ITC Hotels Q3FY26 Analysis: Record Revenues & Strategic Scalability

ITC Hotels has reported a stellar performance for the third quarter of FY26, achieving its highest-ever quarterly revenue and profits. The results reflect a robust growth trajectory driven by a structural supply-demand imbalance in the premium hospitality sector and the successful commencement of the residential business in Colombo.

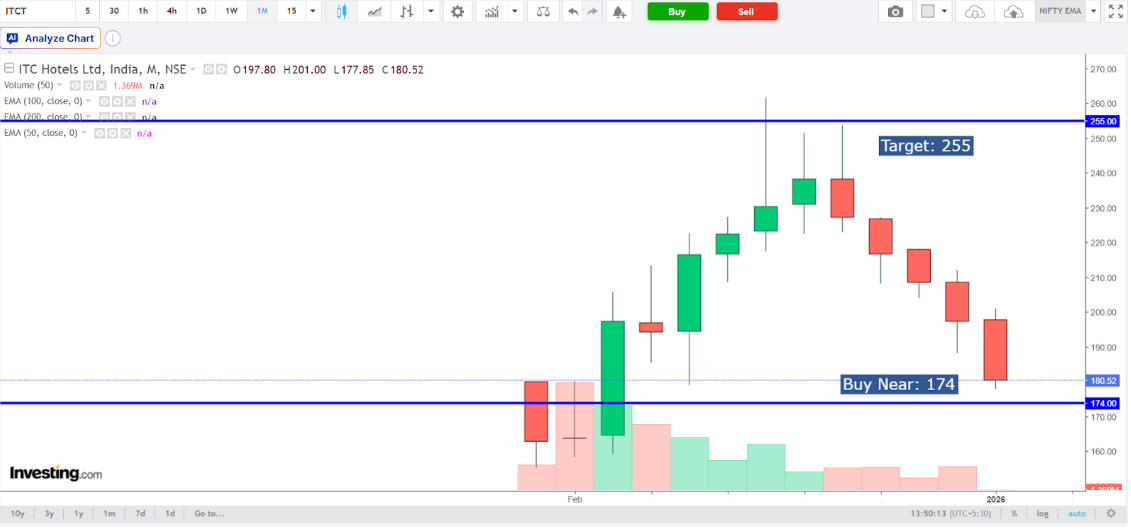

CMP: ₹181 | Market Cap: ~₹38,000 Cr

1. The Financial Growth Table (Consolidated)

The following table highlights the consolidated financial performance for Q3 FY26 compared to previous periods:

Segmental Revenue Growth & Share

The company’s revenue is increasingly diversified with the addition of the real estate segment.

2. Sector-Specific KPIs (Hospitality)

As a leading luxury hospitality player, ITC Hotels tracks specific operational metrics that drive profitability:

RevPAR Growth: Consolidated RevPAR grew by 13% YoY, driven by a 9% increase in ADR (Average Daily Rate) and a 290 bps expansion in Occupancy to 75%.

RevPAR Premium: The company maintained a significant 48% RevPAR premium over the industry average for luxury and upscale segments.

EBITDA Margins: Consolidated EBITDA margins expanded by 47 bps YoY to 38%. On a comparable basis, margins saw a robust 150 bps expansion.

Cost Efficiency: Notable reduction in key costs—F&B costs dropped to 23.6% (from 24.5%), and energy costs fell to 4.6% (from 5.2%) of revenue.

3. Profitability & Valuation Suite

Profitability

ROE / ROCE: Current ROE stands at approximately 6.7% with ROCE at 9.6%.

Operating Margins: Standalone EBITDA margins reached 39%, reflecting strong operational leverage and effective cost management.

Valuation

Current PE: Trading at a trailing PE of ~50x.

Long-term Average PE: The stock's valuation is currently considered "fairly valued" relative to its recent growth trajectory following the demerger.

Price to Book (P/B): 3.36x.

Debt-to-Equity: The company remains "almost debt-free," providing a strong balance sheet for inorganic growth opportunities.

4. Result Commentary & Outlook

Beat/Miss vs. Estimates

Revenue: In-line with analyst expectations, showing a healthy 13% LFL (Like-for-Like) top-line growth.

Profitability: Surpassed expectations on a PAT (before exceptional items) basis, which surged 42% YoY.

Critical Insights from Management

Asset-Right Strategy: Accelerated hotel signings with 28 new hotels (2,790 keys) in CY2025, a 26% growth YoY.

Yashobhoomi Expansion: Secured land for a new 5-star hotel at Yashobhoomi, Delhi, targeted for completion by 2030.

Sri Lanka Turnaround: ITC Ratnadipa in Colombo turned EBITDA positive for the 9-month period ended Dec'25, benefiting from record tourist arrivals.

Future Growth Outlook (FY26-27)

Inventory Pipeline: Target of reaching 220+ hotels and 20,000+ keys by 2030.

Management Fees: Targeting a 2.5x growth in management fees by FY30 over FY25 levels.

Peer Comparison: ITC Hotels maintains a higher RevPAR premium (48%) compared to peers like Indian Hotels (Taj) and EIH (Oberoi) in key markets like Hyderabad (+86%) and Ahmedabad (+56%).

Conclusion

ITC Hotels' Q3FY26 performance confirms its dominance in the premium hospitality segment. With record profits and a clear "Asset-Right" expansion plan, the company is well-positioned for the next growth horizon. In our Wealth-Building Strategy (Step 4: Valuation), we emphasize that buying into quality at reasonable valuations is key.

Fair Value Insight: The Fair Value for ITC Hotels, based on our proprietary discounted cash flow models, is available at https://docs.google.com/spreadsheets/d/e/2PACX-1vQNzwyT8ypfPFozuZO82zZwWhQA677LX16yGKosV8LgD333qX10GQPfZW8pEZvt1UcSw9ozA5lS4-JL/pubhtml?gid=684574702&single=true

Disclosure: This analysis is for educational purposes only and does not constitute a direct buy or sell recommendation. The author is a SEBI registered Investment Advisor.