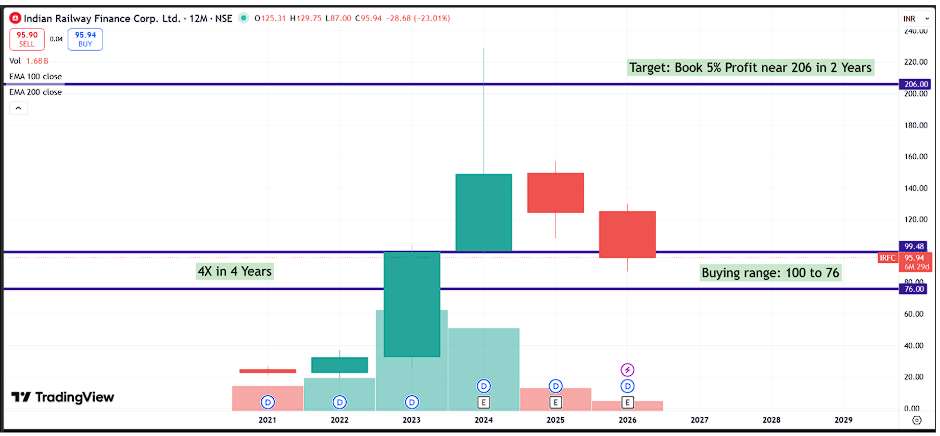

Tactical Short-Term Play (Hold/Book Profits): Because the stock trades at a premium to its 5-year averages, near-term upside is capped. Investors should hold current positions and wait for pullbacks to the ₹80-85 range to deploy fresh capital with an adequate Margin of Safety.

Fairvalue:

Mandatory Financial Disclosure

This report is generated for educational and informational purposes only. We are SEBI-registered investment advisors.