Affle 3i Limited Q4 FY2026 Analysis: Resilient AI-Led Growth vs. Gross Margin Compression

Date: May 28, 2026

Analyst: Profit from It: Investment Team

Here at the firm, we constantly seek businesses that marry structural mega-trends with resilient unit economics. Our analysis of Affle 3i Limited’s Q4 and 12M FY2026 earnings reveals a company firmly capturing the global shift toward AI-native, ROI-linked digital advertising, albeit with near-term margin trade-offs for long-term premiumization.

The Snapshot

The 'Wow' Factor

Relentless Sequential Compounding: Affle registered its 13th consecutive quarter of sequential top-line growth, defying the typical Q4 (Jan-March) seasonal advertising dip and geopolitical headwinds.

Skin in the Game: The Board approved a preferential issue of approx 7.4 mn warrants at INR 1,487 to corporate promoter Affle Holdings, injecting INR 11,000 mn to build a war chest for global M&A.

Massive Scale: The platform reached over 4 billion connected devices globally, delivering a staggering 456 mn conversions in FY2026.

AI Agentic Moat: Distinct from generic GenAI, Affle’s patented 'Human vs. Non-Human Filtration' algorithm uniquely positions them to protect advertiser ROI against the incoming wave of automated bot traffic.

Operational KPI Table

Affle’s underlying engine is driven by its Cost Per Converted User (CPCU) model. Here is how the core metrics trended:

Financial Deep Dive

Cost vs. Efficiency Analysis:

From a Margin of Safety perspective, we must remain critical of costs. During Q4, Inventory and Data Costs rose to $63.3\%$ of revenues, suppressing Gross Margins down to $\approx 36.5\%$. Management attributes this to a conscious investment in acquiring premium touchpoints (CTV, iOS) to target high Lifetime Value (LTV) users. However, Affle displayed excellent operating leverage elsewhere: Employee Benefit Expenses remained flat sequentially at $\text{INR } 635 \text{ mn}$, proving that their integration of AI (OpticksAI and Niko) is actively driving human capital efficiency.

Management Integrity and Tone

Management’s tone, led by CEO Anuj Khanna Sohum, was authoritative, transparent, and grounded. When questioned aggressively on margin compression, management did not deflect; they transparently guided that gross margin compression is a strategic necessity for premium verticalization, expected to normalize over the next $4 \text{ to } 6$ quarters. Furthermore, the commitment to infuse $\text{INR } 11 \text{ billion}$ of promoter capital at CMP reflects deep conviction in their $10\text{x}$ decadal growth vision.

Peer Benchmarking

While global giants like The Trade Desk operate primarily on the supply/agency side via impression-based (CPM) models, Affle is uniquely entrenched in the Direct-to-Advertiser, conversion-linked (CPCU) model. This structure forces deep first-party data integrations, granting Affle a wider competitive moat against local peers like InMobi or Vertoz. In recessionary environments, advertisers naturally gravitate toward Affle's measurable ROI rather than generic brand-building impressions.

Key Risks and Red Flags

Gross Margin Compression: Data and inventory costs are structurally rising as the firm bids for premium users. If CPCU pricing cannot outpace these costs within 12 months, EBITDA targets may be at risk.

Geopolitical Softness: Management flagged temporary softness in select verticals due to global events. Sustained macro shocks could tighten global marketing budgets.

M&A Execution Risk: Affle is gearing up for a large acquisition ($\approx \$100\text{-}\$200 \text{ mn}$). Transforming non-CPCU legacy targets into Affle's CPCU architecture carries significant execution risk.

The Forward Curve

Looking ahead, management maintains a clear guidance of $\approx 20\%$ CAGR over the next 5 years. For the upcoming halves, we project:

Q1 FY2027 (E): Revenue $\approx \text{INR } 7,550 \text{ mn}$, propelled by new logo additions in Developed Markets and the normalization of ad-spends.

Q2 FY2027 (E): Revenue $\approx \text{INR } 8,000 \text{ mn}$, accelerating into the historically strong festive/holiday season with EBITDA margins stabilizing at $\approx 22.5\%$.

Valuation Guardrails

FY26 EPS: $\text{INR } 32.3$

Current P/E: $\approx 45.7\text{x}$

Compared to Affle's 5-year median P/E of $\approx 60\text{x}$, the stock is currently Historically Discounted. Given the robust $25.5\%$ PAT CAGR delivered from FY22 to FY26 and the strong structural tailwinds of AI in AdTech, the current multiples offer a reasonable entry point for patient capital.

Shareholding Updates

The most critical change is the upcoming preferential issue. Affle Holdings (the corporate promoter) is set to acquire $7.4 \text{ mn}$ warrants at $\text{INR } 1,487$ (requiring a $25\%$ upfront payment). This protects the balance sheet for impending acquisitions while signaling immense promoter confidence right around the current market price.

The Advisory Note

Strategic Outlook: Affle represents a core portfolio holding for exposure to the digital advertising and AI mega-trend. Their focus on the resilient CPCU model and human vs. bot filtration makes them an industry outlier.

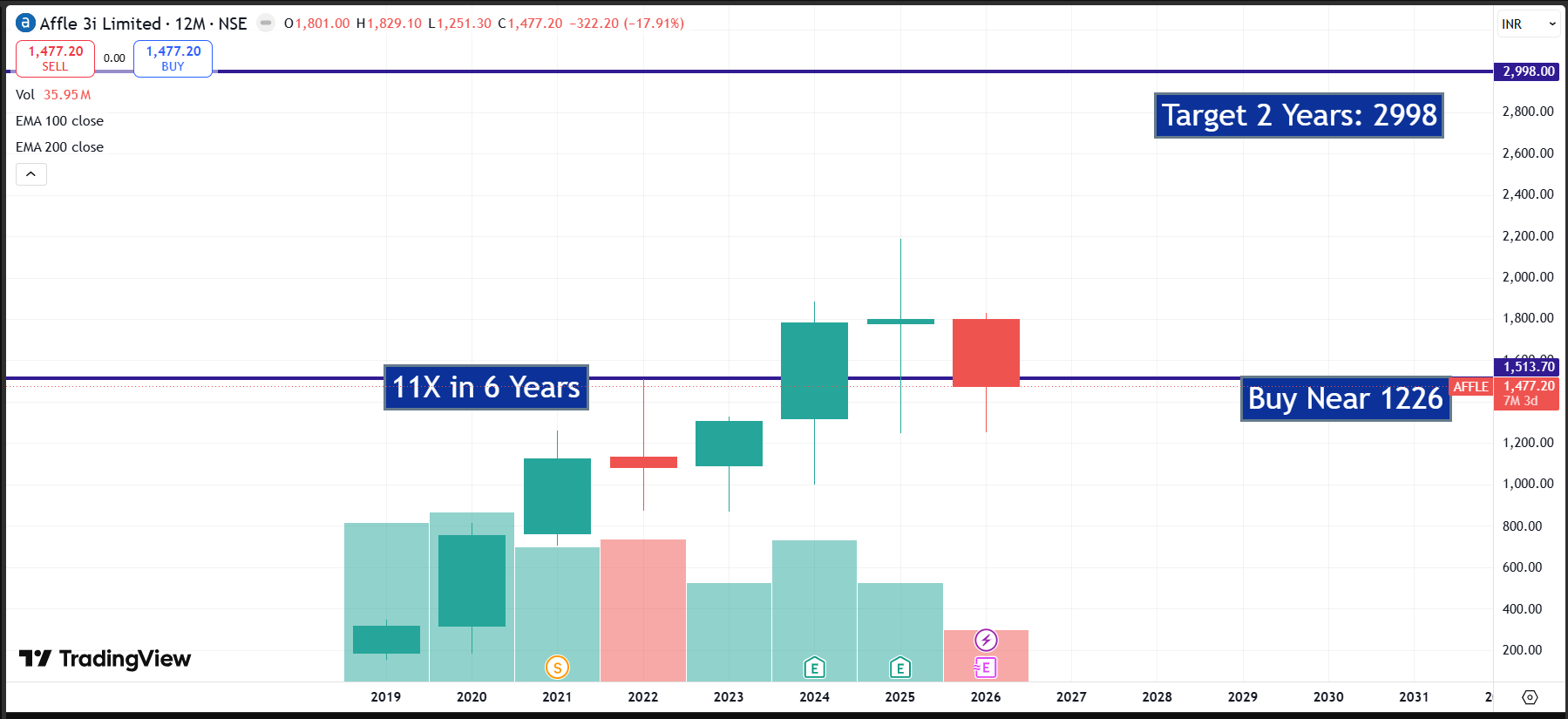

Tactical Opportunity: With the stock hovering near the promoter warrant issue price of $\text{INR } 1,487$, investors are effectively buying at the 'insider floor'. Use current geopolitical volatility to accumulate near 1225.

Disclaimer: This report is for educational and informational purposes only. It does not constitute financial advice. Equity investments are subject to market risks.