Reliance Industries Q3 FY26 Financial Analysis & Investment Insights

Reliance Industries Limited (RIL) continues to demonstrate its dominance across the energy-to-consumer spectrum. The Q3 FY26 results highlight a strategic shift toward high-growth, less cyclical consumer businesses, which now contribute nearly 60% of the group’s EBITDA.

1. Financial Growth Table: Q3 FY26 Performance

2. Sector-Specific KPIs & Manufacturing Insights

Retail & Consumer Goods:

Volume Growth: Digital commerce and merchant orders contributed 1.6 million orders daily at the end of the quarter.

EBITDA Margins: Impacted by a one-time charge from the new Labour Code and aggressive investments in hyper-local commerce.

Digital Services (Jio):

5G Leadership: Jio now holds a 65% share of all 5G subscribers in India.

Data Consumption: Total data traffic surged 34% YoY to 62.3 billion GB.

O2C (Refining & Petrochemicals):

Fuel Cracks: Transportation fuel cracks grew significantly (60%–100% YoY).

Operating Efficiency: Maintained high refinery utilization despite global supply chain disruptions.

3. Profitability & Valuation Suite

Profitability Metrics:

Operating Margin: Consolidated operating margin stood at 10.7% for the quarter.

ROCE Trends: Consistent cash flow generation is supporting a return to a high-capex cycle in New Energy.

Valuation Ratios:

Debt-to-Equity: Maintains a healthy 0.39x, down from 0.42x last year.

Net Debt/EBITDA: Strong deleveraging trend with a ratio of 0.57x.

Credit Rating: Upgraded to A- by S&P, making RIL the first Indian manufacturing company with such a high international rating.

4. Analyst Analysis & Concall Highlights

Beat/Miss vs. Estimates:

RIL delivered a beat on Revenue led by Jio and Retail, while PAT was in-line with estimates as higher interest and depreciation costs (due to 5G asset capitalization) offset operating gains.

Critical Concall Insights:

Quick Commerce Dominance: RIL is on track to become India’s 2nd largest Quick Commerce player, leveraging its 19,979 stores for 30-minute deliveries.

New Energy Commissioning: Integrated solar module and cell manufacturing lines have been successfully commissioned; Glass and Polysilicon plants are slated for later this year.

Al Strategy: The partnership with Google to provide Gemini Pro to 5G users is a key driver for customer premiumization and retention.

5. H1 FY26 vs. Q3 Trend Analysis

The user noted H1 FY26 revenue growth of 16% and profit margins of 4.4%.

Revenue Trend: While Q3 saw a slightly lower 10% YoY growth , the nine-month (9M) revenue growth remains robust at 8.6%.

Margin Trend: 9M PAT growth is an impressive 28.1% YoY. Excluding one-time investment gains, the underlying profit growth remains stable at 13%–14%, showing improved operational efficiency over H1.

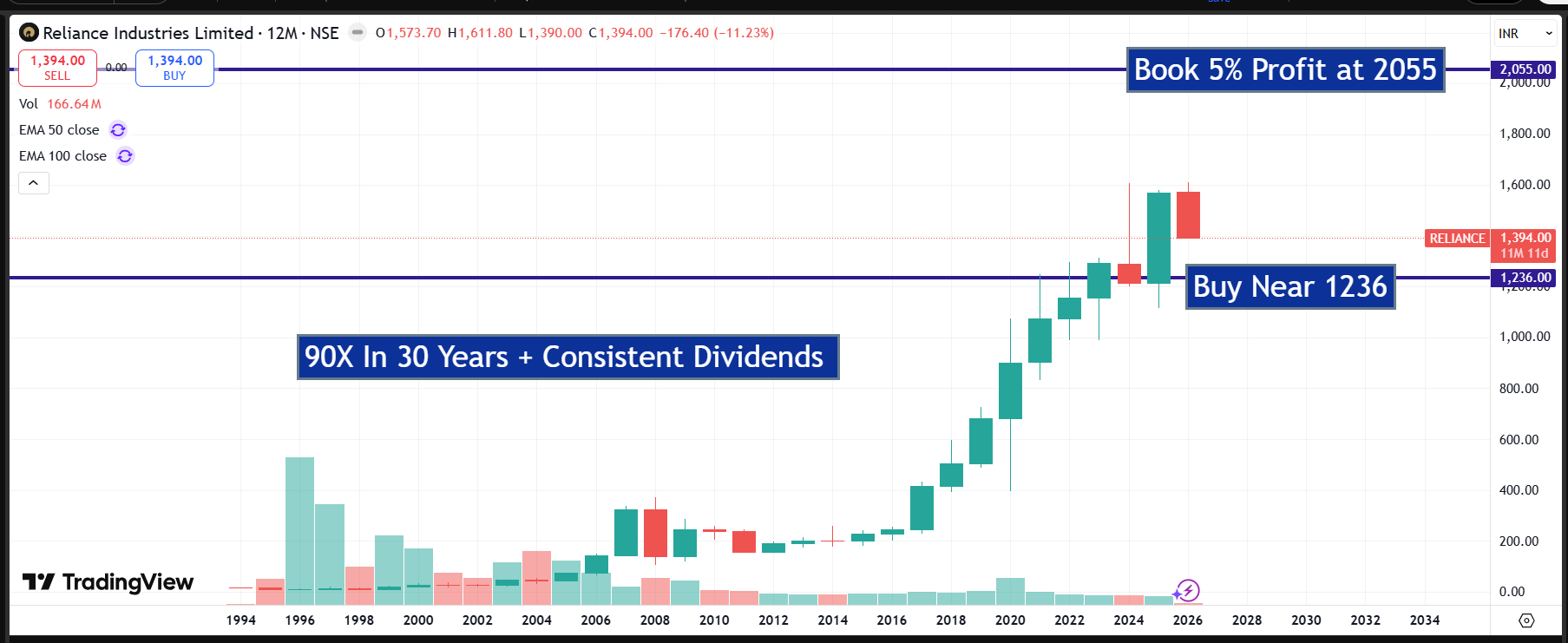

Conclusion: Wealth-Building Strategy

RIL is currently in Step 4 (Valuation) of our wealth-building strategy. The transition from a cyclical energy company to a consumer-tech giant is being rewarded with a credit rating upgrade. While the CMP of ₹1393 reflects current earnings, the massive value unlocking from New Energy and potential IPOs of Jio/Retail remains the long-term trigger.

Fair Value & Detailed Analysis: Available at

Disclosure: I am a SEBI Registered Investment Advisor. This report is for educational purposes and should not be considered a direct Buy/Sell recommendation. Please consult your financial advisor before investing.