Bajaj Housing Finance Ltd. (BAJAJHFL) Q3 FY26 Results Analysis

Bajaj Housing Finance continues its steady growth trajectory, reporting a 21% YoY increase in Profit After Tax (PAT) for Q3 FY26. The company maintains a high-quality, diversified loan book with a strong focus on prime segments while aggressively scaling its "Sambhav" near-prime and affordable housing unit.

1. Financial Growth Table (Q3 FY26)

*Calculated based on 9M and H1 reported data.

Segmental AUM Growth & Share

2. Sector-Specific KPIs (NBFC/Housing Finance)

Net Interest Margin (NIM): Remained stable at 4.0% YoY and QoQ.

Net Interest Income (NII): Increased 19% YoY to ₹963 Cr.

Asset Quality: GNPA stood at 0.27% and NNPA at 0.11%. Provision Coverage Ratio (PCR) is healthy at 58.76%.

Cost of Funds (CoF): Moderated by 5 bps sequentially to 7.3% , and 60 bps lower than Q3 FY25 (7.9%).

3. Profitability & Valuation Suite

Profitability

Return on Equity (ROE): 12.3% (Annualized).

Return on Assets (ROA): 2.3% (Annualized).

Opex to NTI: Improved to 19.0% from 19.8% YoY.

Valuation & Capital

Price to Book (P/B): Calculated at ~3.3x based on CMP 87 and Net Worth of ₹21,838 Cr (Equity shares: ~832.8 Cr ).

Debt-to-Equity: 4.5 times.

Capital Adequacy (CRAR): 23.15%.

4. Analyst View & Management Insights

Beat/Miss vs. Estimates: The company delivered strong AUM growth of 23%, meeting upper-end internal targets. Asset quality remains superior with GNPA at a minimal 0.27%.

Critical Concall Insights:

Tier-1 Capital Decline: Management explained a ~3% QoQ drop in Tier-1 capital due to conservative provisioning for entire undisbursed tranches of under-construction loans following new RBI consolidation guidelines.

Competitive Intensity: High pressure remains from Public Sector Banks (PSBs) on pricing for "Prime" and "Super Prime" segments.

Sambhav SBU Expansion: Monthly disbursement run-rate for the near-prime/affordable segment is at ₹325–350 Cr, with a target to double this to ₹600 Cr+ in 12–15 months.

Future Growth Outlook (FY26-27):

AUM Growth: Guided at 21–23% for FY26.

Marginal NIM Pressure: NIMs may moderate by 15–20 bps in FY26 due to lower investment income following capital raises in FY25.

Operating Leverage: Management expects Opex to NTI to reach 14–15% over the medium term (3–4 years) as digital and AI interventions scale.

Trend Analysis:

Comparing H1 FY26 (Revenue growth 16%, Net Profit Margin 22.6%) to Q3 FY26:

Revenue Growth: Accelerated to 23.6% in Q3, showing an improving trend.

Net Profit Margin: Stood at 23.04% for Q3, showing a slight improvement over the H1 average.

Conclusion: Wealth-Building Strategy

Bajaj Housing Finance remains a "Low Risk, Scalable" business model focused on anchor products like Prime Housing and LRD. With superior asset quality and a clear path toward operating efficiency, it fits well into a long-term wealth-building strategy (Step 4: Valuation).

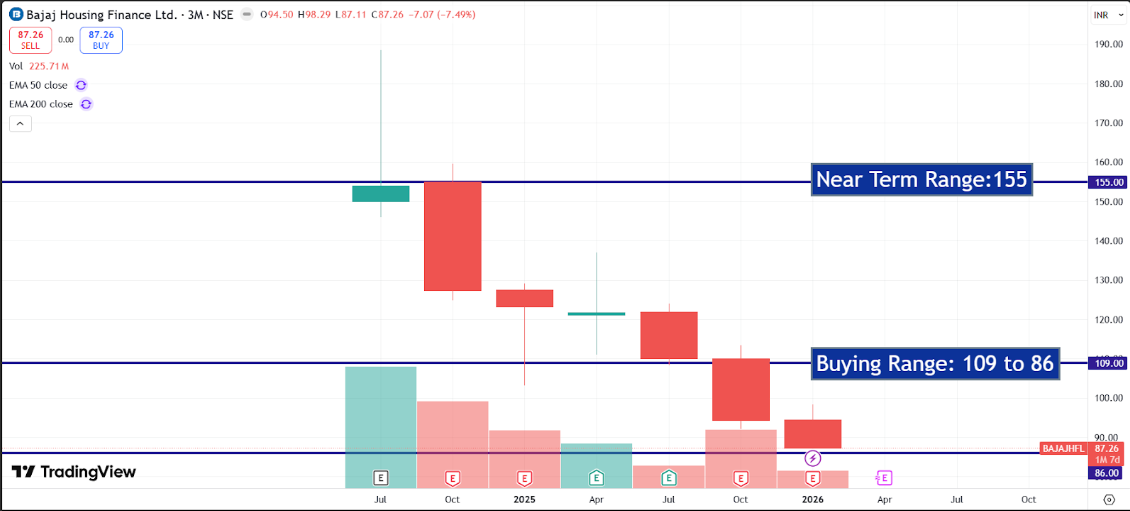

Detailed Fair Value analysis and entry strategies are available at https://docs.google.com/spreadsheets/d/e/2PACX-1vQ0XEkW3UXcRdgIUeuY_R4LO0HkkNODym3xSQjnZQaQBDi7RKpFAdcW2SPZURFmfT3mmX3DxZBEr7FS/pubhtml?gid=190497733&single=true

Disclosure: We are Corporate Investment Advisors. The above analysis is based on publicly available financial data and is intended for educational purposes only. It does not constitute a direct buy or sell recommendation.