Supreme Industries Q4 FY26 Analysis: Volume Leadership vs. Margin Expansion

Supreme Industries has delivered a blockbuster Q4 FY26, characterized by robust top-line growth and a significant surge in profitability. While volume growth remains the bedrock of the company's performance, the sharp rise in PAT suggests improved operational efficiencies and a favorable product mix, even amidst a volatile raw material environment.

The Snapshot

The 'Wow' Factor

Profitability Surge: PAT witnessed a massive ~47.6% YoY growth, significantly outpacing revenue growth.

Highest Ever Volume: The company crossed the 600,000 MT annual volume milestone, reinforcing its market leadership.

Value-Added Dominance: The shift towards high-margin value-added products (~38% share) is clearly translating into bottom-line gains.

Expansion Blueprint: The commitment to 3 new plants in FY27 signals management's aggressive stance on capturing further market share.

Operational KPI Table (Consolidated)

Financial Deep Dive (Consolidated)

Cost vs. Efficiency:

The quarter reflects a masterful balance between scale and profitability. While Revenue grew by a healthy 16.5%, the EBITDA and PAT growth at 33% and 47.6% respectively indicate significant operating leverage. The expansion in margins by over 200 bps YoY suggests that the company successfully navigated PVC resin price volatility by optimizing its procurement and increasing the share of value-added products. Efficiency gains are evident in the controlled growth of other expenses relative to the top-line surge.

The Forward Curve

We project a revenue growth trajectory of for the next half-year. Management insights indicate:

Q1 FY27: Expected volume growth of , supported by a strong start to the agricultural and construction season.

Margin Stability: Guidance points towards maintaining EBITDA margins in the range, aided by the new capacity and lower logistics costs from decentralized production.

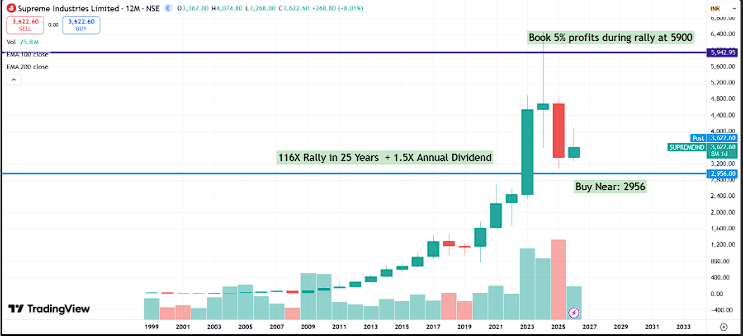

Valuation Guardrails

Current P/E: 33.9x (Adjusted for Trailing 12M PAT)

5-Year Median P/E: 38.2x

Verdict: Fairly Valued to Historically Discounted. With the recent jump in earnings, the stock's valuation has become significantly more attractive compared to its 5-year average.

Shareholding & Management Tone

Promoter Holding: Stable at 48.85%. No pledge issues.

FII/DII Stake: Domestic Institutional Investors (DIIs) have been marginal buyers, showing confidence in the long-term infrastructure and housing story.

Management Integrity: Transparent & Optimistic. The management's focus remains on "profitable volume growth" rather than just chasing market share at any cost.

The Advisory Note

Strategic Outlook (Long-term): Supreme remains the premier play on India's plastic piping and building materials growth. Their debt-free status and consistent capex make them a compounder.

Tactical Outlook (Short-term): The strong earnings beat should act as a catalyst for the stock price. Any dips caused by broader market volatility should be viewed as an entry opportunity given the valuation re-rating potential.