Wonderla Holidays Q4 FY26 Analysis: Premiumisation and Chennai Expansion vs. Climate Risks and Labor Codes

By the Profit from It Research Desk

Date: May 20, 2026

In the highly capital-intensive amusement park sector, true competitive moats are built on operational excellence, geographic expansion, and relentless cost discipline. For Q4 FY26, Wonderla Holidays Ltd. delivered a blockbuster quarter, heavily driven by the operationalization of its Chennai park and a sharp focus on premiumisation.

However, as value investors adhering to a strict "Margin of Safety" mindset, we must look beyond the headline growth. Below is our comprehensive analysis of Wonderla’s Q4 FY26 financial health, management tone, and valuation metrics.

📊 The Snapshot

🚀 The 'Wow' Factor

Highest-Ever Q4 Topline: Consolidated Total Income surged to ₹142.05 Cr, representing a stellar 32% YoY growth.

Massive Operating Leverage: EBITDA for the quarter catapulted by 64% YoY to ₹50.01 Cr, proving the scalability of their fixed-asset model once break-even footfalls are achieved.

Chennai Park Scaling Fast: Launched on December 2, 2025, the Chennai park was a massive catalyst, pushing Q4 footfalls up by 30% YoY to 8.79 lakhs.

Resorts Breakout: The integrated hospitality model is finally paying off, with the resorts business delivering an explosive 84% YoY growth in Q4.

⚙️ Operational KPI Table

In the amusement park industry, the true leading indicators are Footfalls and Average Revenue Per User (ARPU).

🔬 Financial Deep Dive

Note: Consolidated figures in ₹ Crores.

Cost vs. Efficiency Analysis:

Wonderla showcased exceptional operating leverage this quarter. We calculate the EBITDA margin using the formula:

$$EBITDA \ Margin = \left( \frac{EBITDA}{Total \ Revenue} \right) \times 100$$

The Q4 FY26 EBITDA margins expanded drastically to 35.2%, up from ~28.3% in Q4 FY25. Management’s strategy to integrate resorts (like The ISLE at Bengaluru) is driving higher margin, non-ticketing revenue.

However, we are keeping a critical eye on regulatory compliance costs. The company had to absorb a net impact from the new Labour Codes, adjusting ₹2.81 Cr for past service gratuity and ₹1.59 Cr for compensated absences (though some reversals were recognized in Q4). As new parks scale, fixed overheads and employee benefit expenses will require stringent monitoring.

🎙️ Management Integrity and Tone

Tone: Highly Confident but Adaptable.

Executive Chairman and MD Arun Chittilappilly maintained a highly optimistic tone, emphasizing the success of the Chennai park launch and a strategic pivot towards "premiumisation" (enhancing ARPU without drastically hiking base ticket prices).

Transparency Check: When questioned during the earnings call about the severe heatwaves impacting daytime footfalls, management was transparent and defensive in a pragmatic way. They did not dodge the question; instead, they highlighted their operational pivot to "Night Parks" to adapt to climate realities, proving agility in capital utilization.

⚔️ Peer Benchmarking

When benchmarked against its closest listed peer, Imagicaaworld Entertainment, Wonderla remains the undisputed king of capital allocation in this space. While Imagicaa has historically struggled with immense debt burdens leading to equity dilution and restructuring, Wonderla operates with virtually zero debt ($Debt/Equity = 0.00$). Wonderla’s consistent generation of free cash flow funds its CapEx entirely through internal accruals and QIPs, completely avoiding the interest-cost trap that crippled its peers.

🚩 Key Risks and Red Flags

Climate & Weather Dependency: The management openly acknowledged the impact of severe heatwaves. While "Night Parks" are a great mitigation strategy, extended extreme weather will naturally cap daytime asset utilization.

Labor Code Uncertainties: The continuous reassessment of gratuity and compensated absences under new labor codes indicates that employee costs may see unpredictable spikes in the coming fiscal year.

Capital Intensity Execution: While Chennai launched successfully, maintaining ROIC (Return on Invested Capital) as the asset base expands will be management's toughest test.

📈 The Forward Curve

Looking ahead to Q1 and Q2 FY27, we project a 15% to 18% Topline CAGR. Q1 is historically the strongest quarter due to school summer holidays. We expect the Chennai park to hit peak utilization during this period, supplemented by the new ISLE resort in Bengaluru. If the heatwave mitigation strategies hold up, Q1 FY27 could set a new historical high for the company.

⚖️ Valuation Guardrails & Shareholding

Current P/E: 36.76x

5-Year Median P/E: 16.26x to 17.91x

Price-to-Book (P/B): 1.67x

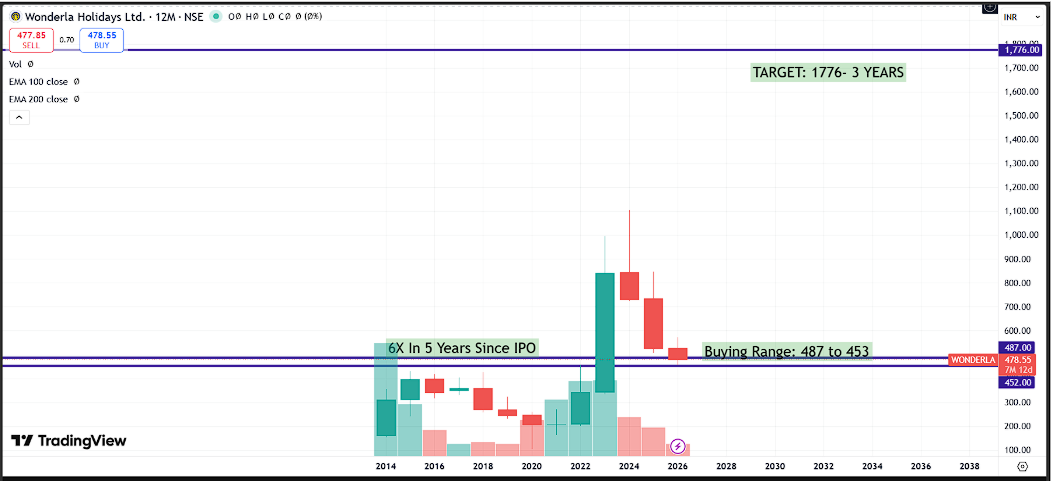

Valuation Verdict: Trading at a Premium. At nearly 37x trailing earnings, the market has already priced in the success of the Chennai park and the post-pandemic revenge travel tailwind. Based on historical multiples, the stock is trading at more than double its 5-year median P/E.

Shareholding Action:

Promoters: Rock solid at 62.25% with zero pledged shares—a massive green flag.

DIIs/Mutual Funds: Showing conviction, having increased their stake from 10.12% to 10.39% recently.

FIIs: Slight tactical trimming from 5.49% to 5.24%.

📝 The Advisory Note

Strategic Outlook (Long-Term): Wonderla is a compounding machine with an unbreachable moat. Replicating their land bank, brand equity, and safety record is near-impossible for new entrants. They are a structural "BUY" on a 5-year horizon.

Tactical Outlook (Short-Term): The current CMP of ₹478 prices in perfection. A broader market correction or a monsoon-heavy Q2 could provide a better entry point closer to the ₹400-₹420 range, offering the requisite margin of safety.

Financial Disclosure: This report is for educational and informational purposes only. The Profitfromit Research Desk and its analysts & our fund do hold direct positions in the stock mentioned.