Bajaj Finance Q3 FY26 Analysis: Robust AUM Scaling vs. Rising Cost of Funds

We have witnessed Bajaj Finance (BAJFINANCE) deliver another quarter of resilient growth, characterized by significant customer acquisition and asset scaling. However, as the credit cycle matures, the "Margin of Safety" mindset remains critical, especially regarding net interest margins and the impact of new regulatory labor codes.

The Snapshot

The 'Wow' Factor

Customer Milestone: Added 4.76 million new customers in Q3 alone, taking the total franchise to a staggering 115.48 million.

AUM Growth: Assets Under Management (AUM) crossed the ₹4,85,000 crore mark, a 26% YoY increase.

New Loan Velocity: Booked 13.90 million new loans in just 90 days, showcasing the efficiency of their omnichannel strategy.

Profitability Resilience: Despite a one-time impact from the New Labour Code, core PBT (before accelerated ECL) grew by 23% YoY.

Operational KPI Table

Financial Deep Dive

The core operating performance remains the "North Star" for Bajaj Finance. While the headline Profit After Tax (PAT) showed some pressure due to a ₹1,164 Cr provision for the New Labour Code and accelerated ECL, the underlying business engine is firing on all cylinders.

Cost vs. Efficiency:

The Opex-to-NII ratio improved to 33.2%, down from 34.0% YoY. We attribute this to the increasing digitisation of the loan lifecycle. However, the Cost of Funds (CoF) increased by 15 bps this quarter, suggesting that while operational efficiency is high, the external borrowing environment remains expensive.

Management Integrity & Tone

We find the management tone to be Transparent and Proactive. During the earnings call, Rajeev Jain (MD) was candid about the "Transient" nature of current credit costs. They are not shifting from "hunting to farming" but rather evolving into a "cross-sell first" organization. This pivot is designed to reduce customer acquisition costs (CAC) in the long run.

The Forward Curve

Based on management guidance, we project:

Q4 FY26: AUM growth likely to maintain the 25-26% corridor.

Q1 FY27: Expected stabilization in NIMs as the cost of funds peaks.

EPS Projection: $EPS_{FY26E} = \frac{Net\ Profit}{Total\ Shares}$. We expect an annualized EPS growth of 18-20%.

Valuation Guardrails

Current PE stands at ~28x, compared to the 5-year median of 35x.

Verdict: Historically Discounted. The market is pricing in regulatory uncertainties (Labour Code) and potential credit cycle peaks, offering a long-term entry point.

Shareholding Pivot

Promoter: Stable at 54.6%.

FII/DII: Marginal increase in DII stake (Mutual Funds) by 0.4%, indicating domestic confidence in the retail credit story.

The Advisory Note

Strategic Outlook (Long-term): Bajaj Finance is no longer just an NBFC; it is a digital payments and lending ecosystem. The "Omnipresence" strategy (Web + App + Offline) creates a moat that is hard for pure-play fintechs to replicate.

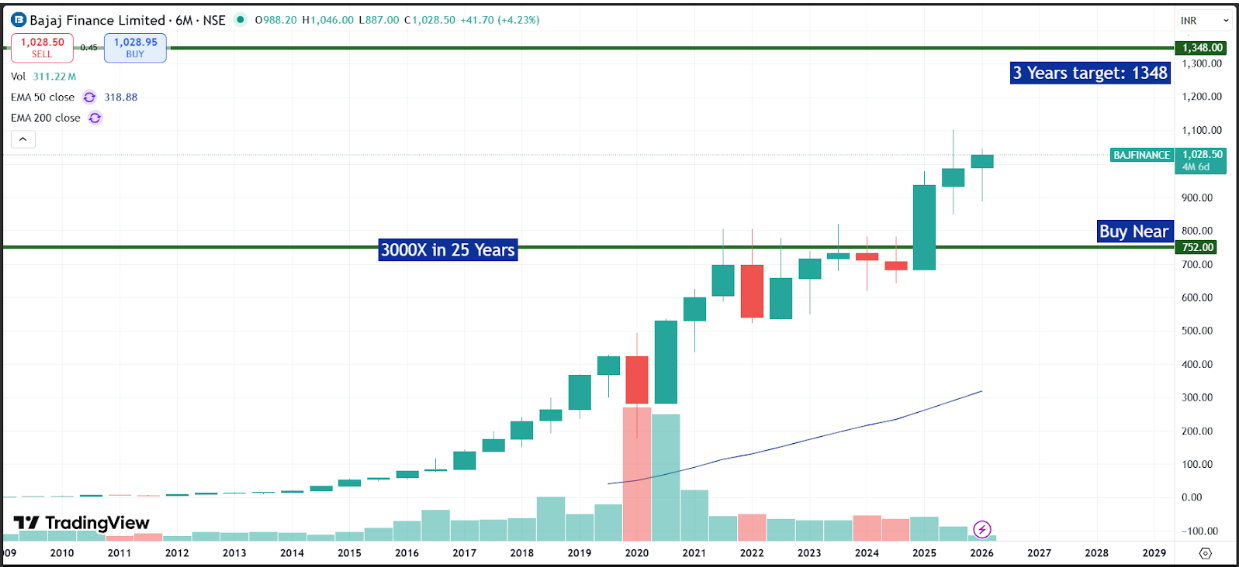

Tactical Outlook (Short-term): The stock may face time-correction as the market absorbs the one-time hit from the New Labour Code provisions. Use price dips toward the 200-day EMA for tactical entries.

Disclosure: This report is for educational purposes only. Investing in equities involves risk. Please consult a SEBI-registered advisor before making investment decisions.