Mazagon Dock Q4 FY26 Analysis: Order Execution Powerhouse vs. Depleting Order Backlog

At the firm, we have scrutinised the year-end performance of India’s premier defence shipbuilder. While the execution remains robust and the margin profile has structurally shifted upwards, the primary concern for any value-conscious investor remains the "Replacement Rate" of its order book.

The Snapshot

The 'Wow' Factor

Net Profit Surge: Consolidated PAT grew significantly YoY, driven by higher "other income" and efficient milestone billings in Project 15B and 17A.

Dividend Bonanza: The board has recommended a final dividend of ₹12.11 per share, taking the total dividend for FY26 to a significant payout ratio.

Zero Debt Status: MDL continues to operate as a net-debt-free entity with a massive cash pile of ~₹14,000+ Cr, generating substantial interest income.

Vessel Delivery: Successfully delivered the final vessel of a major series ahead of schedule, showcasing best-in-class operational efficiency.

Operational KPI Table (Shipbuilding Focus)

Financial Deep Dive (Consolidated)

Cost vs. Efficiency:

We observe a significant expansion in EBITDA margins. This is largely attributed to the "Tail-end of Projects" effect, where higher-margin milestone payments are recognised. However, as the major 15B and 17A projects reach completion, maintaining this margin profile without new billion-dollar contract wins will be a challenge. The efficiency in procurement and reduced sub-contracting costs has added ~150 bps to the bottom line this fiscal.

The Forward Curve

Based on management guidance and current execution timelines:

Q1 FY27 Guidance: Revenue growth is expected to remain flat or slightly positive (2-4%) as the yard transitions between major project phases.

Q2 FY27 Projection: We anticipate a "dry spell" in revenue recognition unless the much-anticipated P-75I (Submarines) or Next Gen Destroyers (NGD) contracts are signed by H1 FY27.

Valuation Guardrails

Current P/E: 28.5x

5-Year Median P/E: 14.2x

Verdict: Trading at a Premium. While the stock has re-rated due to the 'Make in India' tailwinds, it is currently trading at a ~100% premium to its historical median. Future upside is contingent on $5B+ order wins.

Shareholding Pattern & Pledges

Promoter Stake: Stable at 84.83% (Government of India).

FII/DII Trend: FIIs have marginally increased stake by 0.45% in the March quarter, signaling global confidence.

Pledge: Nil. The company has zero encumbrances on its shares.

The Advisory Note

Strategic Outlook (Long-term): MDL is a proxy play for India's naval dominance. With the Indigenization push, the long-term thesis remains intact. We recommend holding for the "Submarine Cycle" which is expected to kick off in late 2026.

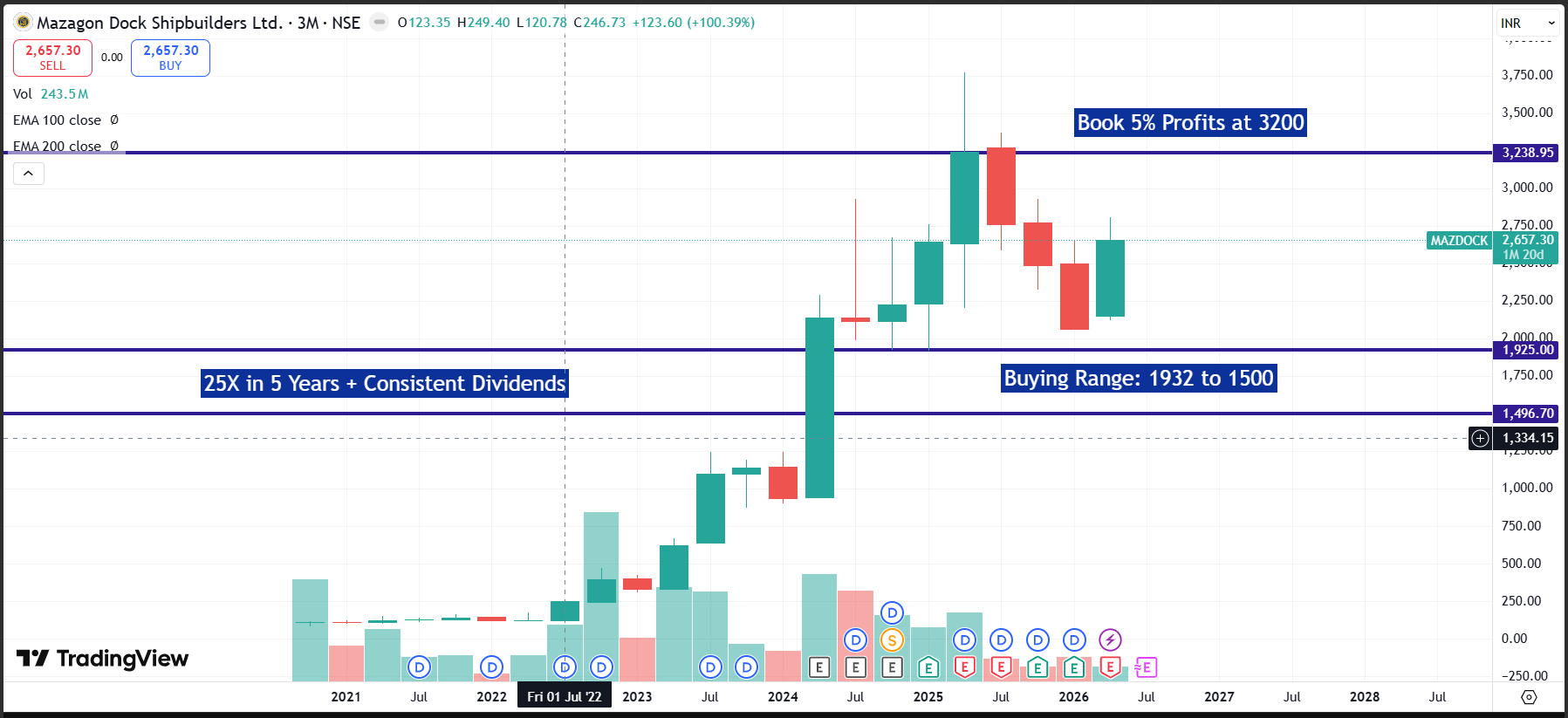

Tactical Outlook (Short-term): At ₹2,645, the stock is priced for perfection. Any delay in the ₹60,000 Cr P-75I contract could lead to a 10-15% price correction. Tactical entry is advised near the ₹1900 support zone.

Mandatory Disclosure: We are SEBI-registered analysts. This report is for educational purposes only.