Waaree Energies Ltd Q1 FY26 Results Analysis

CMP: ₹3,089

Date: July 28, 2025

1. Recent Insights and Highlights 📈⚡

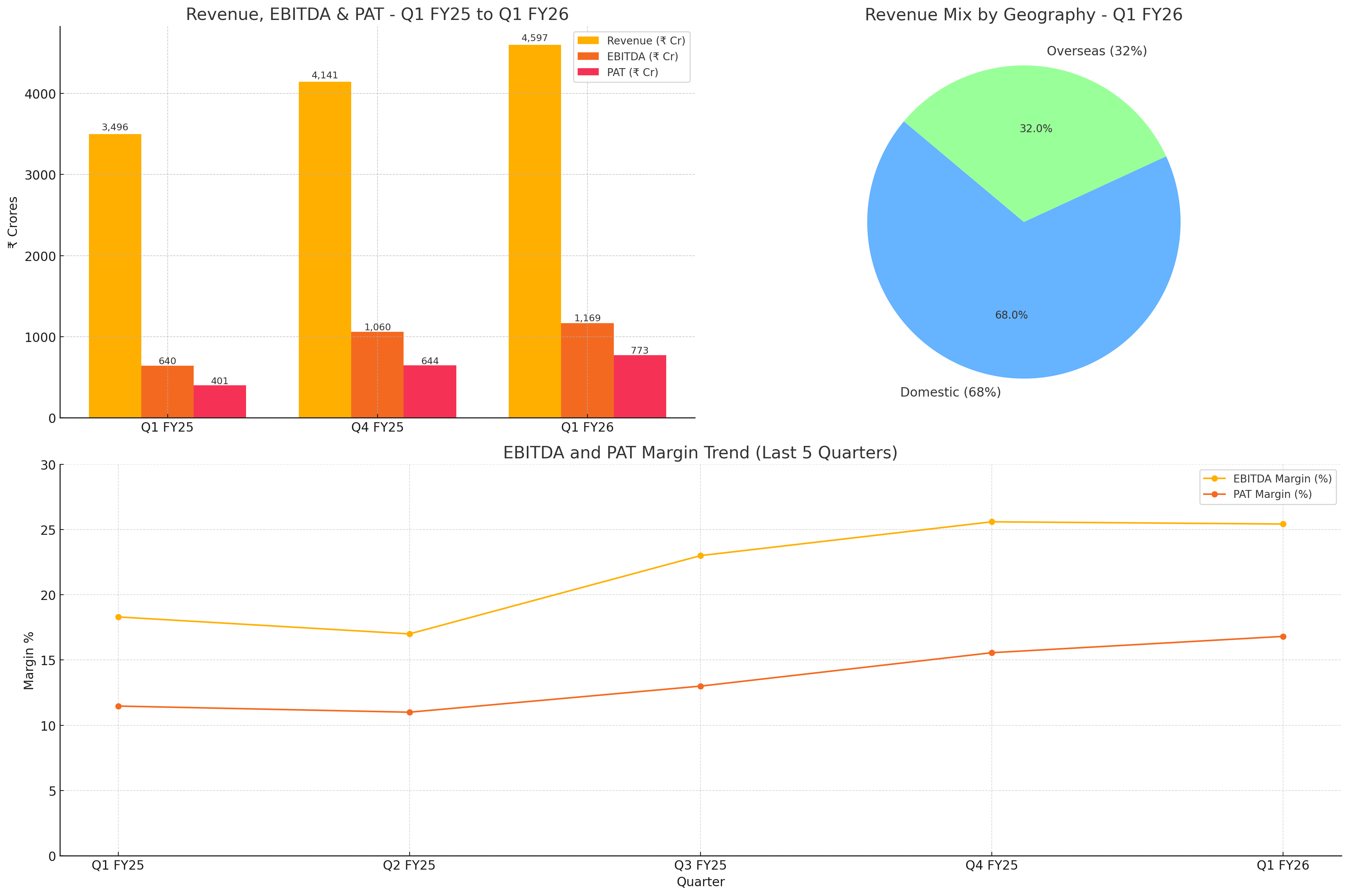

Robust Revenue Growth: Waaree reported consolidated revenue of ₹4,597.18 crore for Q1 FY26, marking a strong 31.5% YoY increase and an 11% QoQ rise.

Profitability Surge: EBITDA surged 82.6% YoY to ₹1,168.67 crore, with EBITDA margins expanding to 25.42% from 18.3% a year ago.

Net Profit Doubled: PAT almost doubled, rising 92.7% YoY to ₹772.89 crore, with net margin improving to 16.81%.

Record Production: Highest-ever quarterly solar module production of 2.3 GW achieved, with cell production ramping up as planned.

Strong Order Book: Order book stands at ₹49,000 crore (~25 GW) with a robust global pipeline exceeding 100 GW.

Capex and Expansion: Board approved ₹2,754 crore capex for new 4 GW cell capacity in Gujarat and 4 GW ingot-wafer plant in Maharashtra, targeting operational readiness by FY27.

Green Hydrogen & Energy Storage: Facilities under construction, indicating a move toward diversified renewable energy solutions.

Manufacturing Shift: Shareholders' approval sought to shift manufacturing locations from Odisha to Gujarat and Maharashtra for efficiency.

2. Consolidated Financial Analysis 📊

Segment & Regional Performance

Domestic Revenue: 68% of total revenue, showing steady growth aligned with Indian solar capacity expansion.

International Revenue: 32%, driven by US and other global demand, including order inflow of ~2.23 GW from Waaree Solar Americas Inc.

3. Profitability, Growth & Valuation Ratios 📈

*FY25 ROE and ROCE from latest annual report, expected to improve with Q1 results.

4. Industry-Specific KPIs and Growth Trends 🌞

Industry outlook remains strong due to supportive government policies (PLI, DCR, ALMM), growing global demand, and advancing solar technology.

5. Near-Term and Long-Term Outlook 🔮

Near Term (1-2 Quarters):

Continued ramp-up of cell and module production.

Commissioning of additional manufacturing capacity in Texas (USA) and Gujarat on track.

Strong order inflows expected to sustain revenue growth.

Close monitoring of US tariff and anti-dumping investigations impacting exports.

Long Term (FY26-FY35):

Capacity planned to more than double by FY27 to 25.7 GW.

Diversification into green hydrogen, battery storage, and inverter manufacturing to capture growing renewable energy segments.

Expected industry growth of 2x–2.5x by FY30 supported by government initiatives and global energy transition.

Strategic acquisition of Enel Green Power India projects pending closure will strengthen renewable project portfolio.

6. Conclusion for Long-Term Investors 💡

Key Positives

✅ Exceptional revenue and profit growth with improving margins

✅ Strong execution track record with record production

✅ Large and healthy order book provides revenue visibility

✅ Strategic capacity expansion aligned with global solar demand

✅ Diversification into emerging green energy technologies

Potential Risks

⚠️ Delays or regulatory risks related to manufacturing relocation and acquisitions

⚠️ Exposure to US trade policies and anti-dumping measures

⚠️ Execution risks in large-scale capex projects

Investment Stance

Cautiously Optimistic / Strong Buy for investors seeking exposure to India’s leading solar manufacturer with visible growth and improving profitability. Monitoring of geopolitical trade risks and project execution progress is advised.

7. Disclaimer ⚠️

This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making inves