HDFC Life: Driving Protection Momentum in Q3 FY26

HDFC Life is a leading private life insurer in India, known for its diverse product mix and robust multi-channel distribution. The company focuses on balancing long-term profitability with prudent risk management.

1. Financial Growth Table: 9M & Q3 FY26 Analysis

The following table provides a comprehensive overview of the financial trajectory for the period ended December 31, 2025.

*Individual APE estimated based on 9M data and YTD growth rates.

2. Sector-Specific KPIs (Insurance/NBFC)

VNB & Margins: Value of New Business (VNB) for 9M FY26 grew 7% YoY to ₹2,773 Cr. Normalised VNB growth (excluding GST/SSV impacts) stood at 13%.

New Business Margin (NBM): The 9M margin was 24.4% compared to 25.1% in the previous year. The contraction was primarily due to the GST impact on the protection segment.

Persistency: 13th-month persistency stood at 85%, and 61st-month persistency at 63%.

AUM: Assets Under Management grew 15% YoY to reach ₹5.3 trillion (including pension funds).

3. Profitability & Valuation Suite

Profitability:

Return on Equity (ROE): 11.6% for 9M FY26.

Operating ROEV: Healthy at 15.6% on a rolling 12-month basis.

Valuation:

Current PE: ~83.5x (TTM) vs. a 5-year average of ~94.9x.

Price to Book (P/B): ~9.9x.

Debt-to-Equity: 0.18x (Standalone) as of Dec 2025.

Section 2: Performance Summary & Concall Insights

Performance vs. Estimates: "Miss" on PAT and Margins. Net profit missed analyst estimates by approximately 2.4%, and VNB margins contracted by 70-110 bps due to the loss of Input Tax Credit (ITC) post-GST rationalization.

Critical Concall Insights:

Protection Powerhouse: Retail protection registered a massive 70% growth in Q3 FY26, driven by the GST exemption on premiums, which acted as a demand catalyst.

Product Innovation: The launch of Click 2 Protect Supreme and higher sum assured policies in the ULIP segment helped offset margin pressure.

Regulatory Resilience: While new surrender value regulations and GST changes initially impacted growth, the company expects momentum to sustain into Q4 FY26.

Section 3: Future Outlook & Peer Comparison

Future Growth (FY26-27):

Analysts project an APE growth of 13% for FY26 and 14% for FY27, driven by a recovery in Non-Par products and sustained retail protection demand. Margins are expected to stabilize around 24.5%–25% as the high-margin protection mix increases.

Peer Comparison:

HDFC Life maintains the #2 rank in the private sector for Individual WRP. While SBI Life (PE ~84.5x) and ICICI Pru (PE ~70.3x) offer competition, HDFC Life’s strong bancassurance (59% of Individual APE) and product innovation provide a competitive moat.

Section 4: Profitability and Margin Trends

Based on H1 FY26 data (16% revenue growth and 4.4% profit margin), the 9M FY26 data shows a stabilization in performance. Total premium growth of 13% for 9M indicates a slight softening from H1, while PAT growth (normalized at 15%) shows that underlying operational efficiency is improving despite regulatory headwinds.

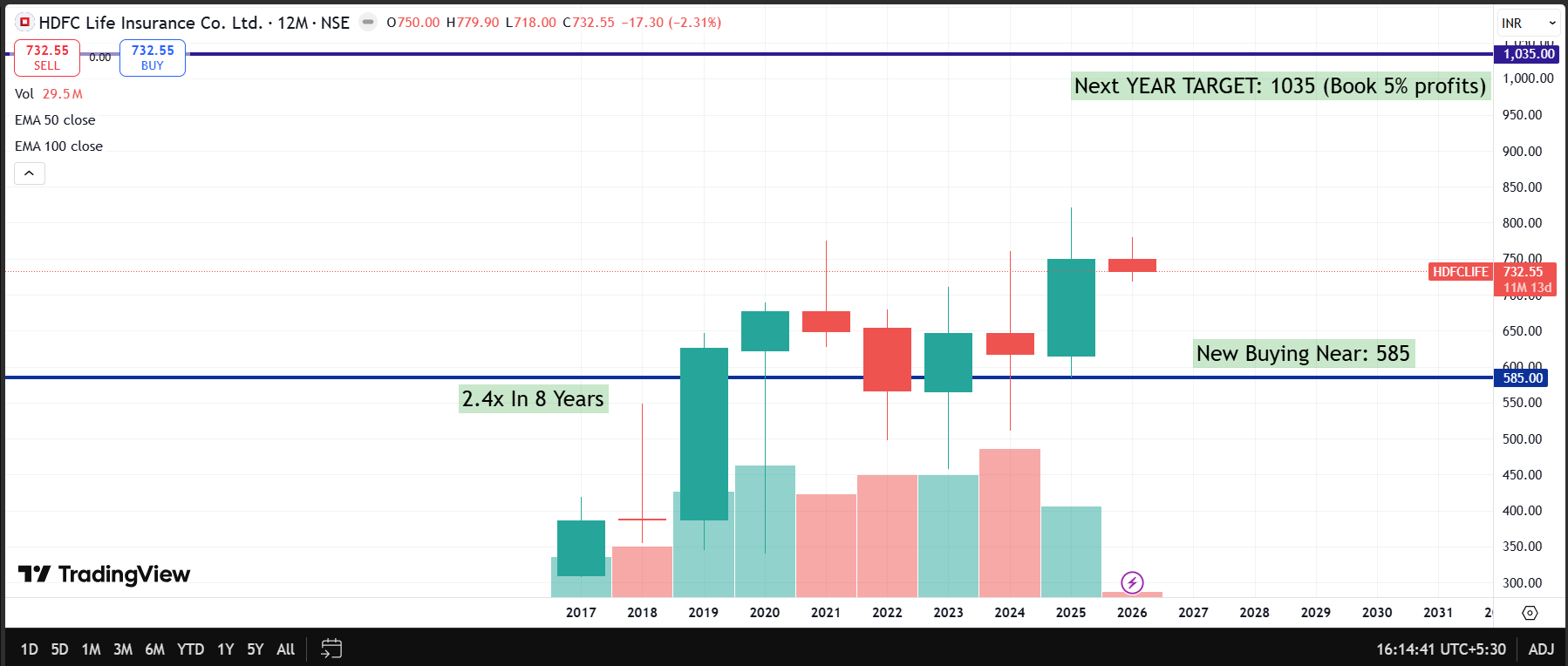

Conclusion: Wealth-Building Strategy

HDFC Life remains a core "Compounder" in the insurance sector. In our '5 Steps Towards Wealth' framework, this analysis pertains to Step 4: Valuation. Although the stock trades at a premium, its consistent Embedded Value (EV) growth of 16% YoY makes it a high-quality portfolio candidate for long-term investors.

Fair Value Disclosure: Detailed Fair Value calculations for HDFCLife are available at https://docs.google.com/spreadsheets/d/e/2PACX-1vTJnHHlGEYqHnvzQYcEl8lNys-JCYjbTGTEh7U4hvGG7Fpuh2AL83rKxYFO9oemvw/pubhtml?gid=1929646466&single=true

Disclosure as an Investment Advisor: This report is for educational and analytical purposes only. Profitfromit is a SEBI-registered Investment Advisor. Our Fund holds a personal position in the stock discussed.