Dr. Lal PathLabs Q4 FY26 Analysis: Volume-Led Growth vs. Rising Competitive Intensity

As the diagnostic sector in India undergoes rapid consolidation and digital transformation, Dr. Lal PathLabs (DLPL) continues to demonstrate why it remains a benchmark for operational efficiency. In the fourth quarter of FY26, we observed a resilient performance characterized by double-digit volume growth, though margins faced pressure from aggressive expansion and competitive pricing.

The Snapshot

The 'Wow' Factor

Robust Top-line Growth: Revenue surged to ₹703 Cr in Q4 FY26, showcasing strong market penetration despite intense competition.

Volume Surge: Processed over 94.5 million samples in FY26, reflecting a robust organic growth engine.

Network Expansion: Added significantly to the reach, ending the year with 312 clinical labs and 7,727 Patient Service Centers (PSCs).

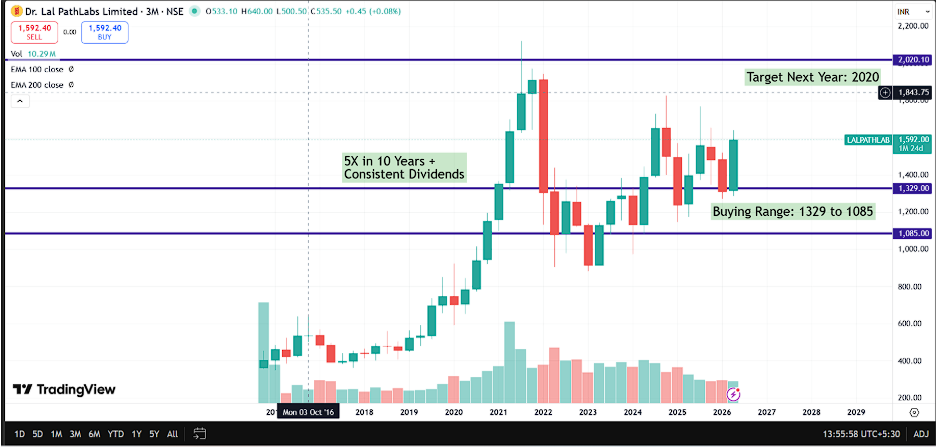

Dividend Payout: The Board recommended a final dividend of ₹4 per share, maintaining its track record of returning value to shareholders.

Operational KPI Table

Financial Deep Dive (Consolidated)

Cost vs. Efficiency:

While the company achieved a strong 16.6% YoY revenue growth, the operational profitability (EBITDA) grew at a slower pace of 6.2%, indicating margin contraction from 28% to roughly 25.5%. The bottom line faced even steeper headwinds, with PAT declining by 15.4% YoY. This decoupling suggests a sharp spike in non-operating costs or high depreciation/interest from new Regional Reference Labs, alongside aggressive marketing spends to protect market share against digital disruptors. The "Margin of Safety" is currently under test as the company prioritizes volume and infrastructure over immediate profitability.

The Forward Curve

Based on management guidance and the current run-rate of PSC additions, we project:

Q1 FY27: Expected Revenue growth of driven by seasonal wellness packages and higher test intensity.

Q2 FY27: Focus will shift toward margin recovery; EBITDA margins expected to stabilize as new labs reach optimal capacity utilization.

Valuation Guardrails

Current PE: 38.5x

5-Year Median PE: 48.2x

Verdict: Historically Discounted. Despite the current profit squeeze, the stock is trading at a significant discount to its long-term average. The market appears to be pricing in the temporary margin pressure.

Shareholding & Pledge Status

Promoter Holding: Stable at 54.1%.

Pledge: Zero Pledge (A major sign of financial health).

FII/DII Trend: Slight increase in DII stake (Mutual Funds) by 0.4% during the quarter, indicating domestic institutional confidence in the recovery thesis.

The Advisory Note

Strategic vs. Tactical:

Strategic (Long-term): DLPL remains a structural play on India's healthcare formalization. Their "Hub and Spoke" model is the most efficient in the industry, and the current dip in profits is likely an investment phase for future dominance.

Tactical (Short-term): At ₹1,550, the stock is at a crucial level. While the PAT decline is a concern, the top-line momentum is strong. Investors should look for signs of margin stabilization before aggressive fresh buying.