IndiGo Q3FY26 Results Analysis: Navigating Turbulence with Resilient Fundamentals

InterGlobe Aviation Limited (IndiGo) remains India’s dominant low-cost carrier, recently navigating a quarter marked by record passenger volumes alongside significant operational and regulatory headwinds. While total income continues to climb, bottom-line profitability was impacted by one-off exceptional items and currency fluctuations.

1. Data-Driven Growth Table: Q3FY26 Performance

Aviation Sector-Specific KPIs

2. Beat/Miss Analysis & Critical Concall Insights

Topline Beat, Bottom-line Miss: Total revenue grew 6.7% YoY, exceeding 245 billion rupees. However, reported PAT plummeted 77.6% primarily due to INR 15,465 million in exceptional items related to new labor codes and operational disruptions.

Operational Resilience: Despite the cancellation of over 2,500 flights in early December, IndiGo served 124 million customers in the calendar year 2025 (a 9% increase YoY).

Strategic Fleet Evolution: The company inducted its first Airbus A321 XLR, enabling 7-8 hour long-haul flights with dual-class cabins, signaling a move toward premium international segments.

Cost Headwinds: CASK ex-fuel ex-forex increased by 2.2% to INR 2.96. Management cited rupee depreciation and capacity moderation as key drivers for rising unit costs.

3. Profitability & Valuation Suite

Profitability Metrics

EBITDAR Margin: 25.6%. While healthy, this is a compression from 27.4% in Q3FY25.

Adjusted PAT: Excluding exceptional items and forex impact, the "underlying" profit was INR 31,306 million.

Cash Position: Strong liquidity remains a moat, with a total cash balance of INR 516,069 million.

Valuation Parameters (at CMP 4915)

Debt-to-Equity: Total debt stands at INR 768,583 million, largely driven by capitalized operating lease liabilities.

Asset Strategy: Management is shifting toward owning assets, with 28 owned aircraft at quarter-end to mitigate forex exposure and strengthen the balance sheet.

4. Performance Trends: Is the Recovery Sustainable?

Considering the H1FY26 revenue growth of 7% and the recent Q3 turnaround from a loss-making Q2, we see a V-shaped recovery in operational stability.

Revenue Trend: Improving. Q3 revenue of INR 245.4 billion is a significant jump from Q2's INR 195.9 billion.

Profit Trend: Mixed. While the reported profit growth is down 78% YoY, the adjusted underlying profit remains robust.

Margin Outlook: Management expects a mid-single-digit percentage increase in unit costs (CASK ex-fuel) for FY26 due to regulatory shifts (FDTL) and currency pressure.

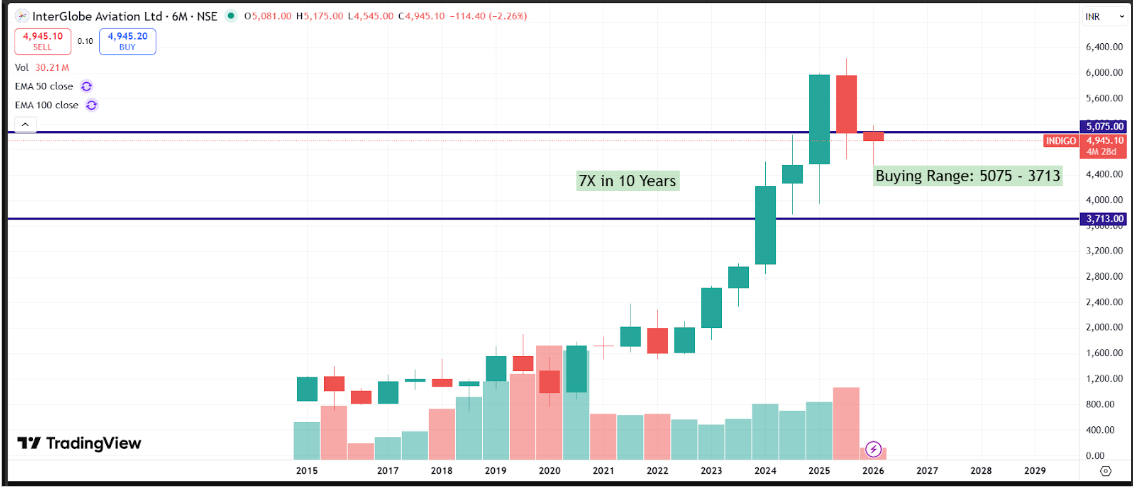

Conclusion & Wealth-Building Perspective

IndiGo is currently in an "invest-to-grow" phase, expanding its international footprint and premium offerings like 'Stretch'. While the current quarter's profit was masked by one-off provisions, the underlying "Cash Engine" remains powerful. For long-term investors, the focus should be on Step 4: Valuation—analyzing if the current market price reflects the long-term potential of its upcoming 900+ aircraft order book.

The detailed Fair Value for INDIGO is available at: https://docs.google.com/spreadsheets/d/e/2PACX-1vQnnMPrFv_rMI3oum6i0vdIDprwF9_e1-GNTwav2jLv5jCchU4vn_M-r74xWQey-g/pubhtml?gid=1870668169&single=true

Disclosure: We are SEBI Registered Investment Advisor. This report is for educational purposes only and does not constitute a direct buy/sell recommendation. Investing in the stock market involves risks;