Kajaria Ceramics Q4 FY26 Analysis: Volume Resilience vs. Realization Headwinds

As the domestic real estate cycle continues its upswing, Kajaria Ceramics, India’s premier tile manufacturer, has navigated a complex Q4. While volume growth remains the North Star for management, pricing pressures in a fragmented market have tested the margins of even the strongest players. At our firm, we maintain a "Margin of Safety" mindset, closely watching if volume gains are being bought at the cost of realizations.

The Snapshot

The 'Wow' Factor

Volume Milestone: Achieved a solid volume growth of 11% YoY in Q4, significantly outperforming the earlier flattish trend in the first nine months of the fiscal.

Dividend Boost: The board recommended a final dividend of ₹6 per share, bringing the total FY26 dividend to ₹11, demonstrating strong cash flow confidence.

Buyback Announcement: In a strong signal of confidence, the board approved a buyback of equity shares worth ₹296.70 Crores at a price of ₹1,380 per share.

Gas Cost Optimization: Management has successfully shifted a larger portion of its energy mix to cheaper biofuels and spot RLNG, softening the blow of high long-term gas contracts.

Operational KPI Table

Financial Deep Dive (Consolidated)

Cost vs. Efficiency:

The EBITDA margin expanded significantly to 19.19% in Q4 FY26 from 10.01% in the year-ago period. While Revenue grew by over 12%, the profit surge was driven by massive operational leverage and a correction in fuel costs. The company is strategically trading some pricing power for volume leadership—a move that has clearly paid off this quarter as unorganized players in the Morbi cluster faced supply disruptions.

The Forward Curve

Based on management guidance, we project:

Q1 FY27: Expected Revenue growth of 8-10% as the wedding season and renovation demand peak.

Q2 FY27: Volume growth expected to sustain at 9%+ as new capacities in Nepal and South India fully ramp up.

Full Year Guidance: Management maintains a double-digit volume growth target for FY27.

Valuation Guardrails

Analysis: Historically, Kajaria has commanded a premium. Even with the massive PAT jump, the stock trades at a reasonable P/E relative to its 5-year median, suggesting the market is still digesting the sustainability of these margins.

Shareholding & Integrity

Shareholding Pattern: Promoters hold a steady 47.69%. Notably, institutional investors (FIIs + DIIs) hold a combined 38.4%, indicating strong institutional confidence.

Pledge: 0% (Clean balance sheet).

Management Tone: Transparent & Confident. Management highlighted that the "unification of sales" efforts in the first 9 months have finally started yielding results in Q4.

The Advisory Note

Strategic Outlook (Long-Term): The structural shift from unorganized to organized players, coupled with the "Housing for All" momentum, makes Kajaria a core portfolio compounder. The entry into Bathware and Adhesives provides a vertical scaling opportunity.

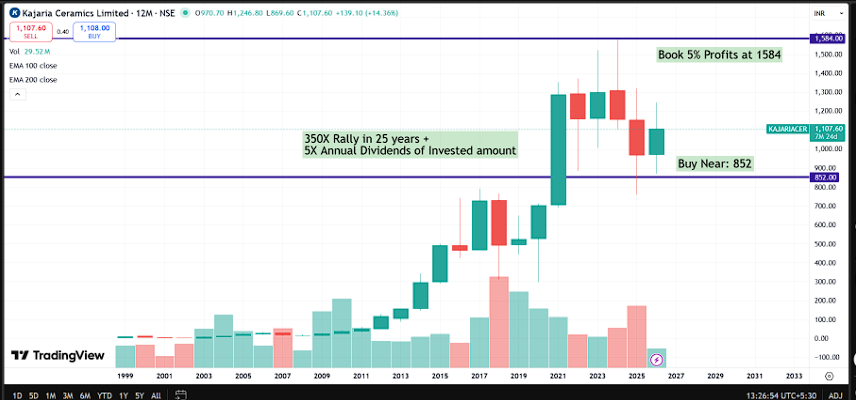

Tactical Outlook (Price Opportunity): With the buyback priced at ₹1,380, the current CMP of ₹1,098 offers a compelling entry point for medium-term investors, representing a significant discount to the company's own valuation of its shares.

Financial Disclosure: This report is for educational and informational purposes only. We are SEBI-registered advisors.