Solar Industries India Limited Q4 FY26 Analysis: Explosive Defense Growth vs. Working Capital Intensity

Welcome back to our elite equity research desk. Today, we dissect the Q4 FY26 performance of Solar Industries India Limited (SOLARINDS). Operating at the dynamic intersection of mining explosives and defense technology, Solar Industries has delivered a record-breaking quarter. However, as disciplined investors, we must look beyond the headline numbers to assess the underlying cash flows, valuation, and operational sustainability.

Let's dive into the data to see if Solar Industries is a strategic long-term hold or a tactical risk.

The Snapshot

(Note: Financial metrics reflect consolidated data)

The 'Wow' Factor

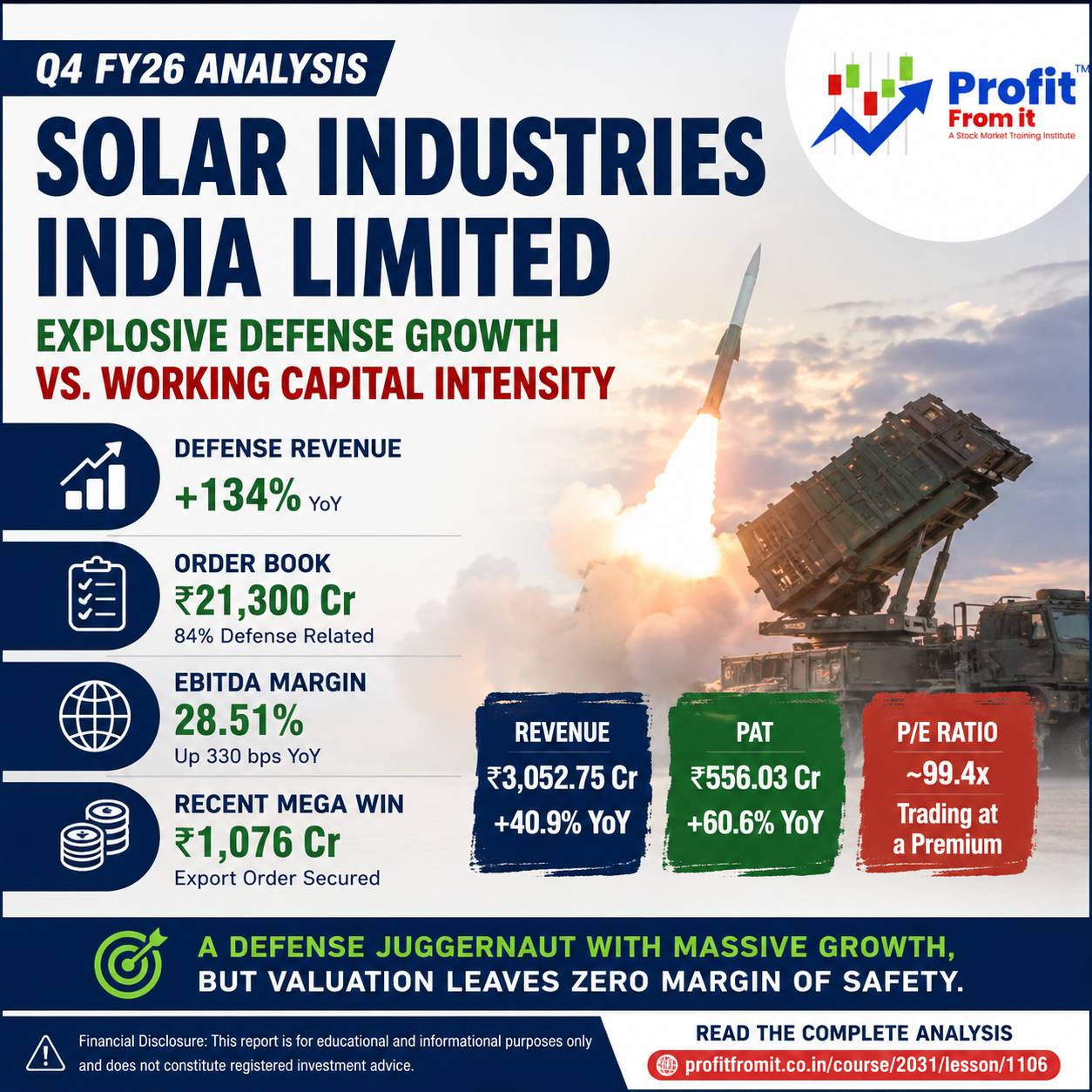

Defense Becomes the Engine: Defense revenue nearly doubled, surging 134% YoY in Q4 to ₹1,008 Cr, now contributing a massive 33% to the quarterly revenue mix (up from 20% in Q4 FY25).

Colossal Order Visibility: The company sits on an order book of ₹21,300Cr, of which ₹18,000 Cr (84%) is defense-related, offering immense multi-year revenue visibility.

Margin Expansion: Highest-ever quarterly EBITDA margins of 28.51% (up 330 bps} YoY), driven by operating leverage and an optimized product mix favoring defense and international markets.

Recent Mega Win: Post-quarter, the company secured a massive ₹1,076 Cr export order for defense products, cementing its global competitiveness.

Operational KPI Table

Financial Deep Dive

Here is the consolidated financial performance for Q4 FY26:

Cost vs. Efficiency

Solar Industries showcased stellar cost control this quarter. The Cost of Materials Consumed as a percentage of sales dropped significantly to $49.84\%$ in Q4 FY26, compared to $54.37\%$ in Q4 FY25. This efficiency is directly linked to an improved product mix, with higher-margin defense and international orders diluting the lower-margin domestic mining constraints.

However, looking at the cash flow statement reveals a stark contrast to the P&L efficiency. Operating cash flows took a massive hit, with the company sucking away roughly $₹1,600\text{ Cr}$ into working capital during FY26. Management cited a strategic inventory build-up to mitigate geopolitical supply chain risks. While prudent from a continuity standpoint, it is a significant drag on cash generation that warrants close monitoring.

$$\text{Cash Conversion} = \frac{\text{Operating Cash Flow}}{\text{EBITDA}}$$

Currently, this ratio is deeply depressed compared to historical averages.

The Forward Curve

Management guidance is intensely bullish. They target FY27 revenue of $₹14,000\text{ Cr}$ (an implied growth of $\sim42\%$ over FY26's $₹9,838\text{ Cr}$). For the next two quarters, we project revenues to track at a run-rate of $₹3,200\text{ Cr} - ₹3,500\text{ Cr}$ per quarter, as execution of the defense order book accelerates and the recent $₹1,076\text{ Cr}$ export order phases in. Capex is slated at an aggressive $₹2,050\text{ Cr}$ for FY27 to support this surge.

Peer Benchmarking

When benchmarked against its closest domestic listed peer, Premier Explosives, Solar Industries operates on an entirely different scale. While Premier may exhibit faster relative percentage growth due to a smaller base, Solar commands unquestionable market leadership, unmatched R&D capabilities (e.g., Bhargavastra counter-drone tech, SEBEX-2), and a vastly superior international footprint spanning 90+ countries. Solar essentially commands the "scarcity premium" of being India's premier integrated defense and explosives play.

Management Integrity and Tone

The tone of MD & CEO Mr. Manish Nuwal during the earnings call was highly confident and transparent. He was unapologetic and clear about the negative operating cash flows, defending the inventory build-up as a deliberate, strategic decision against geopolitical volatility rather than a structural flaw. His candor in addressing the flat domestic mining sector while highlighting international strengths builds substantial investor trust.

Key Risks and Red Flags

Maintaining our 'Margin of Safety' mindset, we must highlight a few critical risks:

Working Capital Drain: The $₹1,600\text{ Cr}$ absorbed into working capital is significant. If geopolitical supply chains normalize and raw material prices drop, the company could face minor inventory write-downs.

Commodity Price Volatility: A spike in ammonium nitrate prices could trigger a near-term demand contraction as buyers wait for prices to cool.

Client Concentration: Heavy reliance on government and defense contracts inherently carries execution and receivable delays, though international diversification is balancing this.

Valuation Guardrails

Let's look at the multiples:

Trailing P/E: $\sim99.4\text{x}$ (Based on FY26 EPS of $₹185.39$)

P/B Ratio: $\sim26.5\text{x}$

Verdict: Trading at a Premium

Solar Industries has historically traded at a premium ($50\text{x} - 60\text{x}$ P/E) due to its moat. However, at nearly $100\text{x}$ trailing earnings, the stock is priced for absolute perfection. The current market capitalization leaves no room for execution missteps or cyclical downturns.

Shareholding Pattern Dynamics

Promoters: Maintained a solid grip at $73.15\%$.

Institutional Confidence: Mutual Funds & AIFs hold a strong $12.18\%$ (led by SBI-MF and Kotak), while FIIs/FPIs hold $6.60\%$. The stable institutional backing underscores long-term confidence in the defense thesis. No significant pledge issues were noted.

The Advisory Note

Strategic Outlook (Long-Term): Solar Industries is a generational wealth creator and a phenomenal proxy for India's "Aatmanirbhar Bharat" defense indigenization and export ambitions. The transition from a mining explosives company to a deep-tech defense contractor is playing out beautifully.

Tactical Outlook (Short-Term): From a price opportunity standpoint, the stock offers zero margin of safety. We advise clients to hold existing positions but wait for a broader market correction or a quarter of consolidated earnings to initiate fresh capital allocations.

Financial Disclosure: This report is for educational and informational purposes only and does not constitute registered investment advice.