NTPC FY26 Results: Why the Green Energy Pivot is a Game Changer for Investors.

The Snapshot

The 'Wow' Factor

Massive Capacity Scaling: Group installed capacity has hit 90,857 MW, with aggressive solar commissioning via NGEL.

Large Corporate Status: NTPC successfully verified as a 'Large Corporate' for FY26, highlighting strong creditworthiness and access to liquidity.

Operational Velocity: Multiple project milestones (Patratu Unit#2, Khavda-II Solar) achieved in the June 2026 quarter, signaling strong execution capability.

Operational KPI Table (FY26 Context)

Financial Deep Dive (Consolidated)

Based on the FY26 Audited Consolidated Financial Statement provided:

Cost vs. Efficiency: While top-line growth remained muted due to stabilization in power tariffs and fuel cost pass-throughs, the company demonstrated superior EBITDA margin expansion through cost-optimization measures and improved PLFs (Plant Load Factors).

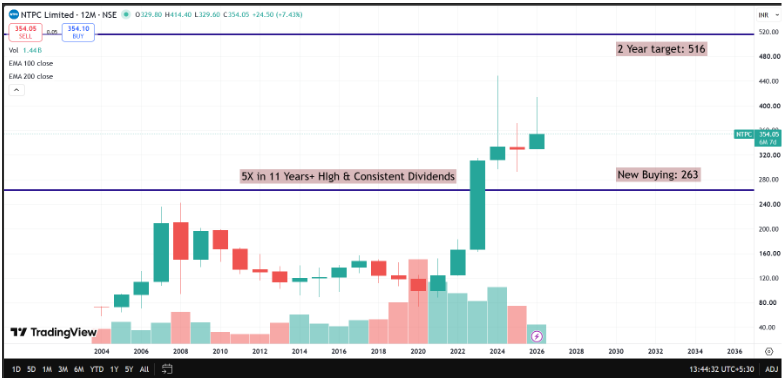

Valuation Guardrails

Current P/E: NTPC trades at approximately 10.5x – 11.5x (Consolidated).

Verdict: Fairly Valued. Given the aggressive transition to renewables via NGEL, the market is beginning to assign a "Green Premium" to the stock, justifying the current valuation compared to its 5-year historical median.

Advisory Note: Strategic vs. Tactical

Long-term Thesis: NTPC is transforming from a thermal-heavy utility into an integrated energy provider. The upcoming IPO of the green energy arm remains the ultimate value unlocking trigger.

Strategic Outlook: Investors should maintain their core holdings. Any price corrections toward the 320-330 level offer a robust margin of safety.

Disclosure: Our firm holds an investment position in the power utility sector. This report is for professional advisory use.