UltraTech Cement Q4 FY26 Analysis: Historic 200 MTPA Milestone vs. Geopolitical Cost Headwinds

As the flagship cement player of the Aditya Birla Group, UltraTech Cement has delivered a historic Q4 FY26, brushing aside regional demand constraints and volatile geopolitical crosswinds. With capacity crossing the psychological 200 MTPA threshold and the highest-ever quarterly EBITDA recorded, the print reflects structural operational leverage. However, as disciplined analysts, we must weigh this stellar compounding story against current valuation multiples and emerging cost pressures.

Here is our elite breakdown of UltraTech's Q4 FY26 performance.

The Snapshot

The 'Wow' Factor

The 200 MTPA Frontier: UltraTech officially crossed 200.1 MTPA in domestic grey cement capacity (205.5 MTPA globally), entrenching itself as the largest cement producer globally outside of China.

Historic Operating Cash Flows: FY26 operating cash flow surged $50\%$ YoY to ₹14,398 Crores, adequately funding the massive ₹10,000 Crore forward CapEx without stressing the balance sheet.

Mega Special Dividend: The board announced a colossal $2400\%$ special dividend (₹240/share), signaling supreme management confidence and rewarding long-term capital providers.

Green Power Ascendancy: Green power mix jumped to an impressive $43\%$ (up from $34.4\%$ last year), acting as a formidable structural hedge against imported fossil-fuel volatility.

Operational KPI Dashboard

(Note: Prior year comparables adjusted for context based on growth percentages provided in the presentation).

Financial Deep Dive (Consolidated)

Cost vs. Efficiency Analysis:

UltraTech's ability to defend margins in Q4 FY26 is a masterclass in cost optimization. Total costs per tonne declined $2\%$ YoY. Despite the ongoing West Asia conflict exerting pressure on global supply chains, fuel costs surprisingly contracted by $1\%$ YoY to $₹874/\text{t}$, heavily aided by reducing clinker conversion ratios ($1.48\text{x}$) and an aggressive push into Alternative Fuels and Raw materials (AFR mix at $7.2\%$). Logistics costs saw a slight $2\%$ YoY uptick ($₹1,154/\text{t}$) due to packaging and ocean freight, but this was comfortably absorbed by the operating leverage generated from an $89\%$ capacity utilization rate.

Shareholding Dynamics & Red Flags

Institutional Shifts:

Recent shareholding patterns indicate a slight rotation. Promoters maintain a rock-solid grip at $59.33\%$. However, we noted a slight reduction in FII exposure (dropping to $13.61\%$), which was readily absorbed by Mutual Funds and DIIs (increasing to $15.24\%$). There are no alarming promoter pledges to report.

Key Risks and Red Flags (Earnings Call & PR Observations):

Geopolitical Fuel Vulnerability: Management transparently flagged that a $\$10$ cost increase in imported coal/petcoke directly hits EBITDA by $₹60-70/\text{t}$. Any severe escalation in West Asia remains a potent risk.

Regional Demand Pockets: Infrastructure demand was notably sluggish in the North (due to GRAP IV constraints and adverse weather) and the East (fiscal issues). Rural housing continues to carry the weight.

Pricing Stagnation: Grey cement domestic realizations were virtually flat YoY ($₹5,034/\text{t}$). Growth is entirely volume-led. In a high-inflation scenario, the inability to hike cement bag prices could compress margins.

The Forward Curve

Looking ahead to H1 FY27, we project robust volume growth driven by the commissioning of an additional $15.9 \text{ MTPA}$ of capacity across diverse geographies (including Visakhapatnam, Shahjahanpur, and Patratu). Furthermore, the upcoming launch of their Cables and Wires business by Q3 FY27 will mark a pivotal transition from a pure-play cement manufacturer to a holistic B2B/B2C building materials conglomerate. Expect EBITDA margins to stabilize in the $20\%-22\%$ range as green power scales toward their $85\%$ target by FY30.

Valuation Guardrails

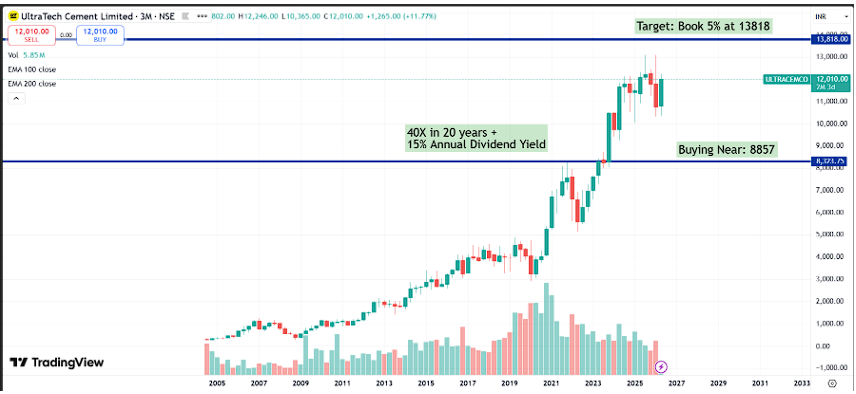

Current Metrics: At a CMP of $₹12,013$, UltraTech trades at a trailing P/E of roughly $43.3\text{x}$ (based on FY26 Diluted EPS of $₹277.45$).

Historical Benchmarking: The 5-year median P/E sits near $37.5\text{x}$.

Verdict: Trading at a Premium. The market is generously pricing in the successful India Cements integration, the 200 MTPA milestone, and peak operating efficiencies. While the premium is justified by its undisputed market leadership and fortress balance sheet (Net Debt/EBITDA at just $0.94\text{x}$), the margin of safety for lump-sum deployment at current levels is narrow.

The Advisory Note

Strategic Outlook: For long-term core portfolios, UltraTech remains an indispensable proxy for India's infrastructure and housing super-cycle. Its unmatched scale and ruthless cost discipline make it a "buy on dips" compounder.

Tactical Action: Investors holding the stock should maintain their positions to harvest the ₹240 special dividend and long-term capital appreciation. Fresh allocations should be staggered systematically (SIP mode) to navigate potential short-term volatility stemming from premium valuations and global energy price fluctuations.

Disclaimer: This analysis is for educational and informational purposes only. It does not constitute personalized financial advice. We maintain a 'Margin of Safety' approach to all capital market evaluations.