📊 Tata Consumer Products – Q1 FY26 Results: Steady Topline, Margin Challenges

📈 CMP: ₹1055

📆 Quarter Ended: June 30, 2025

🏢 Sector: FMCG – Packaged Foods & Beverages

🔍 Executive Summary

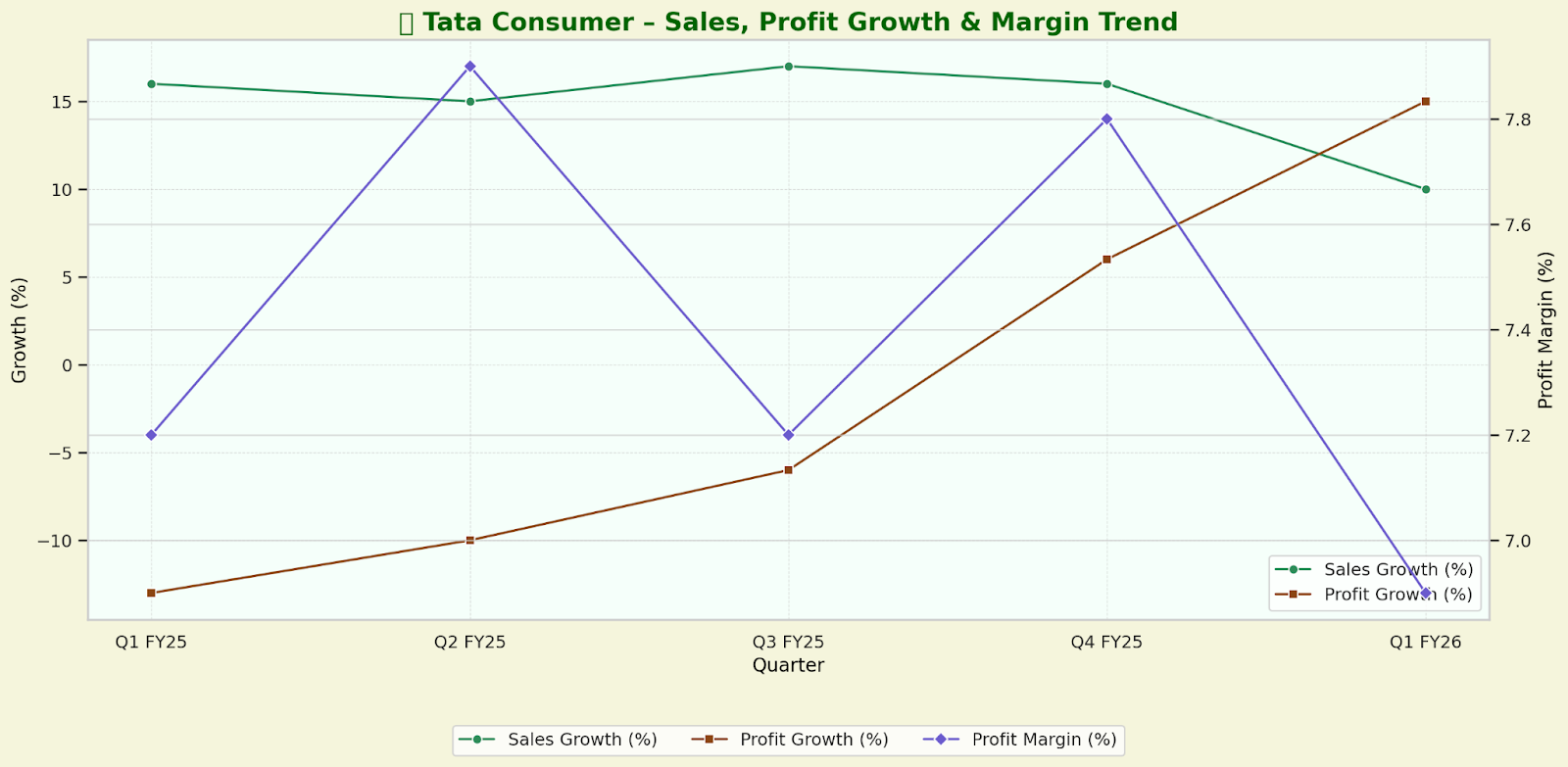

Tata Consumer Products delivered a 10% YoY revenue growth in Q1 FY26, driven by strong momentum in India’s core tea and salt categories. However, EBITDA declined 8% YoY due to inflation in tea and coffee input costs. Profit after tax grew 15% YoY on the back of dividend income and better cost controls.

💡 Key Highlights:

India Packaged Beverages up 12%, with coffee revenue surging 67% YoY ☕

Salt revenue up 13%, Tata Sampann up 27%

EBITDA Margin contracted to 12.9% (down 250 bps)

Net Profit stood at ₹332 Cr, up 15% YoY

📈 Consolidated Financial Performance – Q1 FY26

📊 Segment & Regional Highlights

🇮🇳 India Business: 65% of revenue🌍 International Business: 35% of revenue

🛒 Omnichannel Distribution:

E-Com +61% 📦

Modern Trade +21% 🛍️

Expansion in Food Services & Pharmacies

🌱 Industry-Specific KPIs – FMCG

📉 Margins & Profitability Ratios

📊 Growth Trend Visual

🔮 Outlook – FY26 Guidance & Strategic Direction

📆 Near-Term (Next 1–2 Quarters)

Tea cost inflation remains a margin headwind 🫖

Coffee price volatility may impact non-branded business

Capital Foods & Organic India expected to stabilize with improved ad spends

🧭 Long-Term (FY26–FY30)

Focus on health & wellness, premiumization, innovation

Distribution ramp-up across e-com, QSR, pharmacy channels

Growth businesses (Tata Sampann, Soulfull, Organic India) gaining scale

Tata Starbucks added 6 stores, expanding to Tier-2/3 cities

📌 Valuation & FY26 Estimates

🔍 Current P/E (~78x) seems fully priced. Scope for rerating only with margin revival and strong volume-led growth.

✅ Conclusion for Long-Term Investors

🟢 Positives:

Strong brand portfolio and innovation-led pipeline

Expanding omnichannel presence and premium segments

Balanced growth across core and new businesses

🔴 Risks:

Margin pressure from tea/coffee inflation

Transitory slowdown in Capital Foods/Organic India

Global market volatility

📌 Investment View: Hold with a Positive Bias

Watch for margin improvement and growth in “growth businesses.”

📢 Disclosure

This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making investment decisions.